|

JOHN RUBINO'SLATEST BOOK |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

Weekend Nov 7th, 2015

Follow Our Updates

onTWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

ARCHIVES

| OCTOBER | ||||||

| S | M | T | W | T | F | S |

| 1 | 2 | 3 | ||||

| 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| 11 | 12 | 13 | 14 | 15 | 16 | 17 |

| 18 | 19 | 20 | 21 | 22 | 23 | 24 |

| 25 | 26 | 27 | 28 | 29 | 30 | 31 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 |

KEY TO TIPPING POINTS |

| 1- Bond Bubble |

| 2 - Risk Reversal |

| 3 - Geo-Political Event |

| 4 - China Hard Landing |

| 5 - Japan Debt Deflation Spiral |

| 6- EU Banking Crisis |

| 7- Sovereign Debt Crisis |

| 8 - Shrinking Revenue Growth Rate |

| 9 - Chronic Unemployment |

| 10 - US Stock Market Valuations |

| 11 - Global Governance Failure |

| 12 - Chronic Global Fiscal ImBalances |

| 13 - Growing Social Unrest |

| 14 - Residential Real Estate - Phase II |

| 15 - Commercial Real Estate |

| 16 - Credit Contraction II |

| 17- State & Local Government |

| 18 - Slowing Retail & Consumer Sales |

| 19 - US Reserve Currency |

| 20 - US Dollar Weakness |

| 21 - Financial Crisis Programs Expiration |

| 22 - US Banking Crisis II |

| 23 - China - Japan Regional Conflict |

| 24 - Corruption |

| 25 - Public Sentiment & Confidence |

| 26 - Food Price Pressures |

| 27 - Global Output Gap |

| 28 - Pension - Entitlement Crisis |

| 29 - Central & Eastern Europe |

| 30 - Terrorist Event |

| 31 - Pandemic / Epidemic |

| 32 - Rising Inflation Pressures & Interest Pressures |

| 33 - Resource Shortage |

| 34 - Cyber Attack or Complexity Failure |

| 35 - Corporate Bankruptcies |

| 36 - Iran Nuclear Threat |

| 37- Finance & Insurance Balance Sheet Write-Offs |

| 38- Government Backstop Insurance |

| 39 - Oil Price Pressures |

| 40 - Natural Physical Disaster |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

Charles Hugh Smith's Latest Books

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

OTHERS OF NOTE

Book Review- Five Thumbs Up

for Steve Greenhut's Plunder!

![]()

TODAY'S TIPPING POINTS

|

Have your own site? Offer free content to your visitors with TRIGGER$ Public Edition!

Sell TRIGGER$ from your site and grow a monthly recurring income!

Contact [email protected] for more information - (free ad space for participating affiliates).

HOTTEST TIPPING POINTS |

Theme Groupings |

||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro

|

|||

|

MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

||

|

|||

|

11-07-15 | SII | |

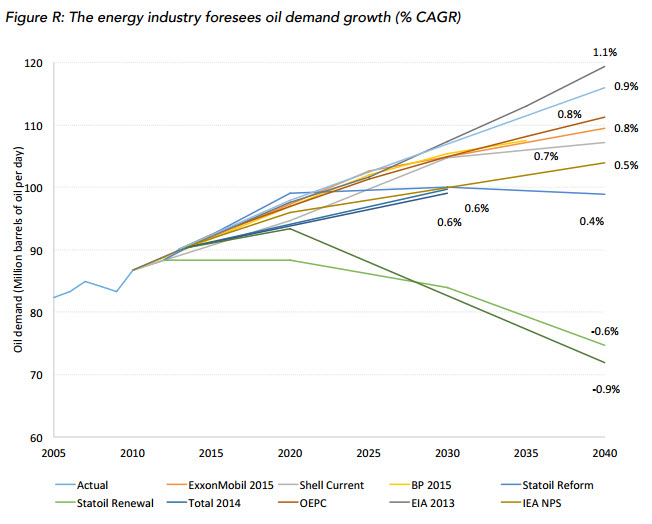

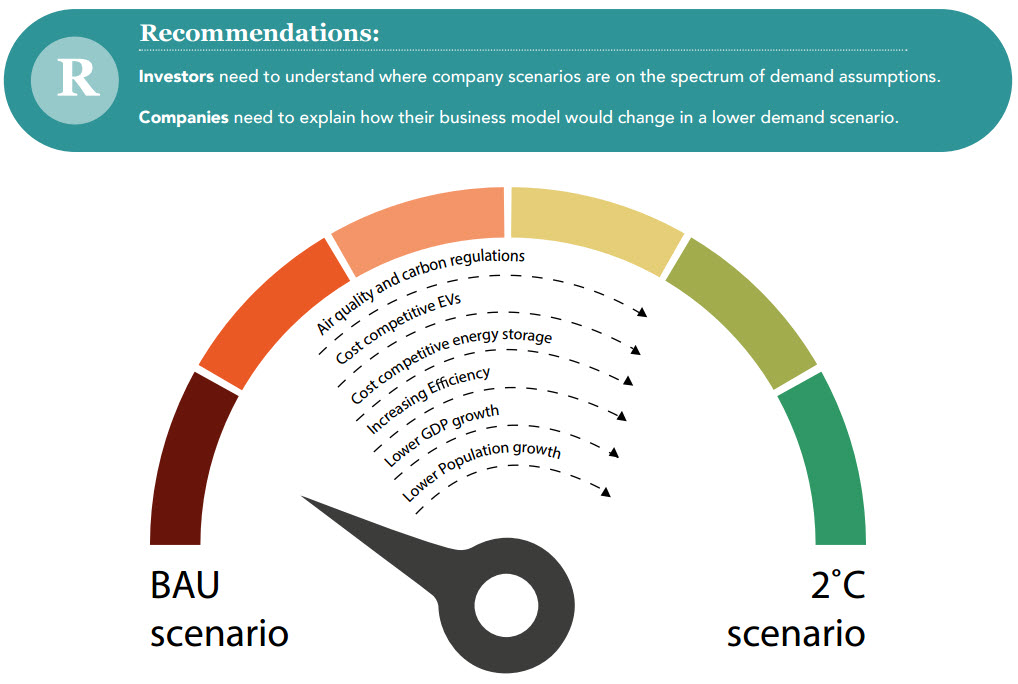

Submitted by Tyler Durden on 11/02/2015 What The Oil And Gas Industry Is Not Telling InvestorsSubmitted by Nick Cunningham via OilPrice.com, Oil prices crashed because of too much supply, but will rebound as production shrinks and demand rises. But what if long-term demand for oil ends up being sharply lower than what the oil industry believes? That is the subject of a new report from The Carbon Tracker Initiative, which looks at a range of scenarios that could blow up oil industry projections for long-term oil demand. Historically, Carbon Tracker says, energy demand has been driven by population, economic growth, and the efficiency (or inefficiency) of energy-using technologies. Carbon Tracker looks at a couple possible future scenarios in which those parameters are altered, resulting in dramatically lower rates of oil consumption. Carbon Tracker has been a pioneer in the concept of “stranded assets,” the notion that fossil fuel assets will lose their value as the world moves to restrict carbon emissions. If an oil field cannot be produced profitably in a carbon-constrained world – or cannot legally be produced because of certain regulations – then it ceases to have value. That puts investors’ dollars at risk, a risk that financial markets have not fully grappled with. However, in a new report, Carbon Tracker expands upon the possible scenarios in which oil demand may not live up to industry predictions. For example, if the world population hits only 8.3 billion by 2050 instead of the 9.7 billion figure typically cited by the UN, fossil fuel consumption could end up being 17 percent lower in 2050 than the oil industry thinks. Coal would be affected the most, with 25 percent reduction in demand compared to the business-as-usual case. How about GDP growth? The expansion of the global economy is pivotal to energy consumption. The industry typically bakes in a GDP growth rate of 2.8 to 3.6 percent per year into its forecasts. But these figures could be on the high end, especially since so much hinges on the ongoing blistering growth from China. But, using BP’s pessimistic GDP scenario in which China and India only grow at 4 percent per year, global energy demand could be 8.5 percent lower in 2035 than the business-as-usual case.

Perhaps more threatening to future oil demand are global policies to ratchet down greenhouse gas emissions, as previously touched upon. Although international negotiations have largely failed to halt the growth of carbon emissions, a significant effort to zero out carbon over the long-term would necessarily cut deeply into demand. Industry projections largely ignore this possibility, as industry estimates for fossil fuel demand in the future would likely lead to average global warming of 4 to 6 degrees Celsius, exceeding the stated goal of capping warming at 2 degrees. More importantly, industry projections for fossil fuel use already exceed the totals that would result if the carbon reduction goals already laid out by countries heading into Paris are implemented. Caps on emissions would upend the entire business model of the oil industry. Carbon Tracker looks at a few other scenarios, including the possibility that renewable energy could make cost reductions and deployment much greater than the oil industry thinks. Indeed, energy prognosticators like the IEAconsistently underestimate the market penetration of solar PV and wind. Actual deployment wildly exceeds every projection that the IEA publishes. It is not hard to see oil industry projections off the mark, undone by falling costs and rapid deployment of solar and wind. Moreover, the combination of energy storage and renewable energy could transform power markets, solving the problem of intermittent energy. Battery storage continues to get cheaper, another trend that the oil industry could be underestimating. Electricity market transformation would also help scale up battery manufacturing, which in turn would reduce the cost of electric vehicles. Take Toyota’s recent announcement that it will target a 90 percent reduction in greenhouse gas emissions from its vehicles by 2050 by developing fuel cell vehicles. There is a long way to go before such a scenario becomes viable, but the announcement should is a shot across the bow for the oil industry. In short, Carbon Tracker concludes, there are very real threats to the business models of oil companies, threats that need to be explained to investors. Right now, those threats are not being taken seriously.

|

|||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - Nov. 1st, 2015 - Nov 7th, 2015 | |||

| BOND BUBBLE | 1 | ||

| RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates | 2 | ||

| RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates | 10-29-15 | GLOBAL RISK SIGNALS | 2 |

| GEO-POLITICAL EVENT | 3 | ||

| CHINA BUBBLE | 4 | ||

| JAPAN - DEBT DEFLATION | 5 | ||

EU BANKING CRISIS |

6 |

||

| TO TOP | |||

| MACRO News Items of Importance - This Week | |||

GLOBAL MACRO REPORTS & ANALYSIS |

|||

US ECONOMIC REPORTS & ANALYSIS |

|||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | |||

| Market | |||

| TECHNICALS & MARKET |

|

||

| COMMODITY CORNER - AGRI-COMPLEX | PORTFOLIO | ||

| SECURITY-SURVEILANCE COMPLEX | PORTFOLIO | ||

| THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur | |||

| 2015 - FIDUCIARY FAILURE | 2015 | THESIS 2015 |  |

| 2014 - GLOBALIZATION TRAP | 2014 |  |

|

|

|||

|

2013 2014 |

|

||

2011 2012 2013 2014 |

|

||

| THEMES - Normally a Thursday Themes Post & a Friday Flows Post | |||

I - POLITICAL |

|||

| CENTRAL PLANNING - SHIFTING ECONOMIC POWER - STATISM | THEME | ||

- - CORRUPTION & MALFEASANCE - MORAL DECAY - DESPERATION, SHORTAGES. |

THEME |  |

|

| - - SECURITY-SURVEILLANCE COMPLEX - STATISM | M | THEME | |

| - - CATALYSTS - FEAR (POLITICALLY) & GREED (FINANCIALLY) | G | THEME | |

II-ECONOMIC |

|||

| GLOBAL RISK | |||

| - GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | G | THEME | |

| - - SOCIAL UNREST - INEQUALITY & A BROKEN SOCIAL CONTRACT | US | THEME | |

| - - ECHO BOOM - PERIPHERAL PROBLEM | M | THEME | |

| - -GLOBAL GROWTH & JOBS CRISIS | |||

| - - - PRODUCTIVITY PARADOX - NATURE OF WORK | THEME | MACRO w/ CHS |

|

| - - - STANDARD OF LIVING - EMPLOYMENT CRISIS, SUB-PRIME ECONOMY | US | THEME | MACRO w/ CHS |

| STANDARD OF LIVING - SUB-PRIME ECONOMY | US | THEME | MACRO w/ CHS |

III-FINANCIAL |

|||

| FLOWS -FRIDAY FLOWS | MATA RISK ON-OFF |

THEME |  |

| CRACKUP BOOM - ASSET BUBBLE | THEME | ||

| SHADOW BANKING - LIQUIDITY / CREDIT ENGINE | M | THEME | |

| GENERAL INTEREST |

|

||

| STRATEGIC INVESTMENT INSIGHTS - Weekend Coverage | |||

|

SII | ||

|

SII | ||

|

SII | ||

|

SII | ||

| TO TOP | |||

Read More - OUR RESEARCH - Articles Below

Tipping Points Life Cycle - Explained

Click on image to enlarge

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

�

TO TOP