|

JOHN RUBINO'SLATEST BOOK |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

Tues. Apr. 12th , 2016

Follow Our Updates

on TWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

![]()

| APRIL | ||||||

| S | M | T | W | T | F | S |

| 1 | 2 | |||||

| 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| 10 | 11 | 12 | 13 | 14 | 15 | 16 |

| 17 | 18 | 19 | 20 | 21 | 22 | 23 |

| 24 | 25 | 26 | 27 | 28 | 29 | 30 |

KEY TO TIPPING POINTS |

| 1- Bond Bubble |

| 2 - Risk Reversal |

| 3 - Geo-Political Event |

| 4 - China Hard Landing |

| 5 - Japan Debt Deflation Spiral |

| 6- EU Banking Crisis |

| 7- Sovereign Debt Crisis |

| 8 - Shrinking Revenue Growth Rate |

| 9 - Chronic Unemployment |

| 10 - US Stock Market Valuations |

| 11 - Global Governance Failure |

| 12 - Chronic Global Fiscal ImBalances |

| 13 - Growing Social Unrest |

| 14 - Residential Real Estate - Phase II |

| 15 - Commercial Real Estate |

| 16 - Credit Contraction II |

| 17- State & Local Government |

| 18 - Slowing Retail & Consumer Sales |

| 19 - US Reserve Currency |

| NEW - Stagflation - Slow Growth & Personal Inflation |

| 20 - US Dollar |

| 21 - Financial Crisis Programs Expiration |

| 22 - US Banking Crisis II |

| 23 - China - Japan Regional Conflict |

| 24 - Poorly Regulated Corruption |

| 25 - Public Sentiment & Confidence |

| 26 - Food Price Pressures |

| 27 - Global Output Gap |

| 28 - Pension - Entitlement Crisis |

| 29 - Central & Eastern Europe |

| 30 - Terrorist Event |

| 31 - Pandemic / Epidemic |

| 32 - Rising Inflation Pressures & Interest Pressures |

| 33 - Resource Shortage |

| 34 - Cyber Attack or Complexity Failure |

| 35 - Corporate Bankruptcies |

| 36 - Iran Nuclear Threat |

| 37- Finance & Insurance Balance Sheet Write-Offs |

| 38- Government Backstop Insurance |

| 39 - Oil Price Pressures |

| 40 - Natural Physical Disaster |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

![]()

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

![]()

Charles Hugh Smith's Latest Books

![]()

![]()

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

![]()

![]()

![]()

![]()

![]()

OTHERS OF NOTE

![]()

![]()

![]()

![]()

Book Review- Five Thumbs Up

for Steve Greenhut's

Plunder!

![]()

|

HOTTEST TIPPING POINTS |

Theme Groupings |

||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro

|

|||

"BEST OF THE WEEK " MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

||

8 - Shrinking Revenue Growth Rate |

04-12-16 | 8 - Shrinking Revenue Growth Rate |

|

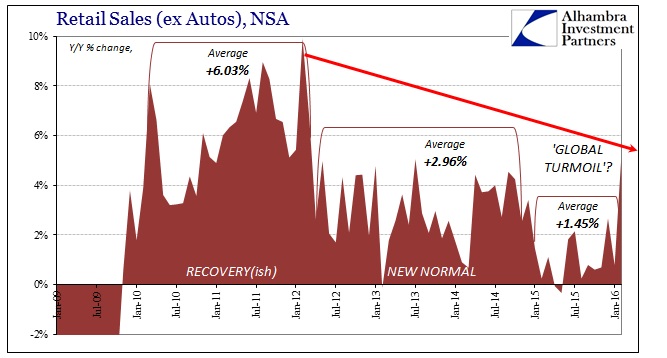

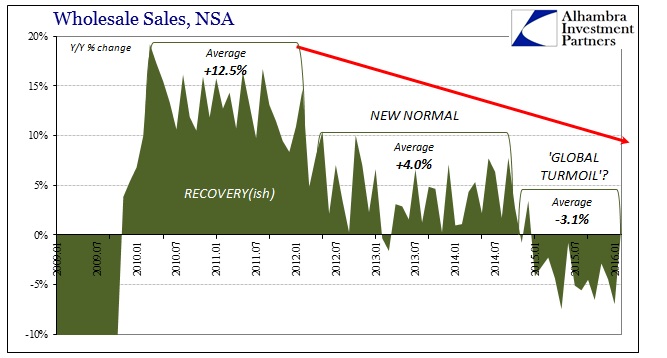

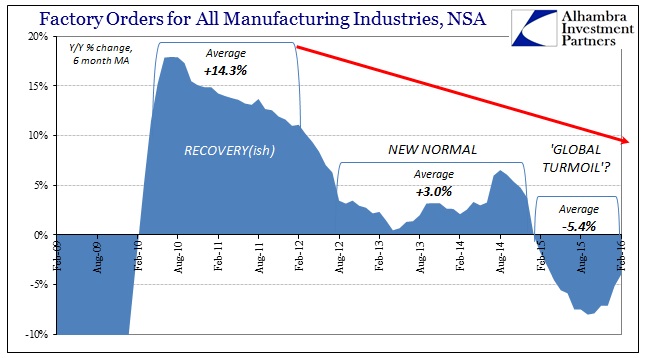

Supply Chain Slump "Worse Than The Great Recession"Submitted by Jeffrey Snider via Alhambra Investment Partners, Not to continue beating a dead horse, but I have a stick and the carcass is right in front of me. The entire supply chain inside the US economy is full agreement both on where the economy is right now and, perhaps more importantly, how it came to be that way. Such harmony is not atypical, as synchronicity usually defines the hard edges of any cycle. This, however, is something else entirely, especially as it stretches back years and confirms we are witnessing nothing like the usual. As it is, this latest part or phase or whatever has already taken up nearly two years. In terms of wholesale sales, as noted this morning, overall sales peaked in July 2014 – meaning nineteen months (thru Feb 2016) of deceleration into sustained contraction. Worse and what is probably the most concerning is that after those nineteen months inventory is only just now starting to correct, and it is doing so ever so gently. That suggests again slowdown without yet any visible end. In that sense, recession might actually be the best case since it would greatly speed up the affair in at least the convergence and reversion of inventory to sales (though that would still leave questions about the economic trend after it). By comparison, the Great Recession featured just nine months of contraction; the whole of the dot-com recession twelve. Those were both top to bottom, peak to trough, over and done with. In 2016, we are very likely facing two years and still only the beginning of reconciliation or balance, and no idea what that might mean further down in wider economic feedbacks and negative multipliers. The supply chain, top to bottom:

One other noteworthy interpretation: to find the “goods economy” including the whole of the supply chain in such joined, steady dislocation cannot be anything but a negative comment on the whole of the economy, services included. That starts with the fact that a significant portion (as much as half) of the “services economy” directly addresses the “goods economy” (retail, wholesale, transportation, etc.). Beyond that, if there is total breakdown in growth and advance in goods that can only mean a serious problem with US consumers. It has already forced economists and policymakers to completely abandon what was in late 2014 and early 2015 inarguable recovery and success. Just because it has not, so far, acted like recession does not propose a clean bill of health (just like it did not, last year, recommend this was all some temporary slump worthy of nothing but dismissal). Instead, that it has continued on for so long suggests quite the opposite, and, again, likely worse than just recession prospects in the long run. |

|||

TIPPING POINTS, STUDIES, THESIS, THEMES & SII COVERAGE THIS WEEK PREVIOUSLY POSTED - (BELOW) |

|||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - Apr 11th, 2016 to April 16th, 2016 | |||

| TIPPING POINTS - This Week - Normally a Tuesday Focus | |||

| BOND BUBBLE | 1 | ||

| RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates | 2 | ||

| GEO-POLITICAL EVENT | 3 | ||

| CHINA BUBBLE | 4 | ||

| JAPAN - DEBT DEFLATION | 5 | ||

EU BANKING CRISIS |

6 |

||

| TO TOP | |||

| MACRO News Items of Importance - This Week | |||

GLOBAL MACRO REPORTS & ANALYSIS |

|||

US ECONOMIC REPORTS & ANALYSIS |

|||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | |||

| Market - WEDNESDAY STUDIES | |||

| STUDIES - MACRO pdf | |||

TECHNICALS & MARKET |

|

||

| COMMODITY CORNER - AGRI-COMPLEX | |||

| THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur | |||

|

2016 | THESIS 2016 |  |

| 2015 - FIDUCIARY FAILURE | 2015 | THESIS 2015 |  |

| 2014 - GLOBALIZATION TRAP | 2014 |  |

|

|

|||

|

2013 2014 |

|

||

James Rickards:“The only way every currency can get cheaper at the same time, is not against themselves, but against Gold!”James Rickards, Chief Global Strategist at West Shore Funds and a widely renowned author is interviewed by FRA Co-founder Gordon T. Long in which they discuss Jim’s just released book The New Case for Gold. They also delve into issues concerning the false perceptions of the world switching back to a Gold Standard and the reasons for a suspected G-20 stealth “Shanghai Accord”. THE NEW CASE FOR GOLD James Rickards suggests that there is a new case for Gold and points out that everyone thinks that what they own currently, in terms of stocks, bonds and other financial securities, is actually only “electronic digits” representing claims on assets. The new reality of Cyber war and Cyber attack suggests the real possibility of a single group of people or political regime hacking U.S servers. The potential exists today for investors to lose wealth and there will be almost nothing any one can do to bring back that money, at least in any realistic period of time. Physical Gold cannot be hacked nor simply be erased from the world’s ledger. It is the most tangible and secure way of preserving wealth and James recommends a portfolio with at least 10% being allocated to physical Gold. Being outside the system, and being non-digital are the two main reasons that smart investors economists suggest will ensure having some sort of security for your wealth. Gold meets both these requirements and in the next big financial crisis will provide you with insurance for the rest of your portfolio.

OUTSIDE THE BANKING SYSTEM – The Best Kind if Insurance The financial system is inherently unstable based on:

Gold acts as an insurance policy no matter what happens:

Gold is always gold – It’s outside the banking system, can’t be reproduced by fiat, It cannot be “hacked”.

Jim talks to FRA about methodically dispelling the decades old arguments and fallacies associated with going back to the Gold Standard. He additionally dispels myths such as:

GOLD IS STILL A MONETARY ASSET & REAL MONEY Rickards feels that over 40 years of “un-education or mis-education” has resulted in the new generation of economists and youth not understanding the importance or the value behind why gold is so important for our economy. We cannot blame the new generation for this gap inn their knowledge. We have not been teaching Gold as money in university curriculum and along with myths created about gold have virtually disowning it from economic thinking.

Gold is the one form of monetary value that can’t fight back which is why they have completely stopped educating the U.S public on Gold as a whole. A POST MONETARY RESET – Gold after the Next Crisis The current financial system is inherently unstable and may soon have to be reformed. Gold will play a prominent role, if that happens. The IMF is the third largest holder of official gold reserves after the United States. Gold is at the very center of international finance as the International Monetary Fund (IMF) with its Special Drawing Rights (SDR) reserve currency is regaining prominence. In addition, the current valuation of the SDR could not be calculated without using gold, even though one has to go back to the 1970s to understand why. China is not only acquiring vast quantities of physical gold, it is also going through the hassle of infiltrating the London gold market and simultaneously setting up its own clearing mechanism in Shanghai. Russia has boosted its gold to GDP ratio to 2.7 percent, higher than the United States percentage of 1.7 percent. All powers are acquiring gold to have some bargaining power when the international financial system will be reformed.

Why? After redistributing the official gold holdings and having monetized everything from bonds to stocks, the world’s governments and central banks won’t have a choice left other than to devalue paper money compared to gold, the same trick President Roosevelt used during the great depression and with the same objective of getting rid of an unsustainable debt burden. In a monetary reset, gold will be the chips that are used to play a game of poker. Russians, Chinese and even the Iranians are stock piling gold because of this fear. If Gold has a role in the future monetary system, Gold’s price has to go up. Gold cannot multiply at the alarming rate that we will need it for. But we can always increase the price which is why the current monetary system will fail in terms of Gold in the future and will still hold the parity between money supply and demand. James expects a price target of $10,000 for the future if this falls in line.

James new book The New Case for Gold is available in stores and online now and provides an in-depth analysis on the old and new reasons for why Gold is a necessity in our upcoming monetary system. As always for more analysis and interviews follow us on twitter @FRAuthority or Subscribe to our YouTube channel, Financial Repression Authority for weekly interviews. Abstract Writer: Saad Gohir [email protected] Video Editor: Min Jung Kim [email protected]

|

|||

2011 2012 2013 2014 |

|

||

I - POLITICAL |

|||

CENTRAL PLANNING - SHIFTING ECONOMIC POWER - STATISM

MACRO MAP - EVOLVING ERA OF CENTRAL PLANNING

|

G | THEME | |

| - - CRISIS OF TRUST - Era of Uncertainty | G | THEME | |

CORRUPTION & MALFEASANCE - MORAL DECAY - DESPERATION - RESENTMENT. |

US | THEME PAGE |  |

| - - SECURITY-SURVEILLANCE COMPLEX - STATISM | G | THEME | |

| - - CATALYSTS - FEAR (POLITICALLY) & GREED (FINANCIALLY) | G | THEME | |

II-ECONOMIC |

|||

| GLOBAL RISK | |||

| - GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | G | THEME | |

| - - SOCIAL UNREST - INEQUALITY & A BROKEN SOCIAL CONTRACT | US | THEME | |

| - - ECHO BOOM - PERIPHERAL PROBLEM | M | THEME | |

| - -GLOBAL GROWTH & JOBS CRISIS | |||

| - - - PRODUCTIVITY PARADOX - NATURE OF WORK | THEME | MA w/ CHS |

|

| 01-08-16 | THEME | MA w/ CHS |

|

| - - - STANDARD OF LIVING - EMPLOYMENT CRISIS, SUB-PRIME ECONOMY | US | THEME | MA w/ CHS |

III-FINANCIAL |

|||

|

FLOWS - Capital, Liqudity & Credit Flows

|

MATA RISK ON-OFF |

THEME |

w/ R Duncan |

| CRACKUP BOOM - ASSET BUBBLE | 12-31-15 | THEME | |

| SHADOW BANKING - LIQUIDITY / CREDIT ENGINE | M | THEME | |

| GENERAL INTEREST |

|

||

| STRATEGIC INVESTMENT INSIGHTS - Weekend Coverage | |||

|

|||

|

SII | ||

|

SII | ||

|

SII | ||

|

SII | ||

| TO TOP | |||

Read More - OUR RESEARCH - Articles Below

Tipping Points Life Cycle - Explained

Click on image to enlarge

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

�

TO TOP