As Ellington pointed out, "We believe that we are now at the end of the "over-investment" phase of the corporate credit cycle in the US that has been playing out since the depths of the GFC. This view is supported by a number of telltale signs of a reversal in the credit cycle:

Worsening Fundamentals - Declining corporate pro ts, record levels of corporate leverage, and an elevated high yield share of total corporate debt issuance

Defaults/Downgrades - Credit rating downgrades at a pace not seen since 2009

Falling Asset Prices - Price deterioration in the lowest quality loans and the most junior CLO tranches

Tightening Lending Standards - Weak investor appetite for new distressed debt issues, declines in CLO and CCC HY bond issuance, and tightening in domestic bank lending standards

Today, the Deutsche Bank credit strategy team led by Oleg Melentyev, in its "Year-Ahead Outlook 2016" report proves beyond a doubt that not only has the credit cycle turned, but that the default cycle is at hand, initially for energy names ("a default cycle in commodity-related areas at this point is unavoidable, and the only real question here is whether it stays contained to those areas or extends itself to other sectors") and soon for most other sectors.

Here is Melentyev's unpleasant message for Yellen, who is now about to hike rates and launch a tightening cycle at precisely the time when should be easing further to take away from the pain that will be unleashed by an inevitable junk bond supernova.

The current credit cycle can be described as mature: it’s old enough, at almost five years, and extended itself far enough (55% debt growth) to be falling right in line with three cycles that came before it in the past 30 years. A widely publicized McKinsey1 study earlier this year estimated a total of new debt created since 2007 at $50trln, half of which came from EM and two-thirds from nonfinancial corporate issuers in DM and EM. Our research suggests that global debt growth rates have remained steady as a percentage of global GDP, at 64%.

A large portion of this funding went towards commodity-related projects, particularly in EM. Our own credit indexes also tell us the extent of exposure to commodities, which is roughly 40% in EM world, and close to 25% in DM. This debt was raised at a time when consensus firmly believed in the commodity super-cycle theory, which at this point we know was wrong. This leads us to believe that a default cycle in commodity-related areas at this point is unavoidable, and the only real question here is whether it stays contained to those areas or extends itself to other sectors.

Evidence we are looking at suggests there is a meaningful probability of seeing early stages of the next default cycle developing in non-commodity sectors as well. We have previously presented a set of indicators in the Evolution of the Default Cycle report in early October, suggesting that recent equity volatility spikes and a widening in highest-quality corporate spreads are potential triggers for tightening credit conditions. We further followed up in recent weeks by showing rare trends emerging in HY underperforming both equities and IG as well as CCCs underperforming BBs, both the types of market behavior usually seen around turning points in the cycle.

Behold the metastasis of the junk bond cancer:

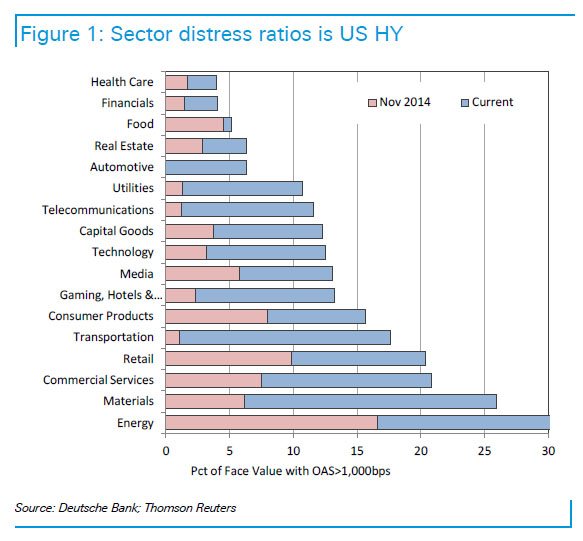

Figure 1 below shows how distress (bonds trading over 1,000bps) has been spreading across the HY space. From its starting point in energy a year ago, it has now reached other commodity-sensitive areas such as transportation, materials, capital goods, and commercial services. But it did not stop here and is also visible in places like retail, gaming, media, consumer staples, and technology – all areas that were widely expected to be insulated from low oil prices, if not even benefitting form them.

In other words, what was until a year ago a purely "energy" phenomenon is now an "everything" phenomenon, despite promises by every prominent economist that plunging energy prices are great news for the economy. As always happens, the economists were dead wrong once again.

It gets worse:

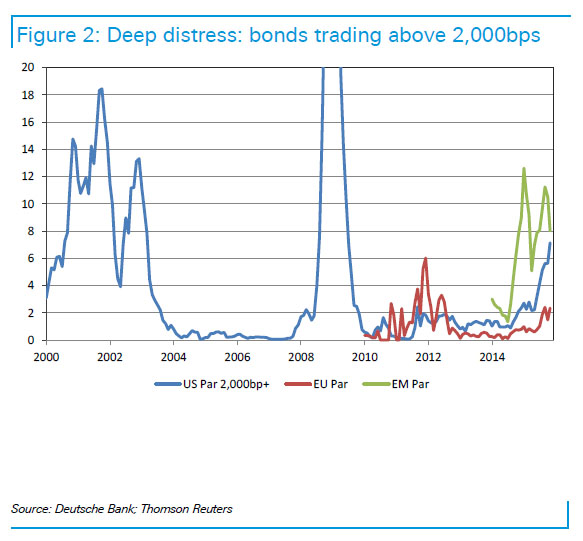

There is another interesting aspect of the distressed environment – overall distress ratio today, at 19% of face value of overall US HY – is only modestly higher than its level at the peak of Oct 2011 selloff (17%), and is comfortably inside of EU HY distress of 35% in early 2012. So one could argue that this level in and of itself is not meaningful, given that it misfired at least twice in recent years. We do not fully agree with such an argument, as it ignores the fact that 2011 and 2012 were still in early stages of the credit cycle, but we would give it 1/2 a credit for trying.

When we change the question and ask what percent of names are in deep distress today, defined here somewhat arbitrarily as 2,000bps (dollar prices around 50pts), the answer we get is 7.1%. This level is materially higher that 2% in US HY back in Oct 2011 or 6% in EU HY back in Jan 2012.

DB is very concerned at the implications of this:

Think about the significance of this number. While some names flirt with modest levels of distress from time to time throughout the normal course of events during the expansionary phase of a cycle, many of them stage comebacks and remain current on their debt obligations. In other words, not all distressed names today will default tomorrow. To witness, the total value of unique cusips in our DM HY index that ever touched on 1,000bps since 2009 through 2014 is $600bn. The actual grand total of defaults during this time is $135bn.

For that same timeframe, $130bn of unique bonds touched on a 2,000bp level. It’s also interesting to note that peak in deep-distress ratio in Figure 2 reflects peaks in actual default rates closely (18% deep distress par vs 20% par default rate in 2002 cycle, for example). It appears that few names ever come back from the deeply distressed levels, and their prevalence in today’s environment has to be taken seriously by credit investors. Ex-energy this metric currently stands at 3.1% of index face value.

Does the credit cycle precede the business cycle or vice versa? The answer: yes.

A generic push-back we hear on this view from time to time is this: how can you be expecting tighter credit conditions and higher default pressures when US economy is doing so well? Our answer is that one does not necessarily contradict the other. We strongly believe that credit cycle leads the business cycle, and as such it is not a pre-requisite to first see a slowing economy and only then to expect tightening in credit. In fact this turn of events would be quite unusual.

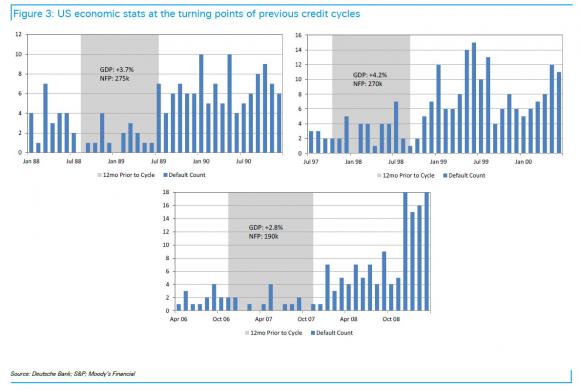

The simplest proof we can provide in support of this is shown in Figure 3 below, where as some of our readers would recognize, we are repeating charts from the cycle evolution piece, showing zoomed-in versions of turns in the past three credit cycles. The grayed-out areas are marking the last 12 months before such turns, and here were are also adding a snapshot of health of the US economy, on average, during those last 12 months. Numbers speak for themselves, but both real GDP growth and non-farm payrolls remain solid and stable during these short time windows.

This is not to suggest that macro environment is irrelevant; it clearly is. But it is important to remember that a stable and solid economy alone is not sufficient to suggest that a turn in credit conditions is impossible.

Deutsche Bank's conclusion:

Overall, all this evidence continues to suggest that default pressures are likely to start accumulating during 2016 even outside of commodity sectors. We forecast ex-commodity default rate to reach 3.5% among US HY issuers, up from the current level of 1.9%. Combined with commodity producers, we are looking at 5.75% overall US HY default rate.

None of which, of course, assumes short-term rates around 1% or higher: in that case the default rate will spike proportionately as the issuance window for even the most creditworthy issuers is practically closed.

Finally, where this imminent default cycle will have unexpected downstream consequences is on the balance sheets of the debt buyers themselves: moments ago SMRA reported that according to its Money Manager Survey, portfolio managers are holding the largest percentage of corporate bonds in history, with allocations rising to 35.8%, surpassing the previous record of 35.7%, seen last week, and 35.6% 2 weeks ago.

In other words, everyone is long and strong just as the bottom is on the verge of falling out of the market.

MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK -Dec 6th, 2015 - Dec 12th, 2015

BOND BUBBLE

1

RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates

2

GEO-POLITICAL EVENT

3

CHINA BUBBLE

4

JAPAN - DEBT DEFLATION

5

EU BANKING CRISIS

6

20 - RISING US Dollar

12-08-15

20

39 - FALLING Oil Price Pressures

12-08-15

39

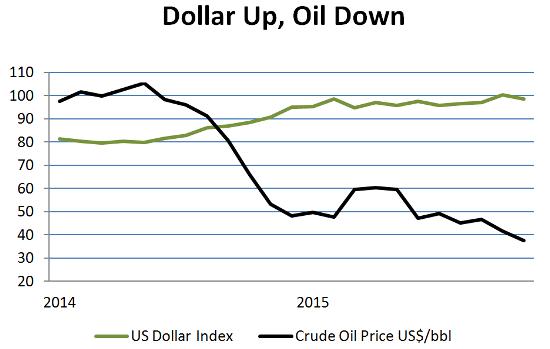

Falling Oil + Rising Dollar

= Crisis For A Whole Lot Of People

by John Rubino on December 7, 2015

Oil is plunging again, this time in the wake of OPEC’s inability to limit its members’ production. The US dollar, meanwhile, is up on the divergence between Fed tightening and ECB/BoJ/BoC easing.

This widening gap is a perfect storm for the many, many entities that have borrowed dollars to speculate in foreign currencies or drill for oil. Some examples:

(Bloomberg) – The commodity-price slump and the slowdown in China’s economy are crippling developing nations’ ability to borrow abroad, even as international debt sales from advanced nations remain at a five-year high.

Issuance by emerging-market borrowers slumped to a net $1.5 billion in the third quarter, a drop of 98 percent from the second quarter, according to the Bank for International Settlements. That was the biggest downtrend since the 2008 financial crisis and reduced global sales of securities by almost 80 percent, the BIS said in a report.

Emerging-market assets tumbled in the third quarter, led by the biggest plunge in commodity prices since 2008 and China’s surprise devaluation of the yuan. The average yield on developing-nation corporate bonds posted the biggest increase in four years, stocks lost a combined $4.2 trillion and a gauge of currencies slid 8.3 percent against the dollar. Sanctions on Russian entities and political turmoil in Brazil and Turkey also affected sales by companies in those countries.

(CNBC) – After years of safely reaching for yield through risky assets like stocks and speculative-grade bonds, Wall Street is heading into 2016 rethinking the strategy.

That trend of low defaults has begun to turn the other way, with the trailing 12-month rate rising to 2.8 percent in November, the highest level in three years, according to ratings agency S&P, which expects defaults to climb to 3.3 percent by Sept. 30, 2016.

Moreover, fellow ratings agency Moody’s reported its liquidity stress index in November hit its highest rate since February 2010. Still more troubling is that some of the damage has begun to spill outside the oil, gas and mining sectors, where most of the defaults had been contained.

Fully one-third of oil and gas and mining and metals companies in Moody’s coverage universe are on review for downgrade or have negative outlooks.

(Bloomberg) – Amid Brazil’s economic and political tumult, the nation’s businesses have seen a record number of downgrades this year — and the total is about to get worse.

Fitch Ratings estimates it may slash the ratings of as many as 10 companies for every one it upgrades in 2016. Fitch said that grim scenario is most likely if it chops Brazil’s grade, an ever-growing possibility as the country’s woes deepen.

A top lawmaker initiated impeachment proceedings against President Dilma Rousseff last week, a move that may further undermine the nation’s finances and exacerbate the worst recession in a quarter century. That spells trouble for companies already finding it hard to obtain financing in the wake of an unprecedented corruption scandal at Brazil’s state oil company.

“You will see companies burning cash,” Fitch’s Carvalho said. “The cross-border market is closed for Brazilian companies, and the local market is selective.”

(CNBC) – If Saudi Arabia maintains oil production at current levels amid the oil price crash, then it’s going to have to cut its budget — or it will likely be bankrupt by the end of the decade. The big issue is Saudi Arabia’s big spending ways, especially increased government spending on social welfare programs.

According to the IMF, government expenditures in Saudi Arabia are expected to reach 50.4 percent of GDP in 2015, up from 40.8 percent in 2014. That increase can be attributed to two things: falling oil prices (it’s bringing in less revenue) and an inflated budget (it’s spending more money).

It’s no secret that a large portion of Saudi Arabia’s roughly 30 million people rely on the government for economic support. In February, the newly crowned King Salman doled out a reported $32 billion to the Saudi people in bonuses and subsidies to celebrate his ascension to the throne.

“We are a welfare society, so the population depends a lot on government subsidies, directly and indirectly,” Abdullah Al-Alami, a Saudi writer and economist, recently told The New York Times. “But one day we are going to run out of oil, and I don’t believe it is wise to be pampered and subsidized.”

To summarize, the world is entering a classic credit crunch, in which lending dries up for marginal borrowers first before tightening for core entities like multinational corporations and developed world governments. And it’s just beginning.

Most of today’s crises evolved with oil considerably higher and the dollar somewhat lower, so current conditions are actually a lot worse than those that, for instance, caused emerging market debt issuance to evaporate and shoved Brazil into existential crisis.

And since oil overproduction will likely to continue while the differences in central bank policies are etched in stone for the next few months at least, it’s possible that the performance gap between oil and the dollar will widen going forward. This will turbo-charge today’s crises and add a few more, as oil producing US states hit financial walls and big chunks of the developing world follow Brazil down the drain.

TO TOP

MACRO News Items of Importance - This Week

GLOBAL MACRO REPORTS & ANALYSIS

US ECONOMIC REPORTS & ANALYSIS

CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES

Global equity markets, as measured by the MSCI Developed World index, are above the lows hit in early October but remain on a downtrend that began after markets peaked at the end of May this year.

As SocGen's Andrew Lapthorne notes, the current level is now only just above where the index stood at the beginning of 2013 and less than 1% above the 2007 peak. In other words, as he warns, "the equity market has run out of momentum," and the 'bill' for the debt overhang is coming due.

The recovery since 2007 has been very one-sided with only Denmark, Switzerland and the US indices exceeding their October 2007 US dollar price levels.

The UK is down 34% in US dollar terms and the MSCI Eurozone is 40% down. The reasons for this weak performance is fairly clear, unlike Japan neither the UK or Eurozone have experienced an earnings recovery in either US dollar terms or in local currency terms. Profits in both regions are still 45-55% down from the 2007 high according to MSCI reported profits.

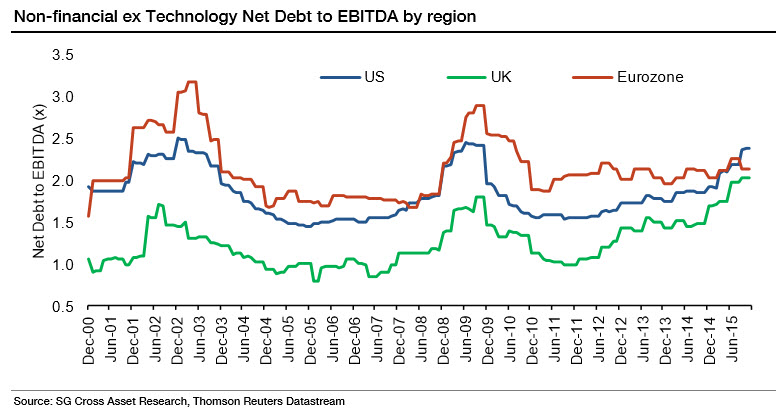

The Eurozone of course has many problems, but at least Eurozone companies have not been boosting leverage as a consequence of disappointing profits, as is the case in the US and apparently the UK as well! As we have remarked upon on numerous occasions, the US equity market has been boosting leverage with record levels of debt-financed share buybacks, resulting in a significant increase in leverage among US corporates.

However with all the focus on the US, many investors may have missed the major corporate debt problem now emerging in the UK stock market. Devoid of the headline-grabbing buybacks, many may not have noticed that both nominal net debt and net debt to EBITDA have never been higher in the UK.

The bulk of that increase has come from a huge rise in Mining sector debt at a time when profits have collapsed, but leverage ratios in other sectors are also elevated. The US is not the only market now facing a corporate debt overhang.

Source: SocGen

COMMODITY CORNER - AGRI-COMPLEX

PORTFOLIO

SECURITY-SURVEILANCE COMPLEX

PORTFOLIO

THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur

FRA Co-Founder Gordon T. Long interviews Brett Rentmeester on Austrian economics and the importance of having an entrepreneurial mindset in investment. Brent Rentmeester is the president of Windrock Wealth Management and has been in the wealth asset management for over 18years. Mr Rentmeester believes the uniqueness of Windrock is its focus on the macroeconomic picture, Austrian economics and what it all means for investment implications as well as an entrepreneurial mindset on how to find investment opportunities.

The Austrian school to him is the “acknowledgement of the influence that central banks have on the business cycle and interest rate and therefore the opportunities left for investment”.

He mentions that the traditional stock, bond portfolio is under a lot of challenge going forward because there is no real and safe income anywhere today. As a result people are becoming speculators and risk takers even when they don’t want to.

Brett believes having an entrepreneur mindset when investing, is the key to addressing the dilemma of income and the future of investment. Secure private lending is lending money to borrowers that is backed by real tangible assets or an income stream. According to him, what makes this a unique category is that it addresses the pockets of lending that is being neglected by the big banks as a result of the financial banking distress that took place in 2008.

On examples of secure private lending, Brett highlights 3 different categories with his examples. He explains that in auctioned rental properties, the government organizations Fannie Mae and Freddie Mac by law are restricted from buying mortgages on such properties until after 2 years, this results in a niche market for private lenders. “In energy markets more states are moving towards a deregulated market”. What this means is that a consumer can buy energy from a variety of energy companies. Now this system is facilitated by third party brokers who go door to door offering this energy from various energy companies. Now because the brokers want the commissions up front and the energy companies can’t provide it, we see people coming in to pay the brokers a discounted fee upfront and then agree to collect the 3year contract provided by the energy companies.

Trade financing

“Global trade happens between different parties but often times it’s financed by big banks, trade receivables. So one party needs to buy goods and a supplier supplies them but someone’s got to finance that transaction and it’s often the third party bank”.

Due to new regulations, banks are required to reserve more capital in such situations, as a result an opportunity is created for private money to finance the transaction between the customer and supplier.

“Rather than taking on more risk you don’t have to today, you just have to be more creative”

– Gordon. T. Long.

Brett echoes this sentiment saying:

“So much of the industry and investors think in a very narrow box of stocks, bonds and maybe hedge funds but there’s a lot of things outside of that, that if you open your mind to the opportunities, are quite interesting to research”.

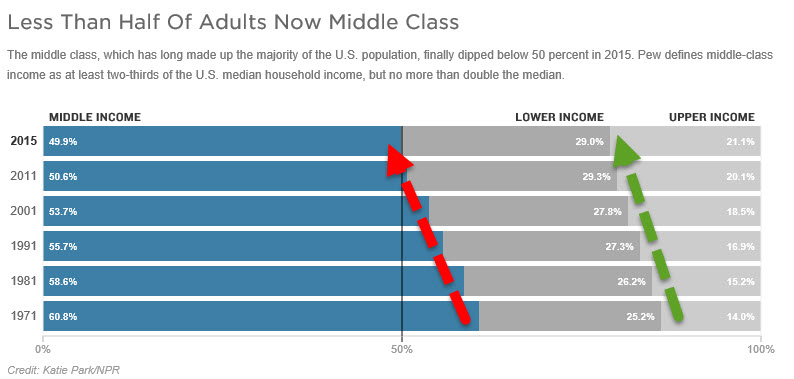

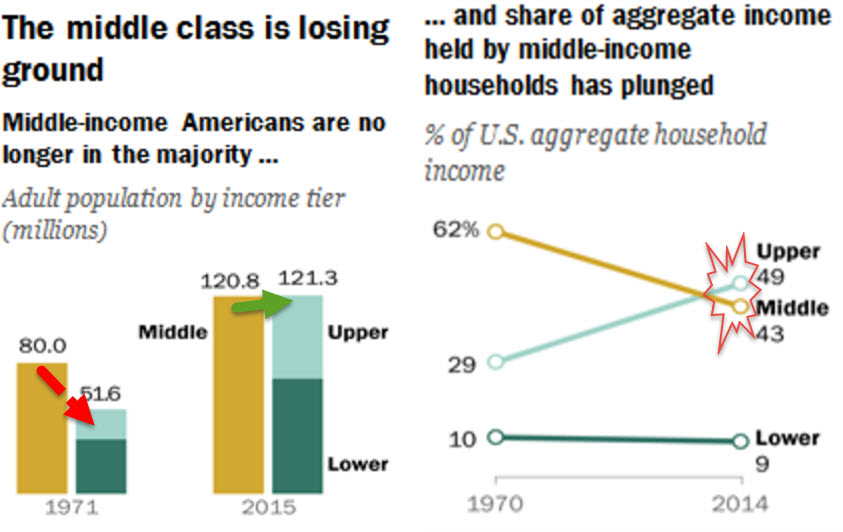

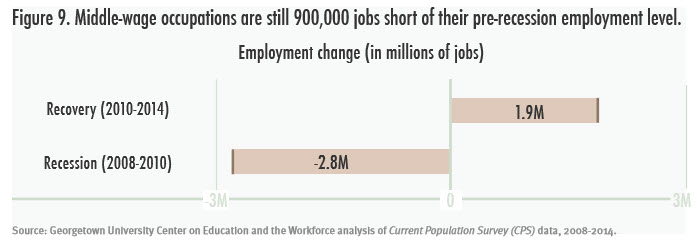

Back in 1971, about 2 out of 3 Americans lived in middle-income households. Since then, the middle has been steadily shrinking.

Today, just a shade under half of all households (about 49.9 percent) have middle incomes. Slightly more than half of Americans (about 50.1 percent) either live in a lower-class household (roughly 29 percent) or an upper-class household (about 21 percent).

As NPR explains, thanks to factory closings and other economic factors, the country now has 120.8 million adults living in middle-income households, the study found. That compares with the 121.3 million who are living in either upper- or lower-income households.

"The hollowing of the middle has proceeded steadily for the past four decades," Pew concluded.

And middle-income Americans not only have shrunk as a share of the population but have fallen further behind financially, with their median income down 4 percent compared with the year 2000, Pew said.

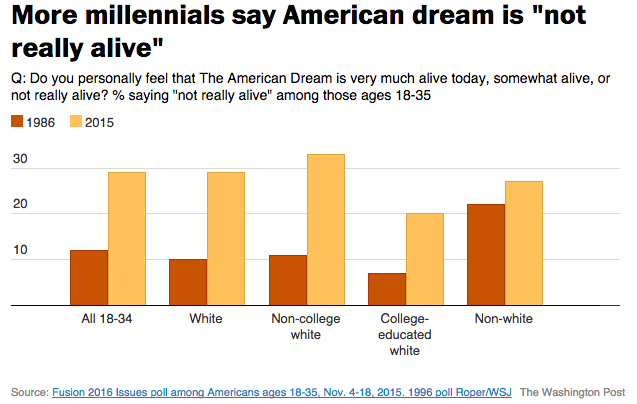

And if you’re a millennial, you’d be forgiven for being disillusioned with the American dream.As we recently noted, compared to young Americans in 1986, you’re three times as likely to think the American dream is dead and buried. As WaPo notes, "young workers today are significantly more pessimistic about the possibility of success in America than their counterparts were in 1986, according to a new Fusion 2016 Issues poll - a shift that appears to reflect lingering damage from the Great Recession and more than a decade of wage stagnation for typical workers.”

It is only a matter of time before the middle class is wiped out and America begins to resemble the poverty, violence and tyranny so often associated with the countries from which many illegal migrants originate.

It appears that time is drawing near as Charles Hugh-Smith recently noted, the mainstream is finally waking up to the future of the American Dream: downward mobility for all but the top 10% of households.

Downward mobility and social defeat lead to social depression. Here are the conditions that characterize social depression:

1. High expectations of endless rising prosperity have been instilled in generations of citizens as a birthright.

2. Part-time and unemployed people are marginalized, not just financially but socially.

3. Widening income/wealth disparity as those in the top 10% pull away from the shrinking middle class.

4. A systemic decline in social/economic mobility as it becomes increasingly difficult to move from dependence on the state (welfare) or one's parents to financial independence.

5. A widening disconnect between higher education and employment: a college/university degree no longer guarantees a stable, good-paying job.

6. A failure in the Status Quo institutions and mainstream media to recognize social recession as a reality.

7. A systemic failure of imagination within state and private-sector institutions on how to address social recession issues.

8. The abandonment of middle class aspirations by the generations ensnared by the social recession: young people no longer aspire to (or cannot afford) consumerist status symbols such as luxury autos or homeownership.

9. A generational abandonment of marriage, families and independent households as these are no longer affordable to those with part-time or unstable employment, i.e. what I have termed (following Jeremy Rifkin) the end of work.

10. A loss of hope in the young generations as a result of the above conditions.

If you don't think these apply, please check back in a year. We'll have a firmer grasp of social depression in December 2016.

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you confirm the facts on your own before making important investment commitments.

THE CONTENT OF ALL MATERIALS: SLIDE PRESENTATION AND THEIR ACCOMPANYING RECORDED AUDIO DISCUSSIONS, VIDEO PRESENTATIONS, NARRATED SLIDE PRESENTATIONS AND WEBZINES (hereinafter "The Media") ARE INTENDED FOR EDUCATIONAL PURPOSES ONLY.

The Media is not a solicitation to trade or invest, and any analysis is the opinion of the author and is not to be used or relied upon as investment advice. Trading and investing can involve substantial risk of loss. Past performance is no guarantee of future returns/results. Commentary is only the opinions of the authors and should not to be used for investment decisions. You must carefully examine the risks associated with investing of any sort and whether investment programs are suitable for you. You should never invest or consider investments without a complete set of disclosure documents, and should consider the risks prior to investing. The Media is not in any way a substitution for disclosure. Suitability of investing decisions rests solely with the investor. Your acknowledgement of this Disclosure and Terms of Use Statement is a condition of access to it. Furthermore, any investments you may make are your sole responsibility.

THERE IS RISK OF LOSS IN TRADING AND INVESTING OF ANY KIND. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Gordon emperically recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, he encourages you confirm the facts on your own before making important investment commitments.

DISCLOSURE STATEMENT

Information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities.

Please note that Mr. Long may already have invested or may from time to time invest in securities that are discussed or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him.

FAIR USE NOTICEThis site contains

copyrighted material the use of which has not always been specifically

authorized by the copyright owner. We are making such material available in

our efforts to advance understanding of environmental, political, human

rights, economic, democracy, scientific, and social justice issues, etc. We

believe this constitutes a 'fair use' of any such copyrighted material as

provided for in section 107 of the US Copyright Law. In accordance with

Title 17 U.S.C. Section 107, the material on this site is distributed

without profit to those who have expressed a prior interest in receiving the

included information for research and educational purposes.

If you wish to use

copyrighted material from this site for purposes of your own that go beyond

'fair use', you must obtain permission from the copyright owner.

{kind=link}