|

JOHN RUBINO'SLATEST BOOK |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

Mon. May 11th, 2015

Follow Our Updates

on TWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

STRATEGIC INVESTMENT INSIGHTS

2015 THESIS: FIDUCIARY FAILURE

2015 THESIS: FIDUCIARY FAILURE

NOW AVAILABLE FREE to Trial Subscribers

174 Pages

What Are Tipping Poinits?

Understanding Abstraction & Synthesis

Global-Macro in Images: Understanding the Conclusions

![]()

| MAY | ||||||

| S | M | T | W | T | F | S |

| 1 | 2 | |||||

| 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| 10 | 11 | 12 | 13 | 14 | 15 | 16 |

| 17 | 18 | 19 | 20 | 21 | 22 | 23 |

| 24 | 25 | 26 | 27 | 28 | 29 | 30 |

| 31 | ||||||

KEY TO TIPPING POINTS |

| 1- Bond Bubble |

| 2 - Risk Reversal |

| 3 - Geo-Political Event |

| 4 - China Hard Landing |

| 5 - Japan Debt Deflation Spiral |

| 6- EU Banking Crisis |

| 7- Sovereign Debt Crisis |

| 8 - Shrinking Revenue Growth Rate |

| 9 - Chronic Unemployment |

| 10 - US Stock Market Valuations |

| 11 - Global Governance Failure |

| 12 - Chronic Global Fiscal ImBalances |

| 13 - Growing Social Unrest |

| 14 - Residential Real Estate - Phase II |

| 15 - Commercial Real Estate |

| 16 - Credit Contraction II |

| 17- State & Local Government |

| 18 - Slowing Retail & Consumer Sales |

| 19 - US Reserve Currency |

| 20 - US Dollar Weakness |

| 21 - Financial Crisis Programs Expiration |

| 22 - US Banking Crisis II |

| 23 - China - Japan Regional Conflict |

| 24 - Corruption |

| 25 - Public Sentiment & Confidence |

| 26 - Food Price Pressures |

| 27 - Global Output Gap |

| 28 - Pension - Entitlement Crisis |

| 29 - Central & Eastern Europe |

| 30 - Terrorist Event |

| 31 - Pandemic / Epidemic |

| 32 - Rising Inflation Pressures & Interest Pressures |

| 33 - Resource Shortage |

| 34 - Cyber Attack or Complexity Failure |

| 35 - Corporate Bankruptcies |

| 36 - Iran Nuclear Threat |

| 37- Finance & Insurance Balance Sheet Write-Offs |

| 38- Government Backstop Insurance |

| 39 - Oil Price Pressures |

| 40 - Natural Physical Disaster |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

![]()

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

![]()

Charles Hugh Smith's Latest Books

![]()

![]()

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

![]()

![]()

![]()

![]()

![]()

OTHERS OF NOTE

![]()

![]()

![]()

![]()

Book Review- Five Thumbs Up

for Steve Greenhut's

Plunder!

![]()

![]()

TODAY'S TIPPING POINTS

|

![]() Scroll TWEETS for LATEST Analysis

Scroll TWEETS for LATEST Analysis ![]()

HOTTEST TIPPING POINTS |

Theme Groupings |

|||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro |

||||

"BEST OF THE WEEK "

|

Posting Date |

Labels & Tags | TIPPING POINT or THEME / THESIS or INVESTMENT INSIGHT |

|

|

MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

|||

AN EARNIGS RECESSION - No Pricing Power Due to an Excess Debt Payments Drain As we write the US stock market, as measured by the S&P 500 and Nasdaq Composite Index, hovers at or near new highs. We will take this as an opportunity to reiterate that this is a bubble that is the direct creation of the Federal Reserve. We continue to refer to this phenomenon as the “Central Bank Bubble”. EARNINGS RECESSION Just under one year ago, analysts were estimating S&P 500 operating earnings to increase for the first quarter of 2015 by over 10%. That number is now substantially lower and has gone negative for the entire index.

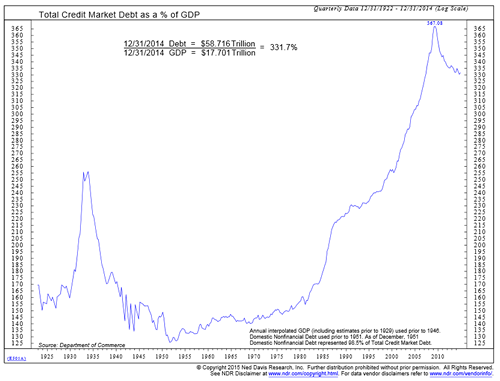

We agree with the former and strongly disagree with the latter. But whether attributed to weather, the west coast port strike, or dollar strength, the fact remains that for whatever the reason, two declining quarters constitutes an “earnings recession”. We have had 13 “earnings recessions” since 1945, and all but three of those have led to an economic recession. We continue to believe corporate earnings will not grow as a whole at a meaningfully different rate than US Gross Domestic Product (GDP), as corporate earnings are a proxy for economic growth. Growth in the economy, in turn, is heavily influenced by “Total Credit Market Debt”, which is the sum of government, corporate and household debt. Only at the time of the great depression of the 1930’s has “Total Credit Market Debt” been greater than 200% of GDP in the United States (see attached chart from Ned Davis Research)).

That is, of course, until the middle 1980’s when this metric again penetrated that barrier. After that time it went on an inexorable march to a whopping 367% of GDP just prior to the bursting of the “Housing Bubble” and stood at just under 332% as of the end of 2014. The level of debt continues to be a headwind to economic growth that will persist until the debt is paid down. FED BUBBLE - Flawed Policy What has acted to somewhat mask this headwind is, what we believe, is the most reckless policy ever adopted by the Fed. The Fed was wrong on the “Dot Com Bubble”; was wrong on the “Housing Bubble”; and we believe will be wrong in the creation of the current “Central Bank Bubble”. This Fed is in a major experimentation mode which is very dangerous. The policy of which we speak is, of course, Zero Interest Rate policy, or (ZIRP). This policy has driven the Fed’s Balance Sheet from $800 billion in 2008 to $4.4 trillion currently. It is because of ZIRP that stocks do not appear, to some, to be expensive. After all, if the alternative is a 2% ten year treasury or 2.6% thirty year treasury, maybe a 2% dividend yield isn’t so bad; or so the thinking goes. But as stated above, the growth in corporate profits in the long run is a proxy for the growth in the economy, or GDP. And right now stocks, measured by market capitalization, are near the highest they have ever been relative to GDP. Every major market bottom and top has been coincident with very low or very high ratios of “Stock Market Capitalization to GDP”(see attached chart from Ned Davis Research).

It is likely the reason is that this metric has purported to be a favorite of Warren Buffet. In fact, the only time this metric has been higher was just before the” Dot Com Bubble” burst. It comes at a time when deflation is playing out all over the world. The dollar is strengthening, which hinders multinational companies from exporting goods abroad. In addition, it appears that companies do not have enough pricing power to increase margins. LIQUIDITY TRAP We at Comstock have been telling our viewers that we have been in a deflationary environment for years. It seems the markets now are agreeing with us as there are currently few countries that are expecting any material inflation over the next ten years. This is evident by the yields in ten year sovereign paper. The following are yields as of the date of this writing:

What all of these countries have in common, in addition to being democracies, is that their respective central banks are in a “Liquidity Trap” situation, where low and even negative interest rates do not encourage consumer spending but rather consumer savings. Businesses in turn do not have the confidence to invest in new plant and equipment. This is particularly true in the United States, where the average age of private fixed assets is the oldest in the past fifty years. So, to our viewers we say, we have been early on this, as we were with the Dot Com and Housing Bubbles, but we are confident this will end the same way as those bubbles. The US stock market is historically expensive and financial assets have been inflated by an experimental central bank policy. It is an error that is now being repeated by central banks in Europe, Japan and just recently, China. These markets are being influenced in similar ways as ours, rather than fiscal and tax policies that would stimulate sustainable growth. We will hold our view that stocks are expensive until they become priced more reasonably relative to the growth prospects of the economy. We have maintained consistently that high levels of debt are the main problem affecting growth and those debt levels will not be going away any time soon. A SUPPORTING RESEARCH PAPER BY THE BIS Leverage dynamics and the real burden of debt

In addition to leverage, the aggregate debt service burden is an important link between financial and real developments. Using US data from 1985 to 2013, we find that it has sizable negative effects on credit and expenditure growth. Strong interactions between leverage and the debt service burden lead to large and protracted cycles in credit and expenditure that match the stylised facts of credit booms and busts. Even with real-time estimates, the predicted adjustment to leverage and the debt service burden from 2005 onwards imply paths for credit and expenditure that closely match actual developments before and during the Great Recession.

|

05-11-15 | STUDY | ||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - May 10th, 2015 - May. 16th, 2015 | ||||

| BOND BUBBLE | 1 | |||

| RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates | 2 | |||

| GEO-POLITICAL EVENT | 3 | |||

| CHINA BUBBLE | 4 | |||

| JAPAN - DEBT DEFLATION | 5 | |||

EU BANKING CRISIS |

6 |

|||

| TO TOP | ||||

| MACRO News Items of Importance - This Week | ||||

GLOBAL MACRO REPORTS & ANALYSIS |

||||

US ECONOMIC REPORTS & ANALYSIS |

||||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | ||||

| Market | ||||

| TECHNICALS & MARKET |

|

|||

| COMMODITY CORNER - AGRI-COMPLEX | PORTFOLIO | |||

| SECURITY-SURVEILANCE COMPLEX | PORTFOLIO | |||

| THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur | ||||

| 2015 - FIDUCIARY FAILURE | 2015 | THESIS 2015 |  |

|

| 2014 - GLOBALIZATION TRAP | 2014 |  |

||

|

||||

|

2013 2014 |

|

|||

2011 2012 2013 2014 |

|

|||

| THEMES - Normally a Thursday Themes Post & a Friday Flows Post | ||||

I - POLITICAL |

||||

| CENTRAL PLANNING - SHIFTING ECONOMIC POWER - STATISM | G | THEME | ||

| - - CORPORATOCRACY - CRONY CAPITALSIM | THEME |  |

||

- - CORRUPTION & MALFEASANCE - MORAL DECAY - DESPERATION, SHORTAGES. |

THEME |  |

||

| - - SECURITY-SURVEILLANCE COMPLEX - STATISM | M | THEME | ||

| - - CATALYSTS - FEAR (POLITICALLY) & GREED (FINANCIALLY) | G | THEME | ||

II-ECONOMIC |

||||

| GLOBAL RISK | ||||

| - GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | G | THEME | ||

| - - SOCIAL UNREST - INEQUALITY & A BROKEN SOCIAL CONTRACT | US | THEME | ||

| - - ECHO BOOM - PERIPHERAL PROBLEM | M | THEME | ||

| - -GLOBAL GROWTH & JOBS CRISIS | ||||

| - - - PRODUCTIVITY PARADOX - NATURE OF WORK | THEME | MACRO w/ CHS |

||

| - - - STANDARD OF LIVING - EMPLOYMENT CRISIS, SUB-PRIME ECONOMY | US | THEME | MACRO w/ CHS |

|

III-FINANCIAL |

||||

| FLOWS -FRIDAY FLOWS | MATA RISK ON-OFF |

THEME |  |

|

| CRACKUP BOOM - ASSET BUBBLE | THEME | |||

| SHADOW BANKING - LIQUIDITY / CREDIT ENGINE | M | THEME | ||

| GENERAL INTEREST |

|

|||

| STRATEGIC INVESTMENT INSIGHTS - Weekend Coverage | ||||

|

SII | |||

|

SII | |||

|

SII | |||

|

SII | |||

| TO TOP | ||||

Read More - OUR RESEARCH - Articles Below

Tipping Points Life Cycle - Explained

Click on image to enlarge

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

�

TO TOP