|

JOHN RUBINO'SLATEST BOOK |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

Fri Apr. 17th, 2015

Follow Our Updates

on TWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

STRATEGIC INVESTMENT INSIGHTS

2015 THESIS: FIDUCIARY FAILURE

2015 THESIS: FIDUCIARY FAILURE

NOW AVAILABLE FREE to Trial Subscribers

174 Pages

What Are Tipping Poinits?

Understanding Abstraction & Synthesis

Global-Macro in Images: Understanding the Conclusions

![]()

| APRIL | ||||||

| S | M | T | W | T | F | S |

| 1 | 2 | 3 | 4 | |||

| 5 | 6 | 7 | 8 | 9 | 10 | 11 |

| 12 | 13 | 14 | 15 | 16 | 17 | 18 |

| 19 | 20 | 21 | 22 | 23 | 24 | 25 |

| 26 | 27 | 28 | 29 | 30 | ||

KEY TO TIPPING POINTS |

| 1- Bond Bubble |

| 2 - Risk Reversal |

| 3 - Geo-Political Event |

| 4 - China Hard Landing |

| 5 - Japan Debt Deflation Spiral |

| 6- EU Banking Crisis |

| 7- Sovereign Debt Crisis |

| 8 - Shrinking Revenue Growth Rate |

| 9 - Chronic Unemployment |

| 10 - US Stock Market Valuations |

| 11 - Global Governance Failure |

| 12 - Chronic Global Fiscal ImBalances |

| 13 - Growing Social Unrest |

| 14 - Residential Real Estate - Phase II |

| 15 - Commercial Real Estate |

| 16 - Credit Contraction II |

| 17- State & Local Government |

| 18 - Slowing Retail & Consumer Sales |

| 19 - US Reserve Currency |

| 20 - US Dollar Weakness |

| 21 - Financial Crisis Programs Expiration |

| 22 - US Banking Crisis II |

| 23 - China - Japan Regional Conflict |

| 24 - Corruption |

| 25 - Public Sentiment & Confidence |

| 26 - Food Price Pressures |

| 27 - Global Output Gap |

| 28 - Pension - Entitlement Crisis |

| 29 - Central & Eastern Europe |

| 30 - Terrorist Event |

| 31 - Pandemic / Epidemic |

| 32 - Rising Inflation Pressures & Interest Pressures |

| 33 - Resource Shortage |

| 34 - Cyber Attack or Complexity Failure |

| 35 - Corporate Bankruptcies |

| 36 - Iran Nuclear Threat |

| 37- Finance & Insurance Balance Sheet Write-Offs |

| 38- Government Backstop Insurance |

| 39 - Oil Price Pressures |

| 40 - Natural Physical Disaster |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

![]()

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

![]()

Charles Hugh Smith's Latest Books

![]()

![]()

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

![]()

![]()

![]()

![]()

![]()

OTHERS OF NOTE

![]()

![]()

![]()

![]()

Book Review- Five Thumbs Up

for Steve Greenhut's

Plunder!

![]()

![]()

TODAY'S TIPPING POINTS

|

![]() Scroll TWEETS for LATEST Analysis

Scroll TWEETS for LATEST Analysis ![]()

HOTTEST TIPPING POINTS |

Theme Groupings |

|||||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro |

||||||

"BEST OF THE WEEK "

|

Posting Date |

Labels & Tags | TIPPING POINT or THEME / THESIS or INVESTMENT INSIGHT |

|||

|

MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

|||||

|

||||||

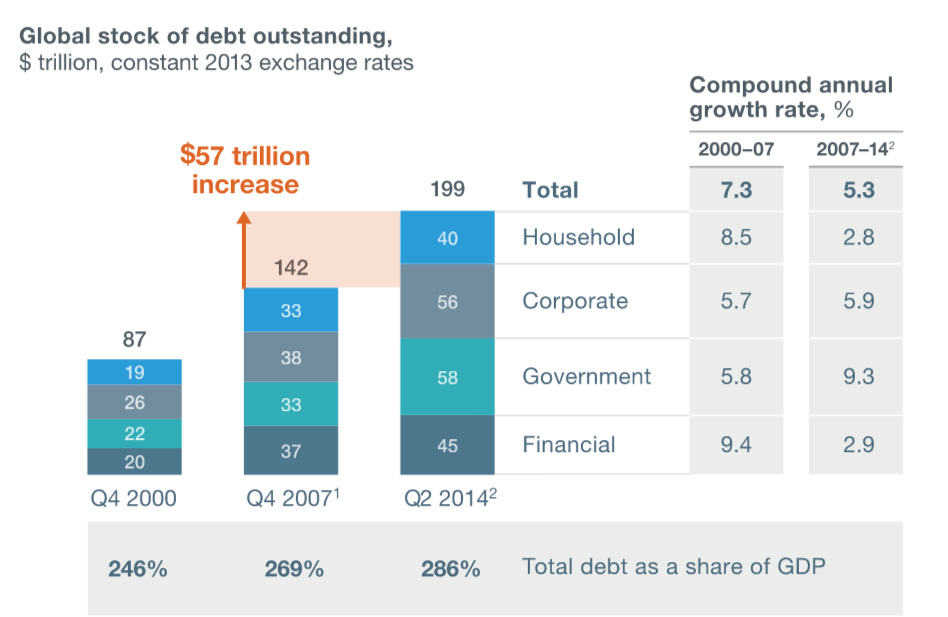

FLOWS - Liquidity, Credit & Debt RICHARD DUNCAN'S LATEST 04-15-15 Central Banks have effectively cancelled trillions of Dollars of government debt and are in the process of cancelling trillions more. When a central bank creates money and buys a government bond, it is the same thing as cancelling that bond - so long as the central bank does not sell the bond and so long as it rolls it over when the bond matures. In other words, Quantitative Easing cancels government debt. That means the United States, the UK and Japan have far less government debt than is generally understood. The same will soon be true for the Eurozone governments. This has important policy implications that the world cannot afford to ignore. The Federal Reserve has acquired $2.5 trillion of US government securities, nearly 14% of all US government debt. The US Treasury Department pays interest on that debt to the Fed. Then, at the end of every year, the Fed turns around and gives its profits to the Treasury, including the profits from the interest income earned on its government debt holdings. Last year, the US central bank gave the US government $97 billion, reducing the budget deficit by nearly 20%. It has given the government $500 billion since 2008. In other words, on the bonds held by the Fed, the government is paying interest to itself, which is the same thing as not paying any interest. Bonds that do not pay interest have been effectively cancelled. Seen in this light, the ratio of government debt to GDP in the United States is not 105%. It is 89%. The UK government is paying interest to itself on the £375 billion of government debt owned by the Bank of England. That is 24% of all UK government debt. Since the Bank of England is unlikely to ever sell those bonds the ratio of government debt to GDP in the UK is actually 70%, rather than 92%, as it is now reported to be. The Bank of Japan owns Japanese government bonds equivalent to 53% of GDP and it is acquiring new government bonds at roughly twice the pace that the government is selling them. When it is understood that Quantitative Easing is debt cancellation, the BOJ’s very aggressive QQE program makes sense. It may be the only way to prevent a fiscal crisis in Japan, where government debt is reported to be 245% of GDP. The more government debt acquired (and effectively cancelled) by the central bank, the less likely a fiscal crisis will be. Fiat money creation on a large scale was supposed to cause very high rates of inflation, or even hyperinflation. It hasn’t because it has taken place at the same time that Globalization has been driving down the cost of labor in the developed economies. Under the Bretton Woods system, when trade between nations had to balance, aggressive fiat money creation would have over-stimulated the US economy (for instance), quickly leading to full employment, full capacity utilization and wage-push inflation. Under the Dollar Standard, trade no longer has to balance; so all domestic bottlenecks can be circumvented by buying from abroad. In our new global economy, two billion people live on less than $3 per day. That means we will not hit capacity constraints in labor, leading to wage inflation, for decades. And that, as the history of the past six years demonstrates, means that the central banks of the developed economies can create money and finance massive government budget deficits without causing inflation. This combination of fiat money and Globalization under the Dollar Standard creates a once-in-history opportunity. The government debt owned by the central banks should be held permanently and perpetually rolled over, effectively cancelling it. It would then be clear that governments really have much less debt than is generally understood. The governments of the developed nations could then borrow more and invest that money in new industries and technologies to restructure their economies and to retrain and educate their workforce at the post-graduate level to ensure that the standard of living in the developed world continues to improve, rather than sinking down to third world levels. Furthermore, large investments in green technologies could be financed with GQE, Green Quantitative Easing, perhaps preventing an environmental catastrophe. Heretical as it may appear at first impression, Quantitative Easing has already effectively cancelled trillions of dollars of government debt without causing inflation. At the very least, this fact completely undermines the case in favor of further growth retarding fiscal austerity. If this opportunity were fully exploited, investments could be financed that would not only restore global growth but that would also improve the wellbeing of everyone on this planet. For all the details on how QE cancels government debt, watch this free Macro Watch video: http://www.richardduncaneconomics.com/qe-is-debt-cancellation-free-video/

If you are a subscriber to my video-newsletter, Macro Watch, log in and learn how the crisis in the global economy will affect you. If not, join here: http://www.gordontlong.com/RichardDuncan/Macrowatch.htm For a 55% subscription discount, hit the “Click Here to Subscribe Now” tab and use the coupon code: flows

|

04-17-15 | THMES FLOWS |

FLOWS |

|||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - April 12th, 2015 - Apr. 18th, 2015 | ||||||

| RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates | 1 | |||||

| CHINA BUBBLE | 2 | |||||

| JAPAN - DEBT DEFLATION | 3 | |||||

| BOND BUBBLE | 4 | |||||

EU BANKING CRISIS |

5 |

|||||

| SOVEREIGN DEBT CRISIS [Euope Crisis Tracker] | 6 | |||||

DE-DOLLARIZATION - AIIB & The Beginning of the End China Takes Aim At Dollar Reserve Status: Promotes Yuan In Investment Bank 04-15-15 As regular readers know, we’ve variously described the China-led Asian Infrastructure Investment Bank as representing both an attempt by China to

Essentially the AIIB will (either intentionally or unintentionally depending on who you believe) serve as an instrument of Chinese foreign policy and any hope of keeping this between the people who are privy to the country’s various hidden agendas (because all countries have agendas), went out the window early last month when the UK staged a coup by breaking with Washington and joining the development bank triggering a flood of applications from Western countries and culminating in membership bids from US “allies” Australia, Israel, and even Canada. Adding insult to injury, the AIIB is now looking to hire officials away from the World Bank and rival ADB. Amid the March membership frenzy, Beijing sought to play down the degree to which the venture would serve to help establish a new world economic order with China at the helm. An article which appeared in The Global Times (a paper run by the state-controlled People’s Daily) very specifically denied any notion that China has designed on establishing a yuan-based global economic system. Here’s an excerpt:

Perhaps, but as we noted at the time, it was on the very same day that the following came across the wires: “China plans to push for yuan to take prominence in loans under the Asian Infrastructure Investment Bank and the Silk Road Fund, people familiar with the matter said. China may encourage $100b AIIB and $40b Silk Road Fund to issue loans directly in yuan or set up yuan-denominated funds under the two institutions, according to the people, who ask not to be identified because deliberations are private.” This prompted us to suggest that “actions speak louder than words.” Today, The South China Morning Post reports that the bank will establish an AIIB currency basket with China set to push for the yuan to take a prominent role and for “special currency funds” to be established in order to issue yuan-denominated loans through the fund. Here’s more:

Yes, “for the next few years,” which really isn’t that long, especially when compared with how long the dollar has dominated the global economic order. Perhaps even more interesting — and more alarming for Washington — is that the move by China to expand the yuan’s influence via a fund that is now backed by nearly every major country on the planet save the US and Japan, comes just as petrodollar mecantilism, which has been perhaps the driving force behind dollar dominance for decades, crumbles in the face of slumping oil prices. As we’ve reported on several occasions, 2014 marked the first year in nearly two decades that oil producers' petrodollar exports (i.e. the recycling of oil proceeds into USD assets) turned negative. In other words, falling oil prices mean producing nations are now removing liquidity from the system rather than adding it, a process Goldman estimates will will sum to nearly $900 billion by 2018. The combination of these two forces could serve to cause a dramatic shakeup in a world that heretofore functioned on a unilateral system, both politically and economically. |

04-16-15 | MACRO GEO-ECONOMICS |

19 - US Reserve Currency | |||

| NOTION - Are Lending Institutions on "Lock Down"? | ||||||

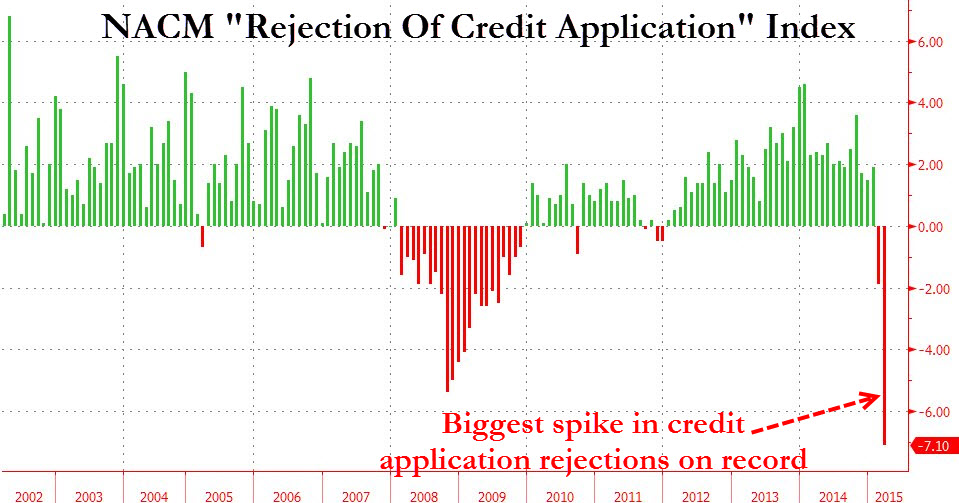

COLLAPSING CREDIT - Public & Corporations Unable to Secure More Credit "There Are Big, Big Problems" - The Shocker Crushing The Economy Revealed 04-13-15 Zero Hedge We are grateful to Alexander Giryavets at Dynamika Capital for pointing us to something which is far more troubling than even the Atlanta Fed's collapse in Q1 GDP tracking: namely the latest Credit Managers Index for the month of March which "deteriorated significantly over the last two months and current readings stand at the recessionary levels not seen since 2008." To be sure, we have previously shown the collapse in consumer debt as reported by the Fed, which as we noted, just suffered its worst month for revolving credit since December 2010 and explains "why the consumer has literally gone into hibernation - it has nothing to do with the weather, and everything to do with the unwillingness to "charge" purchases, which in turn is a clear glimpse into how the US consumer sees their financial and economic future."

It turns out it may not have been just a matter of demand: apparently something very dramatic has been happening in February and especially in March. Instead of spoiling the punchline, we will leave it to the National Association of Credit Managers to explain what happened: From the latest NACM Credit Managers Index:

You mean it wasn't the weather? "As was the case last month, the majority of the damage was seen in the service sector and this month it is going to be hard to blame it all on the weather or some other seasonal factor." Ok, good to know that we were correct in mocking all those "economisseds" who say the recent collapse in seasonally-adjusted (as in adjusted for the seasons... such as winter) data was due to the, well, winter, a winter in which 3 of 4 months were hotter than average! So what is going on? Well, nothing short of another recession it appears.

Of course, in a world in which the only economic growth comes as a result of new credit entering the economy (as opposed to Fed reserves being stuck in the S&P), the only thing that matters is how easy it is to get credit into the hands of those who need it. As it turns out it has never been more difficult to get credit. No really! According to the CMI, the Rejections of Credit Applications index just crashed the most ever, surpassing even the credit crunch at the peak of the Lehman crisis. This can be seen on the chart below. And without any new credit entering the economy, a recession is all but assured. More details on what may be the most critical and completely underreported indicator for the US economy. The report continues, with such a dire narrative that one wonders how it passed through the US Ministry of Truth's propaganda meter:

For those who enjoy tables, here it is: Just in case there was still confusion about what is truly going on when one strips away the daily "S&P500 is at all time highs" propaganda and iWatch infomercials, here is some more doom and gloom from the source:

And the stunner:

No other commentary necessary.

|

04-14-15 | US CONSUMPTION | 25 - Public Sentiment & Confidence | |||

| TO TOP | ||||||

| MACRO News Items of Importance - This Week | ||||||

GLOBAL MACRO REPORTS & ANALYSIS |

||||||

US ECONOMIC REPORTS & ANALYSIS |

||||||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | ||||||

| Market | ||||||

| TECHNICALS & MARKET |

|

|||||

| STUDIES - TIME VALUE OF MONEY - Not Just Inflation Rate but Duration | ||||||

THE MONEY ILLUSION - Selling Time Central Banks Made The Whole World “Buy Time”... There Are Signs We’re Beginning To Sell It 04-14-15 Zero Hedge By Paul Mylchreest of ADM International Selling Time Can you arbitrage time? Central banks made the whole world “buy time”. There are signs that we’re beginning to sell it Central banks artificially lengthened time horizons in financial markets and the real economy by distorting time preference. There is evidence that time horizons are now shortening, e.g. weak capital investment, flattening yield curves, dollar strength & physical gold demand. Perhaps the tsunami of global speculative capital—a result of extreme “financialism” - is getting nervous and seeking safer havens. Historically, volatility in currency markets has led to destabilising flows in speculative capital which have subsequently impacted other financial assets. One way to “sell time” is, paradoxically, buying long-term Treasuries and, therefore, “bond-like” equities, such as financially strong Consumer Staples and Utilities companies. For equities in general, we found two indicators which gave well-timed sell signals at the last two peaks in the S&P 500 in 2000 and 2007. Both of them – Treasury yield curve (7s10s) and “adjusted” MACD - are getting close to giving the first sell signals in nearly eight years. Executive Summary Can you buy and sell time? We think that you can from the perspective of time horizons. In our view, financial markets are operating on the wrong time horizon – one that is too long (thanks to central banks ZIRP/NIRP and credit creation) - although there are signs that this is beginning to change. We are in a global debt bubble and debt has a “time function” given its ability to bring forward consumption from the future into the present. Debt essentially “buys time” and the world has bought a (hell of a) lot of time. The “present” is inexorably catching up with what was the “future.” Time preference reflects the relative valuation placed on goods at an earlier date versus a later date. While current goods (including cash) should always have a higher valuation than future goods, time preference declines as an economy becomes wealthier, i.e. the proportion of income devoted to current consumption falls versus that devoted to saving/capital accumulation. Since the crisis, central banks have sought to address “under-consumption” (how many people do you know who voluntarily under-consume?) by distorting time preferences in the real economy and financial markets via zero interest rates and excessive credit creation. Negative interest rates are another step in this direction. At the heart of their policy, however, is a fundamental contradiction.

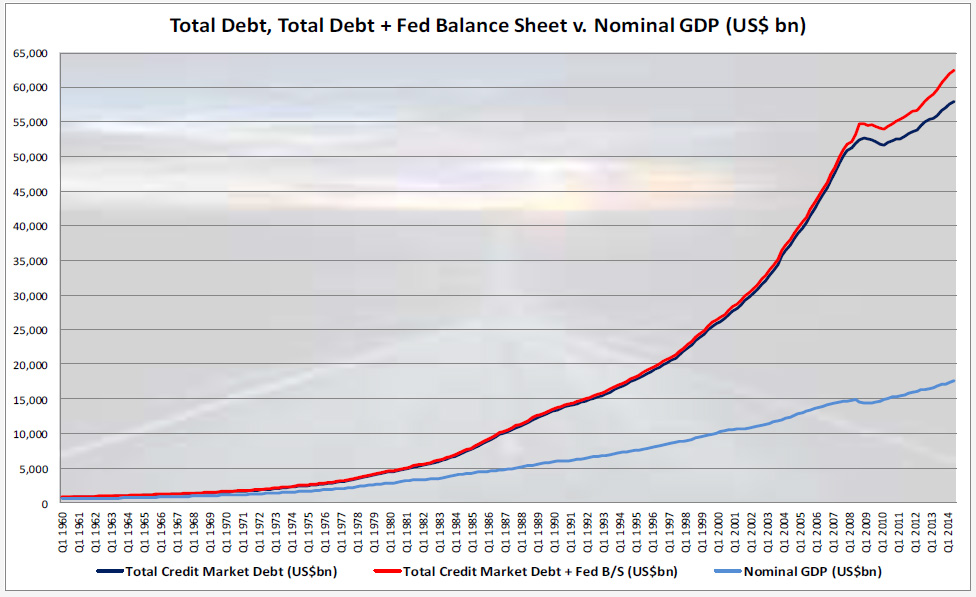

While artificially increasing time preference fundamentally weakens an economy, there is no immediate concern unless there is evidence that businesses, consumers and investors are recognising that time preference is too high and are responding accordingly. We detect signs that time horizons are shortening in both the “real” economy and financial markets. * * * Time, Debt and Central Banks We are in a global debt bubble and debt brings forward consumption into the present from a more distant point in the future – since it removes the need to save the loan value out of disposable income. Consequently, the accumulation of debt has a time function. Debt essentially “buys time”, so borrowers are literally “long” time and short the currency/credit which they must return to the lender at a later date. While lenders lend money, they are also “lending” or “selling” time to the borrowers. While it has a geared effect on economic growth, “buying” more and more time becomes problematic. As time progresses, what is “the present” begins to catch up with what was “the future.” In the US, total credit market debt outstanding is US$58.0 trillion, or $62.4 trillion if you include the Fed’s balance sheet. At 331.7% of GDP, it is significantly higher than the 275% reached at the peak of the Great Depression. What deleveraging? It’s noticeable how central bankers almost never mention that TOO MUCH DEBT is the key factor holding back growth in what is a credit-driven global economy. This is the sleight of hand to deflect guilt. In fact, their strategy has been to address the fallacy (think about it) of under-consumption by an all-out attempt to make it cheaper to borrow so that the world accumulates even more debt. And the US is only a part of the story. The total amount of debt accumulated on a global basis is approximately US$200 trillion according to a recent report from the management consulting firm, McKinsey. The world is “long” (a hell of) a lot of time. Looked at in another way, central banks have artificially lengthened time horizons in the real economy and financial markets by distorting time preference. They have created an illusion at the heart of which is a fundamental contradiction. Time preference is the relative valuation placed on goods (including money) at an earlier date versus a later date. It almost goes without saying that, in general, people would rather fulfil their desires today than tomorrow. Who wouldn’t? People value present goods more highly than future goods. This concept is obviously used in DCF calculations to value financial assets/projects, i.e. cash flows at an earlier date have a higher valuation than cash flows at a more distant date. In an economy, the way that time preference alters the balance between consumption today versus saving/investment for the future - and how debt accumulation interacts with this process – has major implications for growth. As an economy becomes wealthier, time preference declines. Time preference plays a key role in the formation of interest rates along with diminishing marginal utility (e.g. if you were on a desert island with nothing but 2 bananas, it probably makes sense to eat the other one tomorrow). Implicit in time preference is that interest rates should be positive. Borrowers have to compensate lenders for the use of cash now if they don’t want to (or can’t) save it out of disposable income. Lenders require positive interest rates to defer consumption over and above some level of precautionary cash reserve. Negative interest rates violate the normal concept of time preference, implying the premium of present goods to future goods is reversed. A person who saves SFr100 and gets SFr 99 back in a year’s time must judge that the value of SFr 99 for consumption in a year’s time is more than SFr100 now. Switzerland was the first country to see its 10-year yield slip into negative territory. More than 15% of all developed market sovereign bonds are now trading on a negative yield. Swiss yields are currently negative out to nine years, German yields out to six, Danish out to five and Swedish out to four. This strikes us as an extraordinary market signal. How could things have become so distorted and why is the consensus view so complacent? It seems that as long as stock markets are buoyant and sovereign bond yields of major nations remain very low, the majority will bask in the status quo. Many suggestions are being put forward to explain negative yields so far out on the curve.

All might be contributing, to a greater or lesser extent, but most are reflecting economic weakness and/or risk aversion on one hand and extreme policies of central banks on the other. In contrast to the Fed, BoJ, BoE and (now) the ECB, the Swiss National Bank has never bought its own sovereign bonds. Nor should we forget that there are still alternative sovereign bonds with respectable credit ratings and much higher (it’s all relative) yields, e.g. US Treasuries. Yet the yield differential has not been arbitraged away, or at least not yet. And if it was, which way would it go? What’s happening made us think about time preference and the way in which it is being distorted. An increase in time preference implies that a higher ratio of income is devoted to consumption versus saving/investment for the future. It should be obvious that this is precisely the aim of central bank policies to “correct” what they view as under-consumption. At its heart is a cynical inducement for businesses and consumers to make what are, in some cases, incorrect or risky spending decisions. Increasing consumption when savings ratios are low and debt is high suggests that central banks are trying to create the illusion that time preference is lower/falling when it’s actually higher/rising. If we look at the US, for example, while debt is at an all-time high, the savings ratio is at a very low level by historical standards. The problem becomes clear when you think more deeply about rising time preference in an economy. An increase in time preference means a corresponding reduction in saving. Saving/investment, in case we forget these days, is the basis of wealth creation, i.e. the creation and productive application of surplus. An economy with a time preference of 100% would spend all of its income on consumption and would never have any surplus for capital investment in order to increase its standard of living. Indeed, in no way is it an exaggeration to say that it was only by lowering time preference that civilisation was possible. In normal circumstances, the more that time preference is raised, the more people live a hand-tomouth (or “paycheck to paycheck”) existence. Current levels of consumption become harder to sustain, there is less confidence in the future and time horizons shorten. In this environment, capital investment, which is the basis for wealth creation, suffers. All things being equal, high time preference would normally equate with higher interest rates as borrowers compete for scarce funds and need to offer high rates to induce people into saving. Time preference tends to be higher for the very old, the very young, people living in less developed societies and for individuals and entities which are heavily indebted (which increasingly includes governments). In extreme cases, it can be associated with a rise in central planning, “big government”, the subversion of property rights and rule of law and when a system starts decaying towards socialism. Venezuela is an example of this. In such circumstances, governments “kill” productive investment, there is hoarding/shortages and capital flight emerges. What about the opposite situation? When time preference is low or declining, a smaller ratio of income is devoted to consumption versus savings and investment. This implies a comfortable level of financial “surplus”. Current levels of consumption should be sustainable and time horizons lengthen due to greater confidence in the future. Abundant savings implies lower interest rates for borrowers. Businesses and entrepreneurs react to the higher savings/confidence with new capital investment, particularly in higher orders of production which are more distant from the final consumer. This includes natural resources, like oil & gas and metals and mining, and capital goods projects. In a big picture sense, time preference tends to decline when a society experiences a broadly-based rise in wealth/capital accumulation. It is often associated with other factors such as technological progress, free-market capitalism, “small” government, the respect for property rights and the rule of law. This was Douglas French writing in “High Rises and High Time Preferences”. “The lower the time preference rate, the earlier the onset of the process of capital formation, and the faster the roundabout structure of production will be lengthened. Civilization is set in motion by individual saving, investment, and the accumulation of durable consumer goods and capital goods.” It should be clear how central banks are attempting to distort time preference and how their policies contain a fundamental contradiction in terms of time horizons and wealth creation. In essence, they are creating an illusion. While aggressively seeking to increase time preference, with all its negative implications, on the one hand, they are trying to give the impression that time preference is lower than it really is by making current levels of consumption seem more sustainable by forcing down interest rates and replacing savings with cheap credit. This artificially extends time horizons and increases confidence. But, lest we forget, a rising time preference is indicative of a weakening economy, not a strengthening one, and one which is more vulnerable than it looks. It doesn’t take a genius to realise that the end result of trying to artificially lower time preference is to exacerbate the volatility of the business cycle and financial markets. We know the result. Each bubble is bigger than the last because the recovery from the previous bubble requires even lower interest rates and more credit creation…which induces some businesses and consumers to make a new round of risky spending decisions…and eventually…investment decisions.

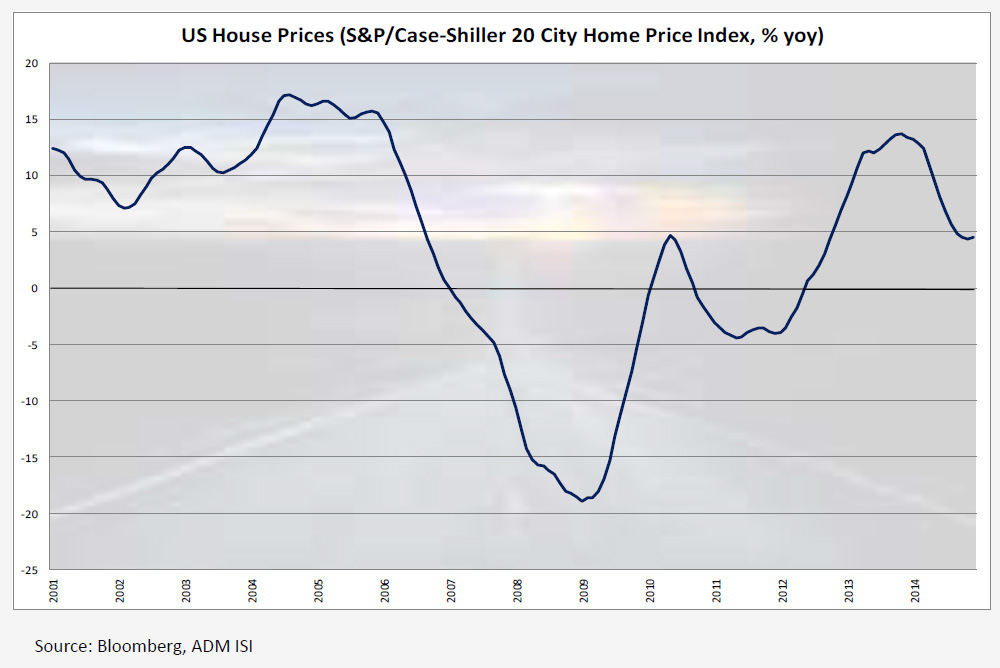

There comes a point when the illusion should start to fade. The average person will start to realise that, in spite of historically low interest rates and all around central bank largesse, their time preference is not that low. In fact, it’s been rising and increasing it further would be irresponsible. Time horizons will shorten and risk increases. The focal point of the last bubble was US house prices and associated securitised loans. House prices, which (according to Bernanke) were never supposed to fall, but were already falling more than a year and a half before Lehman collapsed. This got us thinking about what signs we should we look for to tell if the central banks’ time preference illusion is running out of road. � |

04-15-15 | STUDY "SELLING TIME" |

||||

| COMMODITY CORNER - AGRI-COMPLEX | PORTFOLIO | |||||

| SECURITY-SURVEILANCE COMPLEX | PORTFOLIO | |||||

| THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur | ||||||

| 2015 - FIDUCIARY FAILURE | 2015 | THESIS 2015 |  |

|||

| 2014 - GLOBALIZATION TRAP | 2014 |  |

||||

|

||||||

|

2013 2014 |

|

|||||

FINANCIAL REPRESSION - Negative, long-term effects of massive Money Printing American Thinker posted essay emphasizes the negative, long-term effects of massive money printing through quantitative easing (QE) & of the zero interest rate policy (ZIRP) .. it's all about the financial repression of interest rates - the thinking being that if this were not done, the pain of allowing the free markets to determine interest rates would be unbearable - "One need only imagine the bipartisan political panic were the interest paid by the U.S. federal government on its debt to double or triple, squeezing out hundreds of billions of dollars of spending on military and social programs. It is becoming ever more obvious to ever more people that sustaining these 'financial repression' policies is making economies ever more comatose; ever less dynamic. Exactly when the accumulating long-term economic damage becomes more onerous to central bankers and politicians than the short-term damage of ending QE and ZIRP can’t be known. But that inflection point will come, desired or not; willed or not. It is not avoidable." If the world’s central bankers are successful in pursuit of their short-term goals by the use of Quantitative Easing (QE) and Zero Interest Rate Policy (ZIRP) -- winning the race to the bottom in currency devaluation to the cheers of economically dogmatic, faux-literate media -- these bankers can’t then avoid being failures over the intermediate and longer terms in the race to attract productive, job creating investment. This appeared on April 10 in ZeroHedge.com:

There is no argument now that what has been and is currently missing from the global economic recovery is private market investment in the means of production -- land, building, equipment, productivity-related technology, and software. Attempts in the last 7 years by governments to tax, print, borrow, and regulate their way to prosperity are ever more clearly the reason that this private market investment has been and is being delayed, deferred and cancelled. No sane corporate manager invests long term into a currency that is being persistently undercut by official doctrines -- QE and ZIRP -- nor into an economy undermined by unpredictable waves of regulation and potentially confiscatory tax regimes. This cause and effect is now being denied only by the most dogmatic of progressive ideologues and blindest “social economists”. Despite the obvious, the central bank of every major country on the planet currently has one or both of these programs in force. The U.S. Fed has, to it credit, ended QE. It is clear, however, that ending ZIRP is going to be a difficult and painful process. And there are more than a few smart observers who think ZIRP will never voluntarily end in the U.S. -- nor in Japan, nor in Europe. Their judgment is that the pain of allowing the free markets to retake control of the level of interest rates of intermediate and long maturity bonds, called ending ‘financial repression’, will prove unbearable. One need only imagine the bipartisan political panic were the interest paid by the U.S. federal government on its debt to double or triple, squeezing out hundreds of billions of dollars of spending on military and social programs. It is becoming ever more obvious to ever more people that sustaining these 'financial repression' policies is making economies ever more comatose; ever less dynamic. Exactly when the accumulating long-term economic damage becomes more onerous to central bankers and politicians than the short-term damage of ending QE and ZIRP can’t be known. But that inflection point will come, desired or not; willed or not. It is not avoidable. Michael Booth, often posting and commenting as Cato, lectured in finance and economics at the Univ. of Texas, and worked for 20 years as an independent contractor and managerial trainer on financial topics in the technology industry. |

04-13-15 | THESIS | ||||

2011 2012 2013 2014 |

|

|||||

| THEMES - Normally a Thursday Themes Post & a Friday Flows Post | ||||||

I - POLITICAL |

||||||

| CENTRAL PLANNING - SHIFTING ECONOMIC POWER - STATISM | G | THEME | ||||

| - - CORPORATOCRACY - CRONY CAPITALSIM | THEME |  |

||||

- - CORRUPTION & MALFEASANCE - MORAL DECAY - DESPERATION, SHORTAGES. |

THEME |  |

||||

| - - SECURITY-SURVEILLANCE COMPLEX - STATISM | M | THEME | ||||

| - - CATALYSTS - FEAR (POLITICALLY) & GREED (FINANCIALLY) | G | THEME | ||||

II-ECONOMIC |

||||||

| GLOBAL RISK | ||||||

| - GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | G | THEME | ||||

| - - SOCIAL UNREST - INEQUALITY & A BROKEN SOCIAL CONTRACT | US | THEME | ||||

| - - ECHO BOOM - PERIPHERAL PROBLEM | M | THEME | ||||

| - -GLOBAL GROWTH & JOBS CRISIS | ||||||

| - - - PRODUCTIVITY PARADOX - NATURE OF WORK | THEME | MACRO w/ CHS |

||||

| - - - STANDARD OF LIVING - EMPLOYMENT CRISIS, SUB-PRIME ECONOMY | US | THEME | MACRO w/ CHS |

|||

III-FINANCIAL |

||||||

| FLOWS -FRIDAY FLOWS | MATA RISK ON-OFF |

THEME |  |

|||

| CRACKUP BOOM - ASSET BUBBLE | THEME | |||||

| SHADOW BANKING - LIQUIDITY / CREDIT ENGINE | M | THEME | ||||

| GENERAL INTEREST |

|

|||||

| STRATEGIC INVESTMENT INSIGHTS - Weekend Coverage | ||||||

|

SII | |||||

|

SII | |||||

|

SII | |||||

|

SII | |||||

| TO TOP | ||||||

Read More - OUR RESEARCH - Articles Below

Tipping Points Life Cycle - Explained

Click on image to enlarge

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

�

TO TOP

{kind=link}

{kind=link}

{kind=link}

{kind=link}