SULTANS

OF SWAP: ACT II - The Sting!

There

are 7 stages to executing a successful sting operation. Whether this is

the modus operandi behind the Sultans of Swap operating in the $605

Trillion OTC Derivatives market or just simple coincidence, I will leave

it to you shrewd reader to determine. The seven stages do however

offer us an instructive theater guide to better understand these murky

instruments called Interest Rate Swaps.

There

are 7 stages to executing a successful sting operation. Whether this is

the modus operandi behind the Sultans of Swap operating in the $605

Trillion OTC Derivatives market or just simple coincidence, I will leave

it to you shrewd reader to determine. The seven stages do however

offer us an instructive theater guide to better understand these murky

instruments called Interest Rate Swaps.

Act I can

be found at

SULTANS OF

SWAP: Smoking Guns!

In Act I of our fictional play, we

discovered the players, how our Sting had been set-up, the innovative

financing arrangements employed and the trading mechanism that allowed our

Sting to be potentially perpetrated.

There was a very interesting development however that occurred during our

play�s intermission. We had a fight break out between our DIRECTORS. Our

sleepy actors behind the stage curtains were heard arguing amongst themselves as our audience enjoyed a casual libation and pondered the

smoking guns unveiled in Act I.

What they overheard was the White House (a DIRECTOR) refusing to support

European legislative efforts to stop the apparent deviant behavior of our

sinister SPECULATORS. (See

Act I for your theater guide).

Angela

Merkel

and

Nicolas Sarkozy

emphatically demanded changes

in European Derivatives trading, and they sent Greek Prime Minister George

Papandreou to the White House as an example of a vulnerable victim (PATSY)

to plead the case. He was

quickly rebuked,

being informed that this �was a Greek problem�. The audience once again

heard Johnny Depp�s famous quip from the mob movie �Donnie Brasco�,

when Brasco was trapped in similar exposing entanglements responding �Forget

about it!�. Without US legislation, any European actions

attempted would be knowingly useless in today�s global trading markets.

The President was fully cognizant of this, especially when he authorized

the

$170B of bailouts by the US government

on AIG�s CDSs (Credit Default Swaps) which had been headquartered and

executed out of London. Who has our President possibly been listening to,

especially since he was elected on a platform of �Change� in the midst of

the financial meltdown?

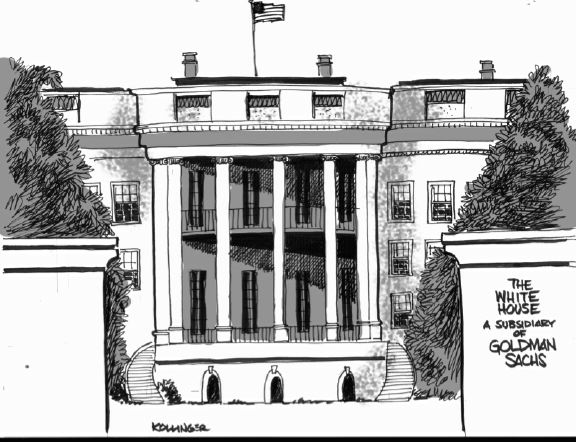

The

cartoon of the White House I saw recently on the web is an indication of a

strong growing public perception. These actions by the White House simply

reinforce this view. Sites are now

detailing

relationship grids with the White House.

I point this out not to cast dispersions on the parties

depicted

by this particular cartoonist, but rather to highlight the public outrage

that is becoming clearly prevalent.

depicted

by this particular cartoonist, but rather to highlight the public outrage

that is becoming clearly prevalent.

But this

is not the full argument between our DIRECTORS that the audience

overheard. The day after the President�s meeting, Gary Gensler the

Chairman of the CFTC (US Commodity Futures Trading Commission) and the

chief enforcement DIRECTOR in the US, spoke in an address to

Markit�s

Outlook for OTC Derivatives Markets Conference

and then again two days later at the

International Regulators to Discuss Future Industry Issues.

He

spelled out almost verbatim

that which we dear reader laid out in Act I concerning the OTC and CDS

trading. I absolutely applaud him and all the professional members within

the OTC. I strongly recommend you study carefully his remarks in full

(1)(2). Make no doubt about it appalled reader, the vast majority of

practicing professionals want this mess cleaned up. There appears to be a powerful element that has the ear of the Legislative Branch of the

US government. Without stringent legislation, the enforcement agencies are

toothless tigers. This is a remake of the play starring former CFTC

Commissioner Brooksley Born in her well documented efforts by

PBS

Frontline�s �The Waring�

which would have potentially avoided the whole 2008 financial crisis (3).

The Washington �Blame Game" cannot be placed at the feet of the CFTC,

though I am sure the commissioner will be another �Fall Guy� in future

years when the Sting has occurred and a successful Getaway has taken

place. Our 7 steps to a successful Sting mandate a �Fall Guy� which allows

for the deflection during the masked getaway. Commissioner Gensler

obviously does not knowingly want to be cast as yet another PATSY in our

instructional theater.

ACT II � THE STING

The

second act is the heist itself. With rare exception, the heist will be

successful, though some number of unexpected events will occur.

6- THE SHUT-OUT

The

whispering has now ended on stage and only the PATSIES remain. They stand

nervously clutching their newly minted Swap contracts.

This is

the stage where the PATSY is trapped by something unexpected. An

original assumption has changed. A key parameter was found critically

flawed. What was commonly accepted as a �truism� or 'given' is no longer

true or predictable.

Our

chart above shows that the financial crisis began with Sub-Prime Consumer lending

and eventually took down most of the US mortgage lending industry. It then rolled on to engulf Fannie Mae /

Freddie Mac / AIG and almost ended Investment Banking as we have

known it in America. What may be misunderstood is how the obligations were

all rolled upward. What was consumer debt suddenly became corporate debt

(i.e. Fannie Mae) which then became sovereign debt (i.e. Fannie

Mae / AIG). This is not by coincidence. The 'assumption' of the

obligations and the securing of the �Guarantee� of debt are part of what

we might label as Regulatory Arbitrage.

Our

chart above shows that the financial crisis began with Sub-Prime Consumer lending

and eventually took down most of the US mortgage lending industry. It then rolled on to engulf Fannie Mae /

Freddie Mac / AIG and almost ended Investment Banking as we have

known it in America. What may be misunderstood is how the obligations were

all rolled upward. What was consumer debt suddenly became corporate debt

(i.e. Fannie Mae) which then became sovereign debt (i.e. Fannie

Mae / AIG). This is not by coincidence. The 'assumption' of the

obligations and the securing of the �Guarantee� of debt are part of what

we might label as Regulatory Arbitrage.

Regulatory

Arbitrage strategies were never clearer than during the following periods

when the US Government was forced:

1- To Lend or Guarantee GM and Chrysler

debt, as stock prices were crushed along with their bond prices and CDS

activity shot up. Don�t forget GMAC in these commitments.

2- To pay AIG obligations of

$182.3B

based on contracts that were heresy. The US government felt it had no

choice but to immediately pass legislation to spend $700 Trillion for

TARP (Troubled Asset Relief Program) to bailout

insolvent banks who declared record profits less than 9 months later.

3- To

suddenly accept the obligations of Fannie Mae and Freddie Mac into

Conservatorship. This was after years of the US

government denying it had implicit responsibility for the debt and

obligations of these agencies. This public charade came crashing down in

September 2008.

It is a

chess game between a keen eyed chess champion executing a carefully

choreographed strategy with each move versus a hallucinating crack cocaine

addict.

Strategy

is something that happens to you when you are looking the other way!

Anonymous

CEO during a bankruptcy proceeding

Let�s take

a second and �peel the onion� on just one of many examples, using the

Fannie Mae and Freddie Mac example above as an illustration.

On

Christmas Eve 2009 the Obama administration quietly slipped out an

announcement entitled �Treasury

Issues Update of Support For Housing Programs�.(4)

The Sub-Titles are labeled �Program Wind Downs� and �Amendments to Terms

of Preferred Stock Purchase Agreements�. A person would have to have

nearly no life to start crawling through such a document with these

headings instead of slipping away to do some last minute family shopping.

But there buried near the end of the fourth paragraph, you read: �Treasury

is now amending the PSPAs to allow the cap on Treasury's funding

commitment under these agreements to increase as necessary to

accommodate any cumulative reduction in net worth over the next

three years�.

(bold mine) Also at the end of the next paragraph, you find:

"The amendments to these

agreements announced today should leave no uncertainty about the

Treasury's commitment to support these firms as they continue to play a

vital role in the housing market during this current crisis.�.

Immediately the Washington Post who pays people to work these holidays ran this story

on Christmas Day:

�U.S.

promises unlimited financial assistance to Fannie Mae, Freddie Mac�.

I am sure this pulled everyone away from the Christmas family meal to

read. Bloomberg also hastily ran the story on Christmas Day: �U.S.

Treasury Ends Cap on Fannie, Freddie Lifeline for 3 Years�

which many who have Bloomberg screens in their home office would have

been riveted to. By Monday the coverage was way down the reading list below

breaking news and the stale yesterday's news. I thought Representative

Scott Garrett (R-N.J.), a member of the House Financial Services

subcommittee that oversees Fannie Mae and Freddie Mac, said it well in the

Washington Post on Christmas Day:

"The Obama administration's decision to write a blank check with taxpayer

dollars for the continued bailout of Fannie Mae and Freddie Mac is

appalling. Not only is this a continued bailout of failed entities that

need to be privatized to protect the taxpayer, the timing of the

announcement is clearly designed to try and sneak the bailout by the

taxpayers."

Representative Scott Garrett (R-N.J.)

U.S.

promises unlimited financial assistance to Fannie Mae, Freddie Mac

Washington

Post

This is

used simply as an instructive example of how things work when people are

feeding at the public trough and how Sovereign Guarantees are secured

within the Holy Grail of Lending. What we learned from the housing bubble

is when accountability was removed; deviant behavior was prone to occur.

When the banks stopped holding the mortgages on houses they initially lent

money to, their motivations changed. In this example, the ultimate

accountability rested with the taxpayer who is almost completely unaware.

The taxpayers� elected representatives are not representing. They are

absent or �handcuffed�. I have heard endless politicians like

Representative Scott Garrett express their frustrations. Michael Moore�s

alarming new movie: �Capitalism:

A Love Story�

is worth reviewing simply to listen to our elected officials using phrase

like �Coup d��tat�.

We have

never witnessed more debt so successfully shifted up the Debt Risk Ladder

to Sovereign debt in the history of the MANKIND.

There is

an old saying:

OLD

SAYING:

�When you

owe the bank

$100,000

and can�t pay you have a problem.

When you owe the bank 100M

($100,000,000)

and can�t pay the bank has a problem�.

TODAY�S

VERSION:

When the

banks owe 100B

($100,000,000,000)

and can�t pay the banks have a problem.

When the banks owe 1T

($1,000,000,000,000)

and can�t pay, MANKIND has a problem�.

To say

governments are being trapped is rather an understatement. Ask the furious

electorate what they think. In the US many border on rebellion with �tea

parties�, while the lunatic fringe crashed a plane into a government

building and another shot military personnel at the pentagon. This is new

behavior not seen in the US. The rage was palpable for those that

witnessed firsthand the election of Scott Brown in Massachusetts. Ask the

rioters in the streets of Greece. It is obvious to all but our DIRECTORS

� still in near oblivion to how they are being played like a violin. The

public has the street smarts to spot a sting, even when those in power

claim to not see it - like former Fed Chairman Alan Greenspan not seeing

the US housing bubble. This may all seem like political hyperbole

from yours truly, but it is important to

the success of �The Getaway�, as you will see later in Act III

The vice is squeezing to set up the actual STING.

7- THE

STING

Events

have changed and our PATSIES found that what was a good idea doesn�t appear to

be such a good idea any longer. They begin reading the small print in

their Swap contract to see how they might alter their commitments (see

Sultans of Swap: Fearing the Gearing!).

What we

have witnessed since 2002 is a race by consumer borrowers to capture what

they perceived to be low rates and by consumer lenders (i.e. pensioners on

fixed income) to chase yield. Like addicts needing a fix they both wanted

it now � immediately. In the case of professional borrowers and lenders,

jobs, careers and advancement were on the line. Success was felt to be

determined by getting another 15 points or possibly 100 basis points. All

were clearly short term preoccupations. They were looking the other way!

We

have see states and municipalities locking themselves into contracts

unwittingly for 30 years versus 10 years, as pointed out the New York Times

(5). They locked themselves into balloon payments that they cannot

possibly ever pay as we witnessed with Kitlos PLC and the Greek government

debt. Debt will be financed in the future with higher principle

amounts (see the growing list at

SULTANS). In a moment we will discuss the

interest rates these rollovers may potentially command.

We

have see states and municipalities locking themselves into contracts

unwittingly for 30 years versus 10 years, as pointed out the New York Times

(5). They locked themselves into balloon payments that they cannot

possibly ever pay as we witnessed with Kitlos PLC and the Greek government

debt. Debt will be financed in the future with higher principle

amounts (see the growing list at

SULTANS). In a moment we will discuss the

interest rates these rollovers may potentially command.

How for

example will the US ever realistically pay for its $62 Trillion in

unfunded liabilities associated with Medicare / Medicaid and Social

Security? (Niall Ferguson estimates it to be $104T (6)). Add to this

another $20T in fiscal spending imbalances by the end of the decade. Since

we don�t have a clue, is it too hard to imagine that those who eventually

will be orchestrating the lending just might?

Unknowable

you say? That may not be. The BANKSTERS seem to know something, if you study the

chart to the right. What they know might be

debatable. What is not debatable, is that they know something is coming!

�The number of companies globally that were rated B- or lower rose to 523,

or 9.3 percent of the total, at the end of last year as speculative-grade

issuers were downgraded, Standard & Poor�s analysts led by

Diane Vazza

said in a March 5 report. That compares with 8.4 percent in 2008 and 5.8

percent in 2007, S&P said.� (8)

�In December, 260 companies had defaulted year-to-date, the

highest count since its series began in 1981. The trailing 12-month

speculative default rate has continued to climb since the crisis though

S&P has lowered its default rate forecast for 2010, because of the

improvement in capital markets. But the more positive default rate

expectation is being driven by increased forbearance by lenders in a

monetary environment propped up by policy-induced liquidity. The S&P

analysts said in a report: �Without a revival in top-line earnings and

growth, many surviving leveraged issuers originated during 2003-2007 could

face renewed default risk unless they significantly reduce their debt

burdens�. (9)

�At the annual conference for the Loan Syndications and Trading

Association, investors and observers said the market�s focus should be

farther into the future. �2011 will be the exciting year,� said James

Ferguson, chief investment officer at Octagon. Problems could arise again

because much of the debt raised to finance the buy-out boom a few years

ago will begin to mature from 2011. The demand that helped to fuel that

boom, mainly from structured vehicles called collateralized loan

obligations (CLOs), has fallen. The financial market also will not have

the support of government stimulus, which will be winding down by then.

Roughly $1,000bn of leveraged loans and bonds are coming due over the next

five years, according to Michael Zupon of Sound Harbor Partners, while

$500bn of CLOs are coming to the end of their investment periods. New

issuance of CLOs has dried up in the downturn. �It sets the stage for what

could be a dramatic period in 2012, 2013 and 2014,� said Mr Zupon. �If it

comes at the same time as an economic downturn, it could create a pretty

serious situation.� (10)

�Edward Altman, the Max L Heine professor of finance at the Stern School

of Business at New York University, said that the surge in so-called

distressed exchanges over the last two years also could add another layer

of defaults. Companies ranging from casino operator Harrah�s to commercial

lender CIT, have tried, both successfully and not, to convince investors

to exchange existing debt for other securities or cash to avoid

bankruptcy. Such exchanges, which usually only happen a few times a year,

exploded to 14 in 2008 and 39 this year. �Fifty per cent of all distressed

exchanges wind up in bankruptcy one to three years after,� Mr. Altman said.

�Of the 2009 crop of distressed exchanges, half will go bankruptcy in 2011,

2012 and 2013.� Mr. Altman, a noted default forecaster, also warned that

optimistic 2010 default forecasts were vulnerable to a downturn in the

economy. (10)

The growth

area in Investment banking is presently bankruptcy, restructuring and

workouts as they gear up for the eventuality. Massive defaults are coming

and everyone knows it except the PATSIES, DIRECTORS and unfortunately the

taxpayer. (see

SULTANS OF SWAP: Fearing the Gearing!)

Ratings will continue to be downgraded which will drive up borrowing

costs and possibly more importantly will drive collateral calls associated

with Interest Rate Swaps.

We mentioned previously that a key part of a sting is that the assumptions

upon which decisions were taken change. We pointed out in �SULTANS

OF SWAP: Smoking Guns!�

that

�the five largest U.S. derivatives dealers,

including

JPMorgan Chase & Co.,

Goldman Sachs Group Inc. and

Bank of America Corp., were on pace through the third quarter to record as much as

$35 billion in revenue last year from trading unregulated derivatives

contracts, according to company reports collected by the Federal Reserve

and people familiar with banks� income sources.� (11)

But it gets worse. In a March 15th, 2010 Business Week

article entitled:

Goldman Sachs Demands Derivatives Collateral It Won�t Dish Out

the �vig�of $35B pales in comparison to �demanding unequal arrangements

with hedge-fund firms, forcing them to post more cash collateral to offset

risks on trades while putting up less on their own wagers. At the end of

December this imbalance furnished Goldman Sachs with $110 billion,

according to a filing. That�s money it can reinvest in higher-yielding

assets. �If you�re seen as a major player and you have a product that

people can�t get elsewhere, you have the negotiating power,� said Richard

Lindsey, a former director of market regulation at the U.S. Securities and

Exchange Commission who ran the prime brokerage unit at Bear Stearns Cos.

from 1999 to 2006. �Goldman and a handful of other banks are the places

where people can get over-the-counter products today.�(12) It isn�t just

new deals, it includes deals that not only corporate but more and more

sovereign PATSIES must restructure.

�Over the last three years the BANKSTERS are extracting ever larger

amounts from the $605 Trillion over-the-counter derivatives market

according to filings with the SEC and reported by Business Week &

Bloomberg. The firm led by Chief Executive Officer Lloyd C. Blankfein

collected cash collateral that represented 57 percent of outstanding

over-the-counter derivatives assets as of December 2009, while it posted

just 16 percent on liabilities, the firm said in a filing this month. That

gap has widened from rates of 45 percent versus 18 percent in 2008 and 32

percent versus 19 percent in 2007, company filings show.

�That�s classic

collateral arbitrage,� said Brad Hintz, an analyst at Sanford C. Bernstein

& Co. in New York who previously worked as treasurer at Morgan Stanley and

chief financial officer at Lehman Brothers Holdings Inc. �You always want

to enter into something where you�re getting more collateral in than what

you�re putting out.�� (12)

THE

COLLATERAL SQUEEZE

|

|

2007 |

2008 |

2009 |

|

GOLDMAN SACHS |

|

|

|

|

COLLECTS |

32% |

45% |

57% |

|

POSTS |

19% |

18% |

16% |

|

NET |

13% |

27% |

41% |

|

|

|

|

110B |

|

|

|

|

|

|

JP MORGAN |

|

|

|

|

COLLECTS |

47% |

47% |

57% |

|

POSTS |

26% |

37% |

45% |

|

NET |

21% |

37% |

45% |

|

|

|

|

37B |

SOURCE:

03-15-10

Goldman Sachs Demands Derivatives Collateral It Won�t Dish

Out Business Week / Bloomberg

�Banks have an advantage in dealing with asset managers because they can

require collateral when initiating a trade, sometimes amounting to as much

as 20 percent of the notional value, said Craig Stein, a partner at law

firm Schulte Roth & Zabel LLP in New York who represents hedge-fund

clients.� (12)

"We

will make them an offer they can't refuse!"

Marlon

Brando on consummating a financial deal in the "Godfather'

All MBA students have studied decision trees and probability paths. Our

PRODUCERS and BANKSTERS with little doubt have the finest army of young

MBA and PhD�s (Quants) graduates in the world working for them. Smart

strategists know that one of the secrets to successful strategy

optimization is in understanding the probability chains. The primary

probability

chain presently suggests an unfolding sequence that will start with Credit

Rating downgrades. This pattern as I mentioned above is now underway but

still is not as visible as it soon will be.

probability

chain presently suggests an unfolding sequence that will start with Credit

Rating downgrades. This pattern as I mentioned above is now underway but

still is not as visible as it soon will be.

Interest

Rates

will soon

begin to rise

for many. A global shortage of savings to fund what is simply monumental

levels of debt can lead to no other result. The question is only when?

Smart money doesn�t let the daily noise distract them, which pre-occupies

the amateurs.

The next shoe will be collateral calls. In the financial crisis we had

margin calls on falling equity prices. This time the

probabilities suggest it will be Collateral Calls

because of lowered ratings and increased risk metrics. We outlined this

inherent trigger with Interest Rate Swaps in

Sultans of

Swap � Explaining $605 Trillion in Derivatives

and

Sultans of

Swap: Fearing the Gearing!

The Business Week / Bloomberg article 3/15/10: �Goldman

Sachs Demands Derivatives Collateral It Won�t Dish Out�

gives a clear sense of activity presently going on in this

area.

The most probable outcome by 2012 will be an extremely serious problem

within the global 'fiat' currency markets. It will be centered on 'fiat'

currencies because they are not anchored or based on any specific

standards such as a gold standard. Presently the vast number of currencies

is �fiat�. They are based on 'confidence'. Confidence today is

becoming a commodity in short supply.

Fiat currencies are also open to debasement. Competitive devaluations and

beggar-thy-neighbor policies are highly likely as trade is fiercely

fought over in

PIMCO�s �New Normal�

. The world�s largest Bond Fund has some fairly clear views on this and

you would suspect is acting accordingly � now.

What

will this mean to those with a strategy, who have set-up the pins and have

been patient? It means initially (as we are seeing now) huge OTC Spreads

by panicky PATSIES forced to get out or renegotiate contracts. It will

soon mean years of built-in balloon payments come due just as

interest rates are rising and the PATSIES have even lower credit ratings than

they had when they assumed the underlying contracts.

What

will this mean to those with a strategy, who have set-up the pins and have

been patient? It means initially (as we are seeing now) huge OTC Spreads

by panicky PATSIES forced to get out or renegotiate contracts. It will

soon mean years of built-in balloon payments come due just as

interest rates are rising and the PATSIES have even lower credit ratings than

they had when they assumed the underlying contracts.

The real crunch potentially comes when interest rates are rising but

inflation is falling, as we have heightened concerns with a deflationary

depression. However, we don�t need this to occur to have low inflation

rates. This will potentially crush our debt junkies in their jaws.

Only a minor move could leave PRODUCERS and BANKSTERS

with a �take� of dramatic proportions as illustrated to the right.

The never ending argument of whether we are going to see Inflation or

Deflation never ceases to amaze me. No one ever asks the question, when?

This is important because the element of time allows for the possibility

of both. A probability path could entail a brief period of stagflation

with slow growth and increasing rates; then as the government continues to

print more money, velocity of money finally kicks in and we have a near

�Minsky Melt-up�. This short lived period of Inflation just as quickly

ends in a currency crisis and subsequent global deflation.

This

probability path produces profits on a $605T derivatives market

that would restructure the global balances of economic and financial

power.

All the

models of the probability paths lead to profits of varying degrees for

key members of the Sultans of Swap. Unlike the PATSIES or taxpayers, the

SULTANS HAVE A STRATEGY. The probability paths suggest an ugly future for

the PATSIES and those that either work for them or are the taxpayers,

responsible for the commitments our elected officials have guaranteed. It

is hard to win against someone who has a strategy and you are unaware of

the game, the rules, the goals and even worse, don�t even know a game is being

played.

The above is not how the process will likely unfold. That is precisely why

you have a strategy � to know what to alter to meet your goals. You need

to be organized to do this. If there is one thing the Sultans have

demonstrated in developing a $605 Trillion derivatives market as fast as

they have, it is that they are organized.

INTERMISSION

We will return shortly with Act III

Sign Up for the next release in the Sultans of Swap

series:

Sultans

ACT III � THE GET AWAY

The

third act is the unraveling of the plot. The characters involved in the

heist will be turned against one another or one of the characters will

have made arrangements with some outside party, who will interfere.

Normally, most of or all the characters involved in the heist will end

up dead, captured by the law, or without any of the loot; however, it is

becoming increasingly common for the conspirators to be successful,

particularly if the target is portrayed as being of low moral standing,

such as

casinos,

corrupt

organisations or individuals, or fellow criminals.

SOURCES

(1) 03-09-10

Keynote Address of Chairman Gary Gensler, OTC Derivatives Reform,,

Markit�s Outlook for OTC Derivatives Markets Conference

(2) 03-11-10

Remarks of Chairman Gary Gensler, OTC Derivatives Reform

, FIA's Annual International Futures Industry Conference

(3)

�The Warning� PBS FRONTLINE - Video

(4) 12-24-09

TREASURY ISSUES UPDATE ON STATUS OF SUPPORT FOR HOUSING

PROGRAMS

(5) 03-05-10

The Swaps that Swallowed Your Town

the New York Times

(6) 12-14-09

An Empire at Risk

Newsweek Magazine

(7)

CSPAN

- Rep Paul Kanjorski Reviews the Bailout Situation

(8) 03-05-10

Nearly 10% Of Global

Corporate Issuers Were Rated 'B-' Or Lower At The End Of 2009

Standard & Poors

(9) 12-22-09

S&P�s �weakest links� list

falls sharply Financial Times

(10) 10-29-09

Warning on 2011 corporate

default risk Financial Times

(11) 03-01-10

Frank, Peterson Vow to Eliminate Provision Keeping Swaps

Opaque

Bloomberg

(12) 03-15-10

Goldman Sachs Demands

Derivatives Collateral It Won�t Dish Out Business Week

/ Bloomberg

FREE

Additional Research Reports at Web Site:

Tipping Points

Gordon T Long

Tipping

Points

Mr. Long

is a former senior group executive with IBM & Motorola, a principle in a

high tech public start-up and founder of a private venture capital fund.

He is presently involved in private equity placements internationally

along with proprietary trading involving the development & application of

Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment

advice. His comments are an expression of opinion only and should not be

construed in any manner whatsoever as recommendations to buy or sell a

stock, option, future, bond, commodity or any other financial instrument

at any time. While he believes his statements to be true, they always

depend on the reliability of his own credible sources. Of course, he

recommends that you consult with a qualified investment advisor, one

licensed by appropriate regulatory agencies in your legal jurisdiction,

before making any investment decisions, and barring that, we encourage you

confirm the facts on your own before making important investment

commitments.

� Copyright 2010 Gordon T Long. The information herein was obtained from

sources which Mr. Long believes reliable, but he does not guarantee its

accuracy. None of the information, advertisements, website links, or any

opinions expressed constitutes a solicitation of the purchase or sale of

any securities or commodities. Please note that Mr. Long may already have

invested or may from time to time invest in securities that are

recommended or otherwise covered on this website. Mr. Long does not intend

to disclose the extent of any current holdings or future transactions with

respect to any particular security. You should consider this possibility

before investing in any security based upon statements and information

contained in any report, post, comment or recommendation you receive from

him.