The

news rocked the global gold market when an almost obscure line item in the

back of a 216 page document released by an equally obscure organization

was recently unearthed. Thrust into the unwanted glare of the spotlight,

the little publicized Bank of International Settlements (BIS) is

discovered to have accepted 349 metric tons of gold in a $14B swap. Why?

With whom? For what duration? How long has this been going on? This raises

many questions and as usual with all $617T of murky unregulated swaps, we

are given zero answers. It is none of our business!

The

news rocked the global gold market when an almost obscure line item in the

back of a 216 page document released by an equally obscure organization

was recently unearthed. Thrust into the unwanted glare of the spotlight,

the little publicized Bank of International Settlements (BIS) is

discovered to have accepted 349 metric tons of gold in a $14B swap. Why?

With whom? For what duration? How long has this been going on? This raises

many questions and as usual with all $617T of murky unregulated swaps, we

are given zero answers. It is none of our business!

Considering the US

taxpayer is bearing the burden of $13T in lending, spending and guarantees

for the financial crisis, and an additional $600B of swaps from the US

Federal Reserve to stem the European Sovereign Debt crisis, some feel that

more transparency is merited. It is particularly disconcerting, since the

crisis was a direct result of unsound banking practices and possibly even

felonious behavior. The arrogance and lack of public accountability of the

entire banking industry blatantly demonstrates why gold manipulation,

which came to the fore in recent CFTC hearings, has been able to operate

so effectively for so long. It operates above the law or more specifically

above sovereign law in the un-policed off-shore, off-balance sheet zone of

international waters.

Since President Richard

Nixon took the US off the Gold standard in 1971, transparency regarding

anything to do with gold sales, leasing, storage or swaps is as tightly

guarded by governments as the unaudited gold holdings of Fort Knox. Before

we delve into answering what this swap may be all about and what it

possibly means to gold investors, we need to start with the most obvious

question and one that few seem to ask. Who is this Bank of International

Settlements and who controls it?

BANK

OF INTERNATIONAL SETTLEMENTS (BIS)

The history of the BIS

reads with all the intrigue of a

spy novel

and comes with a

very checkered past. According to the BIS

web site, as a privately held bank, it decided in recent years to become

wholly owned and controlled by the Central Banks of the world - a highly

unusual decision for a private enterprise. Lengthy court cases in Le Hague

were involved by private members who objected. Something like this is

usually called a buy out or takeover, but there are no public records of

any of the central banks making such an acquisition - an extremely strange

set of events with little media coverage.

The history of the BIS

reads with all the intrigue of a

spy novel

and comes with a

very checkered past. According to the BIS

web site, as a privately held bank, it decided in recent years to become

wholly owned and controlled by the Central Banks of the world - a highly

unusual decision for a private enterprise. Lengthy court cases in Le Hague

were involved by private members who objected. Something like this is

usually called a buy out or takeover, but there are no public records of

any of the central banks making such an acquisition - an extremely strange

set of events with little media coverage.

I am sure it can all be

explained very logically until we get to the size of the balance sheet. We

are talking close to a half trillion dollar balance sheet, or more

specifically 259 billion SDR�s, which is approximately $400B. Where did

the capital or deposits come from? The BIS goes out of its way to

specifically assert it only accepts deposits from member central banks,

though it does also state confusingly in the financial notes that there

are deposits from previous financial statements from recognized

international banks. Therefore, are we to conclude that the US Federal

Reserve has huge deposits at the BIS? Though I couldn�t find the assets on

the Fed�s balance sheet, I�m sure they are there in the small print or on

the New York Feds balance sheet somewhere. It would be a legal

requirement. It is a forensic accounting nightmare to find these items

based on public documents of the various private organizations. Apparently

it is just none of our business. For such a major element of the world�s

operating financial structure to have such poor visibility, it seems

preposterous until you actually do the research. It should be laid out so

a freshman Economics class could easily follow the ownership acquisition

and money flows. It isn�t and it appears to this researcher that it is

intentionally opaque.

Since the BIS goes out

of its way to ensure readers in its annual financial report that no

private funds are accepted, maybe all we really need to know is what the

BIS officially tells us. The BIS is owned and controlled by their member

Central Banks. Therefore if the BIS was to do a gold swap of the magnitude

of 349 metric tonnes, then board member Ben Bernanke would have known of

it in advance and approved it. He would know exactly who the transaction

was with and why. If he didn�t then he is legally negligent in his

fiduciary responsibility as a

BIS board

member, because of

the size of the transaction and its material effect. Other board members

include: Mervyn King, Governor of the Bank of England, Jean-Claude Trichet,

President of the European Central Bank, Axel Weber, President of the

Deutsche Bundesbank and William C Dudley, President of the Federal Reserve

Bank of New York. You can�t have it both ways.

Though we can suspect

many things, there is no other conclusion we can reach than the swap is

part of an agreed upon plan or concurrence between these board members. So

what is the possible understanding or plan?

WHO GAVE UP THE GOLD?

There are not a lot of

institutions who possess 349 metric tonnes of gold. So who needs $14B

worth of cash and has this amount of gold? That shouldn�t be too hard to

find.

Sovereign governments

have historically created their wealth by invading other countries to

pillage their treasuries which held gold, silver and the crown jewels. The

winning and seizure of more land allowed the sovereign to give it to the

nobles who used it to tax and tithe the feudal tenets. Recurring wealth

flowed upward to the sovereign treasury.

Considering today�s EU

membership, where sovereign countries can no longer print their own

currency (the politicians first weapon of choice), there are three

channels (other than the very politically unpopular increase in taxes and

fees) open in modern times to raising money for the treasury:

1-

The public sale of debt

offerings instruments such as Bills, Notes and Bonds

2-

The more recent and

stealthy approach of selling assets, including revenue streams from such

things as taxes, fees, licensing etc.. These are sold into the

securitization market through complex derivative structures such as

Interest Rate and Currency Swaps contracts. This approach, as

recently discovered, has been rampant throughout Europe

even prior to the creation of the EU.

3-

When you exhaust all of

the above, you then sell the family jewels � the sovereign treasury of

gold holdings.

The BIS was very quick

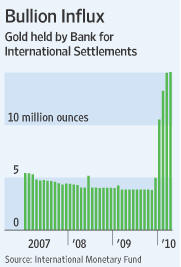

to respond to public speculation about the massive gold swap when they

immediately clarified that the gold swap was with a commercial bank. Since by

its own statements, as I mentioned above, it doesn�t accept deposits from

non member banks, this seems confusing on the surface. Does it or doesn�t

it accept private deposits? It would be respectful to assume that the BIS

is telling the truth and that they did in fact conduct the transaction

with a private bank who was transacting the swap on behalf of a central

bank or sovereign treasury. This would sort of make everything work. For

the BIS to be telling the truth in all their statements, the transaction

must be with a member central bank with the involvement of an intermediary

commercial bank. But something still isn�t right here.

When you work through

the details you quickly arrive at an astounding coincidence. Portugal

shows it has 348 tonnes of sovereign gold. The swap was for 346. Portugal

is a member bank, though does not sit on the Board, but attends the

General Meeting as an observer only. Portugal, as a member of the PIIGS,

only days after the unearthing of the swap, was again downgraded by

Moody�s, thereby making its lending costs even higher than the already

elevated levels being demanded by the financial markets. There is a very

strong possibility that the swap is with Portugal. Though who the swap is

with is important to those trading debt and credit derivatives it isn�t

quite as important to those interested in the gold market.

Ben Davies the CEO of

Hinde Capital in London and a player in the gold market

suspects

(12:40) we may have a modified form of swap emerging. There is the

possibility that the commercial bank is in fact a major gold bullion bank.

Some of the bullion banks have major short positions on gold that far

outstrip the annual physical production of gold. The disconnect between

physical and paper gold along with rising gold prices is likely causing

serious strains on their balance sheet. As Davies

points out

the gold may be transacted from a central bank to the BIS through a

bullion bank while the gold physically remains with the originating

central bank; is classified as �unallocated� at the BIS but in fact remains on

the books of the bullion bank. It effectively is double accounted for. The

increase in gold would allow gold prices to be pushed lower, which in fact

is what has been happening. A careful reading of the BIS financial

statements shows more clearly the accounting for such a transaction.

The March 31 2010

Financial Statement of the BIS shows 43.0B SDR�s of gold or 16.6% of

total assets. According to note #4 to the BIS Financial Statements: �

Included in �Gold bars held at central banks� is SDR 8,160.1 million (346

tonnes) (2009: nil) of gold, which the Bank held in connection with gold

swap operations, under which the Bank exchanges currencies for physical

gold. The Bank has an obligation to return the gold at the end of the

contract.� It is very important to appreciate this note is pertaining

specifically to BIS �assets� which in the case of banks are what the

reader would consider �loans�. Under Financial Policy notes #5 to the

Financial Statement the BIS is clear that under banking portfolios �all

gold financial assets in these portfolios are designated as loans and

receivables�. Separately, but very interestingly the BIS additionally

states � the remainder of the Banks equity is held in gold. The Bank�s own

gold holdings are designated as available for sale�.

There can be little doubt that the Gold Swap is with a central bank where

the physical gold remains. The transaction is considered a deposit at the

BIS (liability) but has been lent to a commercial bank (likely a bullion

bank) as a loan (asset). The question is only why a bullion bank needs to

borrow this quantity of gold, remembering it never gets the physical gold

because it remains at the originating central bank. The reader is

encouraged to read the

Financial Policy notes #4,5, 6, 13, 14, 15,

16, 17 and 19 within the BIS Financial Statement for a clearer

understanding along with Notes to the Financial Statements #4 and #11.

The BIS is known as the central bank to the central bankers.

The BIS may

equally be referred to as the Central Gold Bullion Bank to the Gold

Bullion Banks.

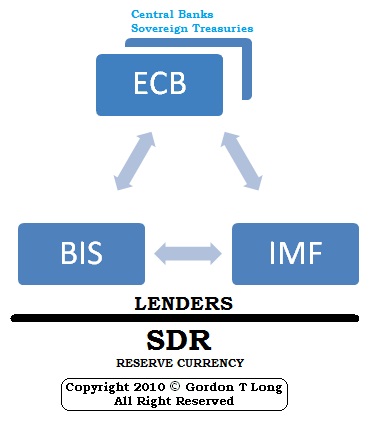

SPECIAL DRAWING RIGHT (SDR)

If problems get worse

for Portugal, as possibly the global economic climate worsens, then the

gold may never legally belong to Portugal. The contracted swap terms at some

point may simply reclassify it a net zero sale, if Portugal fails to

return the cash portion of the swap. The BIS would have 346 tonnes of gold

and Portugal the $14B of Euros it has long since spent to solve a 2010

problem. By then Portugal likely would need even more loans in whatever

currency would replace a crumpling or possibly extinct Euro.

Up until 2004 the BIS

denominated its financial statements in Gold Francs. It now has made a

major shift to denominating itself into Special Drawing Rights (SDRs). The

calculation is exactly the same as used for the IMF. The SDR is operating

as a defacto currency.

It takes a little

arithmetic (which is not done in the financial statements) to be able to

get values in any currency that can give the reader a perspective of the

scope of the activities at the BIS. The SDR reporting obscures the BIS�s

significant size and scope.

FUNDING

For those who followed

the European Sovereign Debt Crisis and the negotiations with Greece, you

know that the IMF was an unwelcomed intruder into EU financial affairs.

Greece on more than one occasion held the IMF as a negotiating ploy and as

a funding alternative to the EU�s procrastination and lack of

decisiveness.

The IMF�s willingness to

interfere created a lot of bad feelings within the EMU and Germany

specifically. As Ambrose Evans-Prichard

reported:

�The ECB is barely on speaking terms with the IMF � the "Inflation

Maximizing Fund" as it was dubbed in a Bundesbank memo - -

The IMF has not caught up to the reality in Europe said ECB �ber-hawk

J�rgen Stark on July 9th� The final EU bailout in fact heavily

involved the IMF participation. The very busy IMF is the dominant crisis

lender of last resort throughout all Central & Eastern European current

financial problems.

What we are seeing is

the emergence of another funding structure based on the SDR - SDR�s that

have a degree of gold backing. The BIS now has a total of 12.4% of its

deposits (32B SDR) in the form gold deposits. Note #11 to the BIS

financial statements states: �Gold deposits placed with the Bank originate

entirely from Central Banks. They are all designated as financial

liabilities measured as amortized cost�.

What we are seeing is

the emergence of another funding structure based on the SDR - SDR�s that

have a degree of gold backing. The BIS now has a total of 12.4% of its

deposits (32B SDR) in the form gold deposits. Note #11 to the BIS

financial statements states: �Gold deposits placed with the Bank originate

entirely from Central Banks. They are all designated as financial

liabilities measured as amortized cost�.

ARE WE SETTING THE PINS UP FOR AN ALTERNATIVE RESERVE CURRENCY?

Are we moving towards

the BIS and IMF being fractional reserve banks that will create money &

credit - a reserve currency that will satisfy Russia and China with an

element of Gold backing? A bank such as the BIS could easily assume this

role (if it hasn�t already) as could the IMF with possible banking charter

adjustments.

The chances are high

that this is the roadmap we will find ourselves taking. Like all banking

that started as Gold backed you could expect that in this case the little

gold backing that starts the process is quickly diminished so a limitless

money machine could begin functioning. The gold backing would likely be an

initial requirement by Russia and China. The partial gold backing would

lend credibility to the acceptance and a possible reserve currency

alternative and eventual establishment as the global reserve currency.

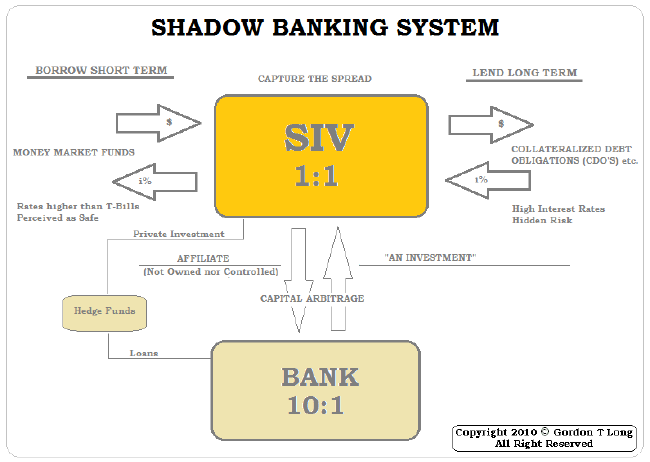

SHADOW BANKING REPLACEMENT

The collapse of the

Shadow Banking system and its attendant SIV / CDO structures were at the

root of the financial crisis. That structure which is representative of a

huge amount of the credit growth since the dotcom bubble burst isn�t

coming back soon, if ever. The world needs more liquidity than the central

banks or sovereign treasuries can currently deliver politically. The

central bankers, huddled in their bimonthly

board meeting at the BIS in

Basel, Switzerland, know this better than anyone. Their discussions in the

very halls of the BIS must resonate with them to use all the tools

available at their disposal - quickly.

board meeting at the BIS in

Basel, Switzerland, know this better than anyone. Their discussions in the

very halls of the BIS must resonate with them to use all the tools

available at their disposal - quickly.

Paul McCulley and

Richard Clarida at

Pacific Investment Management Co. (PIMCO) have written

extensively about the Shadow Banking System and its growth. An extensive

slide presentation on the Shadow Banking System can be found on my web

site at

TIPPING POINTS. I won�t go into the detail here,

but suffice it to say that the shadow banking system collapse has created

a massive hole in credit creation that central bankers can�t fill in the

manner in which they presently appear to be approaching the problem. Of

course appearances can be deceiving

The problem has now

reached crisis proportions and the central bankers know they must urgently

act in a coordinated manner. Deflation now has a firm hand on the global

economy and this must be reversed. I have been calling for a US

Quantitative Easing QE II of $5T in my writings for some time. This amount

is required for the US alone. The entire global requirement is three to

four times this amount.

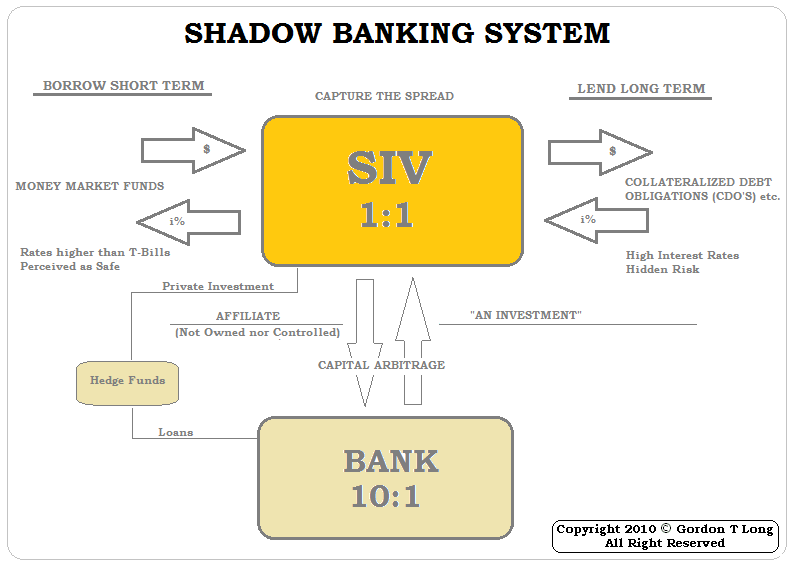

The above chart serves

as an illustration to simplify the essence of the Shadow Banking System .

The international bankers prefer to refer to the process as Capital

Arbitrage. An arms-length agreement allowed the banks to invest in a

Structured Investment Vehicle (SIV) as an affiliate investment. The large

spread that an SIV captured made it an excellent investment, but more

importantly it allowed the banks to use their fractional reserve (10X)

money creation abilities to buy risky securitization products without them

appearing on their balance sheet. The banks received huge multiplier

leveraged returns from the high yielding Collateralized Debt Obligations (CDOs)

until the crisis imploded the game.

When the financial

crisis unfolded you may recall that then US Treasury Secretary Hank

Paulson�s (former Chairman and CEO of Goldman Sachs during the explosion

of Shadow Banking structures) first solution was to create a $100B Super

SIV. The SIV leverage thinking was so entrenched that this was the first

�go to� solution to fight de-leveraging. If we were to jump forward to

today when we are further along in increasing and unprecedented

de-leveraging, what the central bankers need to replace the shadow banking

system is a vehicle that will deliver the previous scale of leverage PLUS

an order of magnitude more. The answer is the Bank of International

Settlements. The SIV model is used as illustrated �Shadow Central Banking

System� above.

With the use of the SDR �currency�, central bankers can compound

fractional reserve lending.

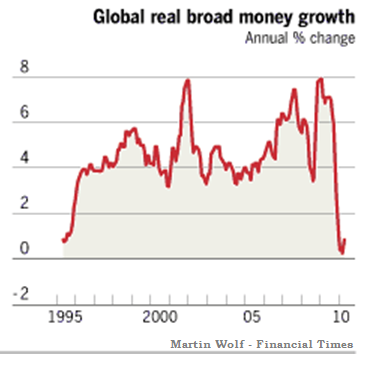

IT�S ALREADY HAPPENING

It is my view this

process is already well along. The following Bloomberg global money supply

growth chart graphically shows this. As the circles indicate, once again

money is flowing into the pipeline or at least into global bank reserves.

CONCLUSION

The advantage of this

approach is:

1.

Leverage: Compounding

money creation between banks

2.

Partial gold backing:

Present BIS levels of 12.4%

3.

SDR: Offers a basket of

currencies approach versus a single currency dependency.

4.

Former Communist bloc

regime backing: China and Russia would likely support this approach for a

number of reasons, which they have already expressed as short comings to

the current global reserve situation.

5.

Reserve Currency: The

SDR approach offers a migration path from today�s US$ reserve currency to

an alternative bank reserve currency to a future global reserve currency.

This may be the final lever required to initiate a Minsky Melt-Up (see:

EXTEND &

PRETEND - Manufacturing a Minsky Melt-Up)

and the $5T in QE II (see:

EXTEND &

PRETEND: A Guide to the Road Ahead)

I have been writing about for some time now.

There are many questions

that are raised in the above discussion - many about the future role and

safety of gold. Time and space don�t allow for this here. I hope to work

through the answers in forthcoming articles.

If you would like to be notified as the articles are released, then

sign-up and additionally follow

the ongoing daily developments at

Tipping Points.

The following gave me concern when I

first read it many years ago and something for you to think about:

"...the powers of financial capitalism had another far-reaching aim,

nothing less than to create a world system of financial control in private

hands able to dominate the political system of each country and the

economy of the world as a whole. This system was to be controlled in a

feudalist

fashion by the central banks of the world acting in concert, by secret

agreements arrived at in frequent private meetings and conferences. The

apex of the system was to be the Bank for International Settlements in

Basel, Switzerland, a private bank owned and controlled by the world's

central banks which were themselves private corporations."

Professor Carroll Quigley

Tragedy and Hope: A History of the World in Our Time (1966)

President Bill Clinton�s Georgetown Professor

Sign Up for the next release in the

Sultans of Swap series:

Commentary

Gordon T Long

Tipping Points

Mr. Long is a former senior group executive with IBM & Motorola, a

principal in a high tech public start-up and founder of a private venture

capital fund. He is presently involved in private equity placements

internationally along with proprietary trading involving the development &

application of Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment

advice. His comments are an expression of opinion only and should not be

construed in any manner whatsoever as recommendations to buy or sell a

stock, option, future, bond, commodity or any other financial instrument

at any time. While he believes his statements to be true, they always

depend on the reliability of his own credible sources. Of course, he

recommends that you consult with a qualified investment advisor, one

licensed by appropriate regulatory agencies in your legal jurisdiction,

before making any investment decisions, and barring that, you are

encouraged to confirm the facts on your own before making important

investment commitments.

� Copyright 2010 Gordon T Long. The information herein was obtained from

sources which Mr. Long believes reliable, but he does not guarantee its

accuracy. None of the information, advertisements, website links, or any

opinions expressed constitutes a solicitation of the purchase or sale of

any securities or commodities. Please note that Mr. Long may already have

invested or may from time to time invest in securities that are

recommended or otherwise covered on this website. Mr. Long does not intend

to disclose the extent of any current holdings or future transactions with

respect to any particular security. You should consider this possibility

before investing in any security based upon statements and information

contained in any report, post, comment or recommendation you receive from

him.

Fair Use

Notice

Fair Use Notice

This site contains

copyrighted material the use of which has not always been specifically

authorized by the copyright owner. We are making such material available in

our efforts to advance understanding of environmental, political, human

rights, economic, democracy, scientific, and social justice issues, etc. We

believe this constitutes a 'fair use' of any such copyrighted material as

provided for in section 107 of the US Copyright Law. In accordance with

Title 17 U.S.C. Section 107, the material on this site is distributed

without profit to those who have expressed a prior interest in receiving the

included information for research and educational purposes.

If you wish to use

copyrighted material from this site for purposes of your own that go beyond

'fair use', you must obtain permission from the copyright owner.