EXTEND

& PRETEND:

Manufacturing a Minsky Melt-Up!

A distracted and preoccupied amateur is no match for a determined,

organized professional with a strategy. Though the collapse of the shadow

banking system was a near fatal miscue for the global bankers, they have

been quick to adjust their strategy. With an army of MBAs, quants and

lobbyists they have reworked their strategy at the expense of the still

comatose and shaken taxpayer.

It is the first anniversary since April 2nd when FASB 157 was

suspended and with it the suspension of �mark-to market� accounting. The

US congress held a gun to the head of the Financial Accounting Standards

Board a year ago. Congress left FASB no choice but to change their

guidelines under the perception that it was a deferral allowing time for the

banks to adjust the toxic and devalued assets on their books. Where are we a year

later with Mark-to Market still �on hold� and Mark-to-Myth endorsed by the

Federal Reserve Bank examiners? Frankly, the �happy face� media doesn�t

want to talk about it, so I will. As an investor, unlike politicians and

the media, I must face reality or I will pay the ugly consequences.

In January's

EXTEND & PRETEND - An Accounting Driven Market Recovery,

I outlined the accounting changes that had been implemented to ignite a

market reversal and rally from the March 2009 low. These accounting

changes ranged from the deferral of FASB 157 in March 2009, the Commercial

Real Estate Loan Workout Policy in October 2009, the three cauldrons

easing in November 2009, the deferral of FASB 166 and 167 in December 2009

and the System Wide Federal Bank Examiner Reinforcement Training in

January 2010. The changes were executed in a controlled and almost

militaristic operation. The market has reacted with a

58.4%

retracement of the 2008 decline and a 70%

increase from the lows in the DOW industrial, trumpeted eagerly by the

nightly news. This was Stage I.

Before we discuss Stage II, which will be the manufacturing of a

�Minsky Melt-Up�, let�s briefly review the extent to which Stage I has

created distortions in the accounting of public traded financial

fiduciaries. We will then be able to see clearly how they have created the

launch pad for Stage II.

STAGE I � AN ACCOUNTING

ORCHESTRATED RALLY

The Friday Night Lottery

Almost every Friday night the FDIC seizes from

1 to 5 local or regional banks as insolvent failures. Saturday morning

we wake to find these bankrupt banks have been magically merged with

another bank. It all seems so normal. But does that speed and ease sound

realistic to you?

According

to Karl Denninger at

The Market Ticker who follows these matters very closely, on

March 6th he reported:

I am

constantly amused by those people who claim there is some vast

"conspiracy" in this country when it comes to banks, balance sheets, and

fraudulent lending and accounting. There is no conspiracy. It is, in

fact, "in your face" fraud. The FDIC does us the courtesy of explaining

it virtually every Friday night,

right on their web page. I am simply

going to take last night's bank closures, which numbered four. One of

them has no "deposit insurance fund" estimated loss available, because

they didn't find someone to take the assets - they're just mailing

checks. But the other three do.

1-

Waterford Bank, Germantown MD: $155.6 million in assets, $156.4 in insured deposits. They were

"underwater" by $800,000, right? Wrong: Estimated loss, $51

million. That is, the assets of $155.6 million were overvalued

by approximately 30% at the time of seizure.

2-

Bank of Illinois, Normal IL: $211.7 million in assets, $198.5 million in deposits. They were

"underwater" by $13.2 million (which is why they were seized), right?

Wrong: Estimated loss $53.7 million. That is, the the assets

of $211.7 million were overvalued by more than 25% at the time of

seizure.

3-

Sun American Bank, Boca Raton FL: $535.7

million in assets (so they claimed anyway), $443.5 million in total

deposits. Heh, why did you seize them - they have more assets than

liabilities? Oh wait: Estimated loss: $103.8 million, so the

actual assets are worth $443.5 - $103.8, or $339.7 million. That is,

the assets of $535.7 million were overvalued by a whopping 37% at the

time of seizure.

This

isn't new, by the way.

In August of 2009 I went

through Colonial Bank's failure based on BB&T's presentation to its

shareholders on the "merger" - and gift it was given by the FDIC. It

too showed that Colonial had been carrying assets on their books at a

ridiculous 37% above where BB&T ultimately marked them as a

whole.

Folks,

your bank is being assessed deposit insurance premiums to pay for these

losses. You are paying these losses through increased

fees and interest expense on your credit cards and all other manner of

borrowing. You are paying for outrageous, pernicious and endemic

balance sheet fraud. There is no conspiracy. It is right under your

nose. One of these three banks, based on their balance sheet, wasn't

even underwater - it was "to the good" by nearly $100 million dollars.

The balance sheet was a flat, bald-faced lie. You want to sit for

this? Why should you?

Now

let's ask the inconvenient question:

Are the

big banks - specifically, Citibank, Bank of America, Wells Fargo and JP

Morgan - all similarly overvaluing their assets?

Why

should we believe they are not? You can go through more than a year's

worth of FDIC bank seizure information and in essentially every

single case you will find that overvaluations of somewhere from

20-50% have in fact occurred, yet not one indictment for

book-cooking has issued.

So let's

be generous and assume that the "big banks" are over-valuing their

assets by 25% - the lower end of the range of what the FDIC says is,

through actual experience, what's going on, and add it all up.

Bank of America shows $2.25

trillion in assets.

Citibank shows $1.89 trillion in

assets.

JP Morgan/Chase shows $2.04

trillion in assets.

Wells Fargo shows $1.31 trillion in

assets.

This

totals $7.49 trillion smackers.

The

FDIC's experience with seizing banks thus far suggests quite strongly

that all four of these entities are lying about these valuations, and

that were they to be seized the loss embedded in them (and for which

you, the taxpayer would be responsible) is somewhere

between $1.49 and $2.99 trillion dollars.

Incidentally, neither the FDIC or Treasury happens to have either

$1.49 or $2.99 trillion laying around, and it is highly questionable if

they could raise it, should that become necessary. Now of course neither you or I can prove this is correct.

However, we can look at the FDIC's own published bank closing

statements, and derive from them a pattern stretching back more than a

year now that has disclosed that in essentially each and every

case the banks in question have overvalued their assets by

anywhere from 20-40%, and that as of the day of the seizure

such an overvaluation was in fact a continuing and ongoing practice. (1)

This was precisely what was in the process of happening, as I

outlined in

EXTEND & PRETEND - An Accounting Driven Market Recovery.

If you were a bank, why would you lend to small business or the consumer

with their inherent risks when you could play the Friday Night Lottery? As

A bank CEO you would ensure that you have plenty of cash ready to buy and take

over the depositors (whose assets you desperately need), while having most

of the bad debt written off and then likely getting very favorable FDIC

guarantees for quickly taking the banks off FDIC�s highly depleted balance

sheets. I imagine every US bank CEO & his/her Board of Directors watch these results closer than the March Madness basketball rankings!

To facilitate these bankrupt banks being taken over so quickly, there is

obviously a considerable amount of very secret negotiations (non transparent, non public bidding) taking place behind the scenes.

Like we saw with TARP (Troubled Asset Relief Program), it is amazing how

much money gets spilled when everyone is in a frenzy to feed at the

government trough.

It�s Only

Going to Get Worse

The

biggest financial issue with local and regional banks is their commercial

real estate loans with building and construction loans being the worst.

The official government stance as stated in the

February report from the Congressional

Oversight Panel makes for sobering reading. It forecasts $200

to $300 billion in losses coming from commercial real estate (CRE) loans. The

report notes these were not considered in the famed stress tests, since

that process looked only through 2010, when the losses from CRE will peak

later. It outlines that:

-

Between 2010 and 2014, about

$1.4 trillion in commercial real estate loans will reach the end of

their terms. Nearly half are are presently underwater, that is the

borrower owes more than the underlying property is currently worth.

-

Commercial property values have

fallen more than 40 percent since the beginning of 2007.

-

Increased vacancy rates, which

now range from 8 percent for multifamily housing to 18 percent for

office buildings, and falling rents, which have declined 40 percent for

office space and 33 percent for retail space, have exerted a powerful

downward pressure on the value of commercial properties.

-

The largest commercial real

estate loan losses are projected for 2011 and beyond; losses at banks

alone could range as high as $200-$300 billion.

-

The stress tests conducted last

year for 19 major financial institutions examined their capital reserves

only through the end of 2010. Even more significantly, small and

mid-sized banks were never subjected to any exercise comparable to the

stress tests, despite the fact that small and mid-sized banks are

proportionately even more exposed than their larger counterparts to

commercial real estate loan losses.

-

A significant wave of

commercial mortgage defaults would trigger economic damage that could

touch the lives of nearly every American.

-

Empty office complexes, hotels,

and retail stores could lead directly to lost jobs. Foreclosures on

apartment complexes could push families out of their residences, even if

they had never missed a rent payment. Banks that suffer, or are afraid

of suffering, commercial mortgage losses could grow even more reluctant

to lend, which could in turn further reduce access to credit for more

businesses and families and accelerate a negative economic cycle.

-

It is difficult to predict

either the number of foreclosures to come or who will be most

immediately affected. In the worst case scenario, hundreds more

community and mid-sized banks could face insolvency. Because these banks

play a critical role in financing the small businesses that could help

the American economy create new jobs, their widespread failure could

disrupt local communities, undermine the economic recovery, and extend

an already painful recession.

The

Chair of the Congressional Oversight Panel, Elizabeth Warren, in

an interview with Charlie Rose on NPR stated:

CHARLIE

ROSE: Commercial real estate, what are we looking at.

ELIZABETH WARREN: Oh golly -- 2,988 banks that by the terms of their

own regulators are too concentrated in commercial real estate. These

are the medium size banks. By the end of this year, half of all

commercial real estate loans will be underwater, and they are coming in

�11, �12 and �13.

The reason this is such a bad problem anyway -- think about that, nearly

3,000 banks out of a total of 8,000 -- it�s the very banks that do

small business lending who are about to get socked in the nose on real

estate, commercial real estate losses.

CHARLIE ROSE: So we�ll see banks going under because they�ve got too

many loans out there are not being repaid?

ELIZABETH WARREN: We�re seeing banks that don�t want to lend because

they see every dollar that comes in the door and say "I�ve got to hold

on to it to try to fill my commercial real estate hole or else I will be

gone."

Home Equity Loans (HELOCS)

I find it amazing that with all the talk about government programs to keep

people in their foreclosed homes, with government incentives to increase

home sales, with new home construction at a near standstill and home

prices finally reaching some sort of bottom (near term), we never talk

about the billions of Home Equity Loans that were taken out from 1996

onward. Does it pass your common sense test that people would stop

paying their mortgage, car payments, credit cards and yet still pay their

Home Equity Loan? I don�t think so. But the banks have written down next

to nothing here. This is the issue with Mortgage write-down. If you write

down the mortgage, by definition the Home Equity Loan is now a 100%

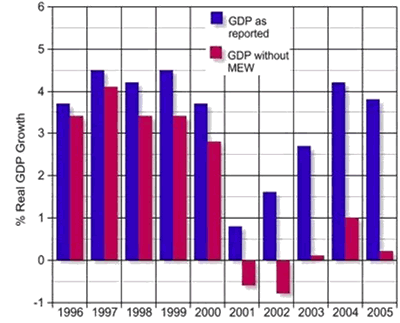

write-off. Ouch! Doesn�t anyone remember this graph which was so prevalent

only a few years ago?

This is an absolute huge problem and is presently being hidden behind

all the mortgage foreclosure coverage. Amherst Securities, according to

Reuters " has said "commercial banks hold approximately $767 billion

of the total $1.05 Trillion of second mortgages outstanding, with the Big

4 holding over $400 billion alone."

Reuters

estimates that if the banks mark down the entire portion of home equity

debt that exceeds home value values, the net of estimated reserves would

be:

$37.2 billion for Wells Fargo

$29.9 billion for JP Morgan

$28.6 billion for Bank of

America

$11.5 billion for Citi

=====

$107.2 billion

If we were to write down these unsecured home equity lines by only 40%,

then the potential increase in regulatory capital for these 4 banks

increases by: $3.1B for Wells Fargo, $1.3B for JP Morgan, $2.1B for Bank

of America and $1.0B for Citigroup. Nothing is

being done, nor is anything being forced by Federal Reserve Bank examiners

to be done.

I could go on about shadow housing inventory, �jingle� mail and �strategic

defaults�, the python in the pipe with Option-ARMS, the failure of HAMP

etc., but I am sure you have heard all you want to hear about housing to

know the banks have yet to effectively address the issue. Like landmines

the issues still lay on their balance sheets.

Because of

this situation,

the banks still minimally

require

40% higher collateral values. So how are they going to get it?

STAGE II --

MANUFACTURING A MINSKY MELT-UP

My

grandfather, who was proud to keep his farm during the depression, had an

expression that I haven�t heard in a long time. He was fond of warning that:

�Banks lend you an umbrella when it is sunny and then demand it back when

it starts to rain!� It has been a long time since we have had a �rainy�

economy for any protracted period of time, but to this prairie farm boy

the economic weather forecast doesn�t look that good.

My

grandfather, who was proud to keep his farm during the depression, had an

expression that I haven�t heard in a long time. He was fond of warning that:

�Banks lend you an umbrella when it is sunny and then demand it back when

it starts to rain!� It has been a long time since we have had a �rainy�

economy for any protracted period of time, but to this prairie farm boy

the economic weather forecast doesn�t look that good.

We therefore need to remember some basics of banking. First, banks make

money borrowing short and lending long. This strategy is inherently risky.

This is why banking requires extensive regulatory laws and ever vigilant

bank examiners. Neither are to be �tampered� with, which our politicians

now seem oblivious to.

Secondly, inflation and deflation are different for banks. The Consumer

Price Index and how much food, energy, consumer staples etc have increased

is not highly relevant to banks. Inflation or deflation to banks is about

asset price increases or decreases. It is about whether their collateral

positions are increasing or decreasing. I don�t mean to be too simplistic

here since cost of money is critically important, but it serves to make

the point that bank strategy is driven by their view of the direction of

asset prices and whether their loans are covered, their capital ratio

requirements are secure or what a new risk adjusted loan is worth to them.

What does this chart to the right say about where banks view asset prices

to be headed?

Banks win

on asset inflation. Banks potentially lose on asset deflation.

Rising

asset prices:

1- Make

Collateral more valuable or easier to secure for banks

2- Raise

borrowing levels with which to finance higher priced asset prices which

increase interest payments and fees.

If banks thought collateral values were headed lower, here is what they

would do:

|

1-

Freeze new loans secured by collateral that will potentially

deflate |

In

Process |

|

2-

Seize existing loan collateral on defaulted loans before collateral

falls below book value |

In

Process |

|

3-

Demand higher collateral levels for loans |

In

Process |

|

4-

Charge higher rates and tighter terms |

In

Process |

Banks need asset values to continue to climb. Now that the markets have

reached �nose bleed� levels and appear to be at the stage of looking for a

consolidation, the banks need another strategy to ignite asset prices

further. The banks must see higher asset prices to have any hope of

achieving satisfactory Capital Ratios with the known amounts of bad and

toxic debt still on their books. Is it any wonder banks are now making

their profits primarily in their trading operations driving asset prices

higher and with their Interest Swap where they are squeezing collateral

call levels? (see:

SULTANS OF SWAP: The Get

Away!)

MANUFACTURING A MINKSY MELT �UP

If the banks wanted to get collateral values up, and manufacture a �Minsky

Melt-Up' here is what some of their strategy elements would call for:

I am not saying that a successful Minsky Melt-Up will be achieved or in

fact could be successfully manufactured. Frankly, I would be very skeptical

if it weren�t for the fact that former Federal Reserve Chairman Alan

Greenspan specifically said this could not happen (He also stated that

market bubbles could not be identified by the Fed nor addressed with

Monetary Policy (yeh right)). His views

have typically been my contrarian indicator which has given me an

investment edge over the years.

Before reading Alan Greenspan�s �Greenspeak�, consider that we presently have

unstable economic policies, risk premiums have been high and the Fed has

successfully inflated a bubble in the Bond Market over the last 20 months

through QE (Quantitative Easing).

�Greenspan said

�because the markets themselves are asymmetric: they melt down, but

don�t melt up!� Mr. Greenspan argues:

(1) the ironic result of successful stabilization policies is a journey

to excessively-thin risk premiums, and if

(2) history has not dealt kindly with the aftermath of protracted

periods of low risk premiums, and if

(3) asset prices do not tend to melt up but do tend to melt down,

then

(4) logic implies that the fattest fat-tailed secular risk to price

stability is deflation, not inflation.

How so? If bubbles are the ironic externality of successful

stabilization policies, then those policies can be successful only so

long as there are asset classes that the central bank can inflate into a

bubble. When there are no more free and clear assets to lever up, the

game ends in a debt-deflation. As the great Hyman Minsky intoned,

stability is ultimately destabilizing! That is the logical consequence

of too-successful inflation stabilization. Don�t call it a conundrum,

but rather a dilemma, if the Fed were to set and achieve a too-narrow

target zone for inflation. (2)

If according to Hyman Minsky, protracted periods of market stability leads

to instability and a market meltdown, does this preclude therefore that

protracted periods of market instability negate the possibility of a

market melt-up (per Greenspan)? I intentionally phrased the logic

for this argument in perfect �Greenspeak� fashion so we can all remember

exactly how we got ourselves into this global predicament in the first

place.

CONCLUSION

This is a

well executed strategy. It has been almost militaristic in its execution -

all the elements from a solid communications program (i.e. CNBS hype),

accounting and regulatory changes (FASB 157, 166, 167 deferrals et al ),

government statistics (does anyone actually still believe the CPI, Labor

Report or other

government statistics

any more?), and public�s sentiment through the controlled market

perception barometer pumped at them every evening on how well the DOW

Industrials are doing. The US economic and financial situation has now

reached a point where the potential crisis could be referred to by our

government interventionists as a matter of national security. This is

precisely why I am leaning towards a Minsky Melt-Up being successfully

manufactured.

There is an old market saying: �Don�t fight the Fed!� This market

guideline has never been truer. In fact today it is more appropriate to

say:

�It is impossible to fight central bank planning�

To fight the central party planning (i.e. shorting an artificial market)

exposes your wealth to being officially confiscated!

Sounds like something

Karl Marx would have said?

Sign Up for the next release in the

Extend & Pretend series:

Commentary

SOURCES:

(1)

03-06-10

All

You Need To Know About Bank Balance-Sheet Fraud

The Market Ticker

(2) 08-03-06

Paul McCulley and Doug Noland Both Praise Hyman Minsky

Economic Dreams

(3) 04-06-10

New NYSE Options Pricing Pyramid Promotes Derivative Driven

Market Melt-Up Zero Hedge

(4) 04-08-10

Home equity horror

Reuters

The last Extend & Pretend article:

EXTEND & PRETEND - Hitting the Maturity Wall!

Gordon T Long

Tipping Points

Mr. Long is a former senior group executive with IBM & Motorola, a

principle in a high tech public start-up and founder of a private venture

capital fund. He is presently involved in private equity placements

internationally along with proprietary trading involving the development &

application of Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment

advice. His comments are an expression of opinion only and should not be

construed in any manner whatsoever as recommendations to buy or sell a

stock, option, future, bond, commodity or any other financial instrument

at any time. While he believes his statements to be true, they always

depend on the reliability of his own credible sources. Of course, he

recommends that you consult with a qualified investment advisor, one

licensed by appropriate regulatory agencies in your legal jurisdiction,

before making any investment decisions, and barring that, you are

encouraged to confirm the facts on your own before making important

investment commitments.

� Copyright 2010 Gordon T Long. The information herein was obtained from

sources which Mr. Long believes reliable, but he does not guarantee its

accuracy. None of the information, advertisements, website links, or any

opinions expressed constitutes a solicitation of the purchase or sale of

any securities or commodities. Please note that Mr. Long may already have

invested or may from time to time invest in securities that are

recommended or otherwise covered on this website. Mr. Long does not intend

to disclose the extent of any current holdings or future transactions with

respect to any particular security. You should consider this possibility

before investing in any security based upon statements and information

contained in any report, post, comment or recommendation you receive from

him.