We maintain that this will likely fall this low before the downside of the credit cycle is finished. With earnings now, a single digit p/e would imply an S&P 500 below 1109; a whopping 40% below current levels.

We like to consider the longest time periods available to find reliable historical trends in data series. Of these, the price/earnings ratio (p/e ratio) of the S&P 500 index is instructive to study. Major bull markets in equities tend to start from heavily disfavored markets; those with earnings multiples (p/e ratios) in the single digits.In a sense, investors have to give up hope in the stock market before it can regain popularity. In the chart below, you will see that price/earnings ratios around 6 or 7 have preceded long equity bull markets.

Yet, for all the upheaval in the markets over the last 16 years, the US stock market has not yet fallen to single digit p/e ratios. The S&P 500 p/e ratio is currently about 16 and it has been 33 years since the index last traded with p/e below ten. We maintain that this will likely fall this low before the downside of the credit cycle is finished. With earnings now, a single digit p/e would imply an S&P 500 below 1109; a whopping 40% below current levels.

It is important to note that these are glacial processes and we aren't predicting this to happen on any particular schedule, but markets in 2016 have returned to a sense of fear and we just want to remind readers that there is a lot of space between 1870 and 1100 in the S&P 500.

The Fragile Forty

How The World Lost

$17 Trillion In 6 Months

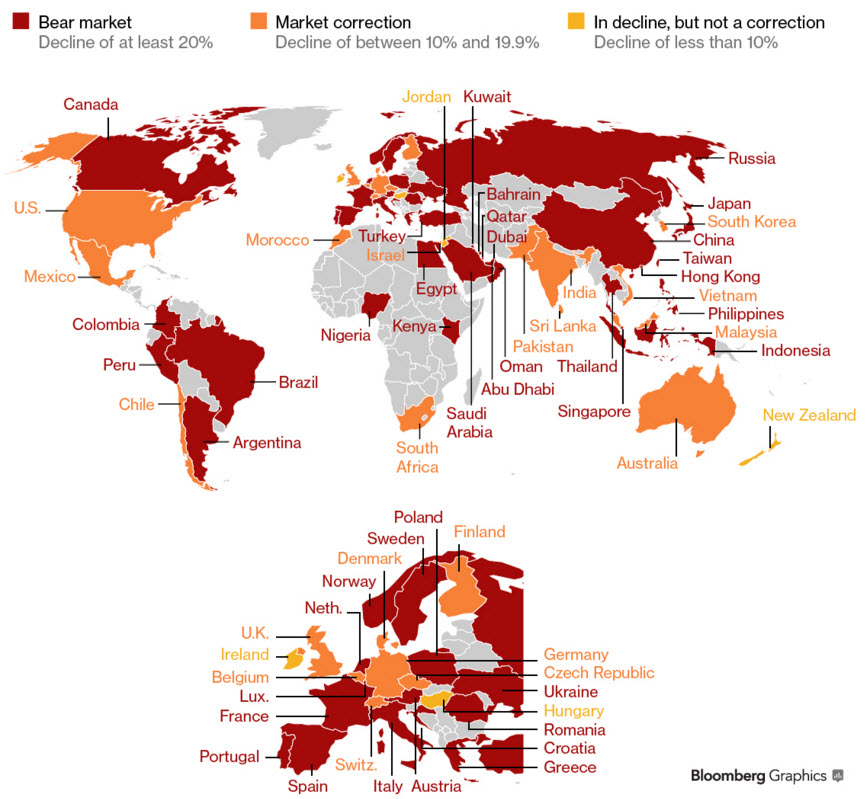

It's official. More than 50% of the "wealth" effect created from the 2011 lows to the 2015 highs has been destroyed (despite the world's central banks going into money-printing overdrive over that period). Almost $17 trillion of equity market capitalization has evaporated in just over 6 months with over 40 global stock indices in bear markets...

The U.K. was the latest market to fall 20 percent from its peak, while India is less than 1 percent away from crossing the threshold that traders describe as the onset of bear market.Nineteen countries with $30 trillion have declined between 10 percent and 20 percent, thereby entering a so-called correction, according to data compiled by Bloomberg from the 63 biggest markets on Wednesday.

Emerging nations bore the brunt of the meltdown, accounting for two out of every three bear markets. Slowing Chinese growth, the 24 percent slump in oil this year and currency volatility have driven developing-nation stocks to the worst start to a year on record.

Among equity indexes that are on the cusp of entering bear territory are Australia, India and the Czech Republic, each having fallen about 19 percent from their rally highs. New Zealand and Hungary are putting up the best resistance to the turmoil, limiting their losses to less than 7 percent.

So just before you (Jim Cramer et al.) demand the central banks do more, just remember what reality looks like - will you use any centrally-planned rally to buy moar or sell into as the smoke and mirrors of yet another bubble is exposed with the business cycle inevitably beating the rigging...

TIPPING POINTS, STUDIES, THESIS, THEMES & SII

COVERAGE THIS WEEK PREVIOUSLY POSTED - (BELOW)

MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - Jan 10th, 2016 - Jan 16th, 2016

TIPPING POINTS - This Week - Normally a Tuesday Focus

BOND BUBBLE

1

RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates

2

RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates

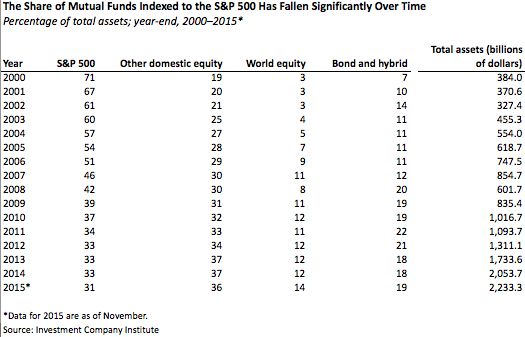

As volatility in the stock market grows, a handful of experts are raising an alarm about the rise of index ETFs and mutual funds, which has never accounted for this much of the market before.

They warn that the unprecedented amount of index ETFs trading in the market — index ETFs accounted for nearly 30 percent of the trading in the U.S. equities market last summer — could magnify, or even cause, flash crashes.

In turn, that may put individual investors, who are increasingly invested in index funds, more at risk. And many may not realize how exposed they are to the risks of a relatively small group of stocks held in the major indexes, said experts.

Siegfried Layda | Getty Images

Tim McCarthy, a former president of San Francisco-based Charles Schwab and Japan's Nikko Asset Management, has been a longtime proponent of index investing. But he now advises that investors diversify their investment styles as well as their asset classes.

He suggested investors move 25 percent to 50 percent of their equity portfolios into actively managed absolute return funds, preferably those with a 10-year track record and a relatively small amount of assets of between $1 billion to $2 billion. (Research has shown over the years that active managers stand their best chance of success before their assets under management grows too high.)

As always, he said, investors should look for low fees.

A stock bubble in index funds

He said he has grown increasingly uneasy about the risks based on the hypergrowth of index funds, and the price difference between stocks outside and inside index funds.

From 2007 through 2014, index domestic equity mutual funds and ETFs received $1 trillion in net new cash and reinvested dividends, according to the Washington, D.C.-based Investment Company Institute. In contrast, actively managed domestic equity mutual funds experienced a net outflow of $659 billion, including reinvested dividends, from 2007 to 2014.

Meanwhile, the price of the underlying equities in index funds is rising, though no one is sure exactly why. Research by S&P Capital IQ, as of Dec. 31, found stocks that were in the Russell 2000 were trading at a 50 percent premium to stocks that were not, up from 12 percent in 2006. The statistics are based on median price-to-book ratio.

That kind of price difference is seen by some as a kind of canary in the coal mine, indicating that there is a bubble in the stocks of companies held in index funds — and that their prices could come down further and faster than other stocks in a downturn. In turn, that could put pressure on the share prices of the index mutual funds and ETFs themselves.

"It's complicated, but it could be a very big problem," said David Pope, managing director of quantamental research at S&P Capital IQ. He and colleague Frank Zhao studied the liquidity in the market for the S&P 500 last summer and identified the 10 stocks that had the biggest difference in liquidity at that time, compared with the index. They included ExxonMobil, Berkshire Hathaway, Johnson & Johnson,Microsoft, General Electric, Wells Fargo, Procter & Gamble, JPMorgan Chase, Pfizer and PepsiCo.

"A structural problem may arise when the liquidity demanded by the ETF exceeds the liquidity availability of some of the underlying holdings," they wrote.

Basically, if an investor wants to sell an index fund as the market declines, the managers of the fund might have trouble selling some of the stocks in the fund. An active manager could choose to sell any stock in her fund and thus potentially navigate a downturn better. But an index fund manager has to sell exactly the shares held in the index in the same proportion as demanded by the index. If the fund manager doesn't find a buyer for, say, shares of ExxonMobil, the price of ExxonMobil will fall until a buyer is found.

Assessing the risks

While market theorists have always recognized this as a potential problem for index investing, no one has been sure exactly how it would play out or when problems might arise. As long as there are enough buyers and sellers actively setting prices and trading, index funds and stocks should pose no extra risk. It's just that no one is sure exactly how many is enough.

Indeed, not everyone thinks McCarthy is right, and others point to different risks as bigger causes for concern, including the unknown impact of the way that high-frequency traders place orders.

"So we have two new factors when it comes to a potential market situation," said John Rekenthaler, vice president of research for Chicago-based Morningstar. "There are always new factors. Most of the time, new factors don't play out according to expectations."

He pointed out that two decades ago, people worried about what the impact of 401(k)s would be in the market and whether non-professional investors would be apt to sell more quickly in a downturn. The opposite turned out to be the case.

Even if the risk posed by index investing is rising, the growth in index funds doesn't necessarily pose a huge system risk, pointed out Sean Collins, senior director of industry and financial analysis for the Washington, D.C.-based Investment Company Institute. "The share of assets going into index funds is rising. Does that necessarily cause markets to be dysfunctional? The answer is no," he said.

He pointed out how much more diversity there is now in index investing. Much of the money flowing into index funds has been going into markets in which there hasn't been much indexing before, including emerging markets equities and bond markets.

McCarthy said investors would be wise to look at their portfolios with the emerging risk of index funds in mind. There's not much an individual investor can do to guard against the risks posed by high-frequency trading, short of bowing out of the market entirely.

What investors should do

But there are some steps investors could take to manage the risks posed by an index fund-dominated market.

In addition to investing some of their stock portfolios in actively managed funds, McCarthy suggests investors take a hard look at how diversified they are.

First, he said, an investor could make sure he or she isn't double-exposed to the same stocks. He cited the case of a friend of his, a doctor, who had invested in blue-chip stocks, some mutual funds and in an S&P 500 fund that turned out to hold — guess what — many of the same blue chips and tech stocks. In the downturn in 2000–2001, he lost 50 percent of his portfolio.

Every market is different, McCarthy said. But in part because of the flow of money into index funds, the U.S. equities market has become more dominated by a handful of big technology stocks. That's something that index fund investors, like his doctor friend, may not easily recognize now.

As someone who has managed the back end of trading systems, McCarthy said he is increasingly uneasy about the level of index investing and has begun to give speeches about the potential dangers of a market in which a growing number of managers are hamstrung by the requirement that they match their indexes.

But he knows that he's at the leading edge of people talking about it — and that many think he is warning too hard and too fast. "This is unfamiliar territory for me," he acknowledged. "But index investing has so much power, and it's derivative-priced.

"Sometimes it's better to be vaguely right than exactly wrong," he said.

— By Elizabeth MacBride, special to CNBC.com

GEO-POLITICAL EVENT

3

CHINA BUBBLE

4

JAPAN - DEBT DEFLATION

5

EU BANKING CRISIS

6

TO TOP

MACRO News Items of Importance - This Week

GLOBAL MACRO REPORTS & ANALYSIS

US ECONOMIC REPORTS & ANALYSIS

CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES

Market - WEDNESDAY STUDIES

STUDIES - MACRO pdf

TECHNICALS & MARKET

Market - WEDNESDAY STUDIES

STUDIES - MACRO pdf

TECHNICALS & MARKET

01-20-16

Profit, Multiple & Margin Trouble Are In Store For Global Equities In 2016

The U.S. dollar has recently been negatively correlated both with the MSCI All-Country World Index (ACWI) and deep cyclical sectors. Given that the U.S. comprises over 50% of the MSCI ACWI, a firming in the U.S. dollar eats into U.S. corporate sector profitability via negative translation effects and the importing of global deflation. In fact, global EPS have been contracting for three consecutive quarters and according to our model will remain under pressure in 2016. Now P/E multiples are under pressure. Since the late 1970’s the forward P/E multiple for the S&P 500 has compressed at the onset of fresh Fed tightening cycles. Consequently, global equity markets are unlikely to make any significant headway in 2016, especially as margin pressures intensify. Instead, the risks are heavily titled to the downside, making a capital preservation portfolio mindset a necessity.

For additional information on Global Alpha Sector Strategy’s Quarterly Review & Outlook please visit the website at gss.bcaresearch.com.

Hopes fading for global profits, once seen as equity catalyst

Forecasts are still too high for 2016, market watchers say

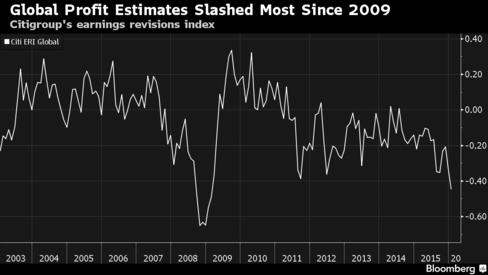

Stocks are losing their last line of defense.

Amid a selloff that erased more than two years of gains -- about $14 trillion -- from global stocks now on the brink of a bear market, at least earnings stood as a potential bright spot. Those hopes are fading: analyst profit downgrades outnumbered upgrades by the most since 2009 last week, according to monthly data from a Citigroup Inc. index that tracks such changes.

Declines in oil and and other commodities, the withdrawal of Federal Reserve support, Europe’s fragile recovery and China slowdown fears are combining to jeopardize one of the few remaining stock catalysts after a global rally of as much as 156 percent since 2009. And profit growth estimates are still too high for this year and 2017, says Bankhaus Lampe’s Ralf Zimmermann.

“The momentum in the global economy is slowing down to such an extent that people are seriously talking about recession,” said Zimmermann, a strategist at Bankhaus Lampe in Dusseldorf. “This is not just China, it’s far more widespread. There are few places to hide. Even defensives will feel the pain.”

Investors are running for the door -- they pulled about $12 billion from global stock funds last week, and the MSCI All-Country World Index is near its lowest level since August 2013.

Economists’ projections for worldwide expansion in 2016 have dropped steadily in the past months to just 3.3 percent, with estimates for China and the U.S. falling since the summer. The biggest bears are getting more bearish -- DoubleLine Capital’s Jeffrey Gundlach sees global growth slowing to just 1.9 percent in 2016, making it the worst year since the aftermath of the financial crisis in 2009.

This earnings season may not provide much reassurance, say strategists at JPMorgan Chase & Co. Analysts project a 6.7 percent contraction in fourth-quarter profits for Standard & Poor’s 500 Index members. For peers in Europe, estimates call for growth of just 2.7 percent for all of 2015, about half the pace predicted four months ago.

There are some pockets of optimism: lower energy prices may encourage consumers to spend more, Europe’s recovery has been exceeding expectations and the Fed has given itself the flexibility to delay further rate hikes. The earnings bar is so low that the scope for positive surprises is great, says ETF Securities’ James Butterfill.

“Fundamentals in the U.S. and Europe still look pretty good,” said Butterfill, head of research and investment in London. “Markets seem to be overly focused on the poor state of global manufacturing, and losing their view of the consumer. Confidence is rising, people have more money in their pockets, and company earnings should reflect that. Now is a good opportunity to buy because everyone is so bearish.”

For others, the outlook is gloomy. Europe’s resilient recovery is threatened by companies heavily reliant on American and Asian demand.

“Even without a recession, profit forecasts for the full year are too optimistic,” said Stewart Richardson, chief investment officer at RMG Wealth Management in London. “It’s not just a China problem, U.S. growth is slowing on its own right. It looks like Europe is not slowing, but give it six or 12 months and maybe it will be.”

COMMODITY CORNER - AGRI-COMPLEX

THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur

The most telling sign that we are heading into a real political economic shit storm is the fact that “TRUST” is collapsing on all sides. Obama is looking for any opportunity to disarm Americans. Why? This is simply because government is in trouble and they no longer “trust” the people. Likewise, the “rich” are starting to withdraw their money from investments that would create jobs because they are worried about the rising discontent among the majority of the population. Then we have the collapse in “trust” among anyone who is a career politician. So welcome to the theme of Davos — the collapse in “trust”.

NOTE: This is an absolute atrocious German translation - but the point is still clear!

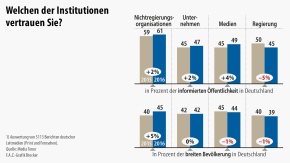

This news alarmed shortly before the start of the World Economic Forum in Davos deeply: In Germany, the confidence plunges into the actions of politicians in the light of the refugee crisis almost from. And all over the world mistrust of the general public to the better-educated and high-earning strata is widening. The elites no longer lead. Also, the information behavior of the corresponding groups falls further and further apart. The world gets an understanding problem.

For the "Trust Barometer" the global PR agency Edelman has more than 33,000 people surveyed in 28 countries around the world between October and November of last year. The result is clear: Confidence in the German politics has sunk in the informed population by 5 percentage points. A similar dynamic down there has otherwise given only in countries such as India, the United Arab Emirates and Poland. And events such as the conflict in the New Year's Eve in Cologne are not yet included in these figures because it took place only after the end of the survey period. It is obvious that they have yet led to significantly poorer than the measured values last fall.

Growing distrust of "those up there"

Here, the fundamental trust in governments, industry, NGOs and the media is to inform the world among those who have a higher education and belong to the intense upper 25 percent of the income pyramid, most recently even increased. These may have contributed especially the extremely good state of the economy in 2015, which in turn particularly applies to the situation in Germany. That confidence in this country yet so strong decline in the policy precisely in this group makes the German decline particularly remarkable - besides the fact that the Cabinet around ChancellorAngela Merkel (CDU) has cut above average in the polls of the past and in Compared to other governments had been regarded in the world as a guarantor of stability.

Around the world comes a phenomenon added, which should also be interested in the elites: In the vast majority believed "those up there" increasingly rare. Data that have been gathered from the media analysis company Media Tenor, confirm these impressions. The studies of Media Tenor and Edelman are the Frankfurter Allgemeine Zeitung before advance. In the data can be found not primarily an economy of inequality, as has been described by the French economist Thomas Piketty in his bestseller "The capital in the 21st century". What is reflected in the data, is an inequality of confidence around the world, which, however, often correlated with income inequality.

Trust inequality is reinforced by Trump, Le Pen & Co.

"It is a great illusion in the game, namely the idea that elites continue to lead and follow the masses," says the CEO Richard Edelman Edelman. And his boss Susanne Marell Germany-agrees. "Friends, family members and ordinary employees of an enterprise continues to be much more familiar than representatives of media, from companies or even politicians," says Marell.Greed, misbehavior, the democratization of the media, all that would mean that it was no longer so easy to gain the trust of the general population.

This inequality of trust has significant consequences. Quite obviously growing by the receptivity for politicians who want to make their prey to the fear of the population. As examples of this, both the refugee crisis and the bitter dispute over free trade agreements such as the targeted TTIP agreement between Europe and the United States can serve. Against TTIP go hundreds of thousands to the streets, the topic is emotionally heavy burden, especially the perceived or real lack of transparency in the negotiations bothers people. This is not altered, that democratically elected parliaments in each country of the agreement must agree in the end. Who benefits from this development?International fall Edelman to names of politicians such as Donald Trump or Marine Le Pen a.

Public confidence in elites decreases

In times of a new industrial revolution, which has the digitization of the entire value chain in the economic result, is added another worrisome finding. The skepticism about innovation is increasing in the general population. And the expectation of governments to regulate the market more, is diametrically opposed to the wishes of the economy, not to overdo it exactly in this point. The confidence barometer survey from Edelman message is perfectly clear on this point, however: The general population has become quite clearly too high, the pace of innovation. Here you want to see slow down the state and its representatives.

In more than 60 percent of the countries that were included by Edelman to the survey, the confidence of the masses in politics, business, NGOs and the media, however, is even fallen below a level of 50 percent. In marked contrast, the confidence of the elites has risen and is at the highest levels since the survey began. The average gap in confidence in the four institutions has grown between the elites and the general population to 12 percentage points. In the United States, the difference is 19 percentage points, suggesting the elites in the country on a huge disaffection the general population. In Germany, there are 9 points, here, however, on a constant level. Because the trust barometer also shows that each major differences with the income inequality in the countries concerned are related.

Discrepancy between elites and broad mass

Fittingly, in two-thirds of the countries surveyed, less than half the general population thinks it you better go than even five years ago. Also that is remarkable in view of a steady economic recovery: Is the observation match the reality, the profits made are disproportionately ended up in the hands of the higher-earning elite. This development is likely the debate about where the future flow automation dividends from the digitization of the economy, provide new food.

Hardly surprising, therefore, is that the biggest difference between the elite and the wider population is then also be seen in the attitude towards the economy and the company. While the confidence of elite has risen sharply in the economy, given the good economic in recent years, prevails in the crowd in front of deep skepticism. This skepticism is particularly high in certain sectors - and the financial services covered here still to strongly negative. There is a gap of more than 20 percentage points between the resurgent confidence of the elite in the industry and the general population.

The image of the greedy Bankers remains influential

The data that Media Tenor has collected through the analysis of the media coverage in the past year, confirm - and more: because the crisis of confidence is not confined to the financial sector. The diesel and emissions scandal at Volkswagen has led to resignations of once highly esteemed managers like the VW CEO Martin Winterkorn, will cost the shareholders of the Group's many billions of euros and has damaged not only the reputation of the automaker, but the entire German economy, as Susanne Marell Notes of Edelmann.

"But the public image of the banking sector deteriorated again," says Roland Schatz of Media Tenor - rights issues and the effectiveness of regulation stood still in the focus of media coverage. "Some banks were indeed able to convey a message of improvement, but the overall impression remains," says Schatz. So the new leadership of Deutsche Bank mediate among the Britons John Cryan currently although the feeling of a new beginning. But the overall impression is to act within remains of an industry that is dominated by the poorly educated, greedy managers. Account must be taken, however, that the German media tended compared to the United States or Great Britain to a particularly critical enterprise reporting. In fact, the image that has the general population from the banks, namely recently improved somewhat again as the trust barometer of Edelman shows has.

Tupperware shows how it works

For this survey, there is also that companies will always be given the chance to regain confidence quickly back. For confidence in the Chairman's basically risen again significantly - unlike the people involved in politics. The company will also have expected, the rapid transformation of the economy to cope better than politics, whose confidence levels are on the ground. 80 percent of the population at large expect companies to know both increase profits and contribute to improving the economic and social conditions in the communities in which they operate.

A good example of this is in the eyes of Edelman, the company Tupperware: Nearly 3.1 million women in countries such as China, India, Indonesia and South Africa make sales for the company - and bring much needed money home to their families. But the bosses, for example, Unilever or Starbucks would have made it through appropriate action in the past few months to improve the image of their business significantly in the public notices Susanne Marell from Edelman.

2016 Outlook – James Turk, Alasdair Macleod, John Butler;

Financial Repression Is Intensifying

Discussion on the year ahead .. negative interest rates potential for the U.S.$ – unintended consequences .. the risks of capital controls .. malinvestments from ZIRP & massive money printing .. the importance of investment in real assets as stores of value .. how financial repression is intensifying .. 48 minutes

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you confirm the facts on your own before making important investment commitments.

THE CONTENT OF ALL MATERIALS: SLIDE PRESENTATION AND THEIR ACCOMPANYING RECORDED AUDIO DISCUSSIONS, VIDEO PRESENTATIONS, NARRATED SLIDE PRESENTATIONS AND WEBZINES (hereinafter "The Media") ARE INTENDED FOR EDUCATIONAL PURPOSES ONLY.

The Media is not a solicitation to trade or invest, and any analysis is the opinion of the author and is not to be used or relied upon as investment advice. Trading and investing can involve substantial risk of loss. Past performance is no guarantee of future returns/results. Commentary is only the opinions of the authors and should not to be used for investment decisions. You must carefully examine the risks associated with investing of any sort and whether investment programs are suitable for you. You should never invest or consider investments without a complete set of disclosure documents, and should consider the risks prior to investing. The Media is not in any way a substitution for disclosure. Suitability of investing decisions rests solely with the investor. Your acknowledgement of this Disclosure and Terms of Use Statement is a condition of access to it. Furthermore, any investments you may make are your sole responsibility.

THERE IS RISK OF LOSS IN TRADING AND INVESTING OF ANY KIND. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Gordon emperically recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, he encourages you confirm the facts on your own before making important investment commitments.

DISCLOSURE STATEMENT

Information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities.

Please note that Mr. Long may already have invested or may from time to time invest in securities that are discussed or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him.

FAIR USE NOTICEThis site contains

copyrighted material the use of which has not always been specifically

authorized by the copyright owner. We are making such material available in

our efforts to advance understanding of environmental, political, human

rights, economic, democracy, scientific, and social justice issues, etc. We

believe this constitutes a 'fair use' of any such copyrighted material as

provided for in section 107 of the US Copyright Law. In accordance with

Title 17 U.S.C. Section 107, the material on this site is distributed

without profit to those who have expressed a prior interest in receiving the

included information for research and educational purposes.

If you wish to use

copyrighted material from this site for purposes of your own that go beyond

'fair use', you must obtain permission from the copyright owner.

{kind=link}