|

JOHN RUBINO'SLATEST BOOK |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

Thurs. Sept 10th, 2015

Follow Our Updates

onTWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

ANNUAL THESIS PAPERS

FREE (With Password)

THESIS 2010-Extended & Pretend

THESIS 2011-Currency Wars

THESIS 2012-Financial Repression

THESIS 2013-Statism

THESIS 2014-Globalization Trap

THESIS 2015-Fiduciary Failure

NEWS DEVELOPMENT UPDATES:

FINANCIAL REPRESSION

FIDUCIARY FAILURE

WHAT WE ARE RESEARCHING

2015 THEMES

SUB-PRIME ECONOMY

PENSION POVERITY

WAR ON CASH

ECHO BOOM

PRODUCTIVITY PARADOX

FLOWS - LIQUIDITY, CREDIT & DEBT

GLOBAL GOVERNANCE

- COMING NWO

WHAT WE ARE WATCHING

(A) Active, (C) Closed

MATA

Q3 '15- Chinese Market Crash

(A)

Q3 '15-

GMTP

Q3 '15- Greek Negotiations

(A)

Q3 '15- Puerto Rico Bond Default

MMC

OUR STRATEGIC INVESTMENT INSIGHTS (SII)

NEGATIVE-US RETAIL

NEGATIVE-ENERGY SECTOR

NEGATIVE-YEN

NEGATIVE-EURYEN

NEGATIVE-MONOLINES

POSITIVE-US DOLLAR

ARCHIVES

| AUGUST | ||||||

| S | M | T | W | T | F | S |

| 1 | 2 | 3 | 4 | 5 | ||

| 6 | 7 | 8 | 9 | 10 | 11 | 12 |

| 13 | 14 | 15 | 16 | 17 | 18 | 19 |

| 20 | 21 | 22 | 23 | 24 | 25 | 26 |

| 27 | 28 | 29 | 30 | |||

KEY TO TIPPING POINTS |

| 1- Bond Bubble |

| 2 - Risk Reversal |

| 3 - Geo-Political Event |

| 4 - China Hard Landing |

| 5 - Japan Debt Deflation Spiral |

| 6- EU Banking Crisis |

| 7- Sovereign Debt Crisis |

| 8 - Shrinking Revenue Growth Rate |

| 9 - Chronic Unemployment |

| 10 - US Stock Market Valuations |

| 11 - Global Governance Failure |

| 12 - Chronic Global Fiscal ImBalances |

| 13 - Growing Social Unrest |

| 14 - Residential Real Estate - Phase II |

| 15 - Commercial Real Estate |

| 16 - Credit Contraction II |

| 17- State & Local Government |

| 18 - Slowing Retail & Consumer Sales |

| 19 - US Reserve Currency |

| 20 - US Dollar Weakness |

| 21 - Financial Crisis Programs Expiration |

| 22 - US Banking Crisis II |

| 23 - China - Japan Regional Conflict |

| 24 - Corruption |

| 25 - Public Sentiment & Confidence |

| 26 - Food Price Pressures |

| 27 - Global Output Gap |

| 28 - Pension - Entitlement Crisis |

| 29 - Central & Eastern Europe |

| 30 - Terrorist Event |

| 31 - Pandemic / Epidemic | 32 - Rising Inflation Pressures & Interest Pressures |

| 33 - Resource Shortage |

| 34 - Cyber Attack or Complexity Failure |

| 35 - Corporate Bankruptcies |

| 36 - Iran Nuclear Threat |

| 37- Finance & Insurance Balance Sheet Write-Offs |

| 38- Government Backstop Insurance |

| 39 - Oil Price Pressures |

| 40 - Natural Physical Disaster |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

Charles Hugh Smith's Latest Books

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

OTHERS OF NOTE

Book Review- Five Thumbs Up

for Steve Greenhut's Plunder!

![]()

TODAY'S TIPPING POINTS

|

Have your own site? Offer free content to your visitors with TRIGGER$ Public Edition!

Sell TRIGGER$ from your site and grow a monthly recurring income!

Contact [email protected] for more information - (free ad space for participating affiliates).

HOTTEST TIPPING POINTS |

Theme Groupings |

||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro

|

|||

|

MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | 09-10-15 | ||

The End Of The Fed's "Interest Rate Magic Show" LoomsSubmitted by Aswath Damodoran via Musings On Markets, The Fed, Interest Rates and Stock Prices: Fighting the Fear FactorIf it feels like you are reading last year’s business stories in today's paper, there is a simple reason. The Federal Reserve's Open Markets Committee (FOMC) meeting date is approaching, and in a replay of what we have seen ahead of previous meetings, we are being told that this is the one where the Fed will lower the boom on stock markets, by raising interest rates. While this navel gazing may keep market oracles, Fed watchers and CNBC pundits occupied, I think that the Fed’s role in setting interest rates is vastly overstated, and that this fiction is maintained because it is convenient both for the Fed and for the rest of us. I think that there are multiple myths about the Fed’s powers that have taken hold of our collective consciousness, and led us into an investing netherworld. So at the risk of provoking the wrath of Fed watchers everywhere, and repeating what I have said in earlier posts, here are my top four myths about central banks.

1. The Fed sets interest rates Myth: The Federal Reserve (or the Central Bank of whichever country you are in) sets interest rates, short term as well as long term. In my last post on this topic, I mentioned my tour of the Federal Reserve Building, with my wife and children, and how sorely tempted I was to ask the tour guide whether I could see the interest rate room, the one where Janet Yellen sits, with levers that she can move up or down to change our mortgage rates, the rate at which companies borrow from banks and the market and the rates on US treasuries.

Reality: There is only one rate that the Federal Reserve sets, and it is the Fed Funds rate. It is the rate at which banks trade funds, that they hold at the Federal Reserve, with each other. Needless to say, not only is this an overnight rate, but it is of little relevance to most of us who don't have access to the Fed windows. While there is a tenuous link of Fed Funds rate to short term market interest rates, that link becomes much weaker when we look at long term rates and their derivatives.

Why preserve the myth: Giving the Fed the power to set interest rates gives us all a false sense of control over our economic destinies. Thus, if rates are high, we assume that the Fed can lower them by edict and if rates are too low, it can raise it by dictate. If only..

2. Low interest rates are the Fed’s doing

Myth: Interest rates are at historic lows not just in the United States but in much of the developed world, and it is central banking policy that has kept them there, through a policy of quantitative easing The myth acquires additional sheen when accompanied by acronyms such as QE1 and QE2, which bring ocean liners to my mind and a nagging fear that the next Fed move will be titled the Titanic!

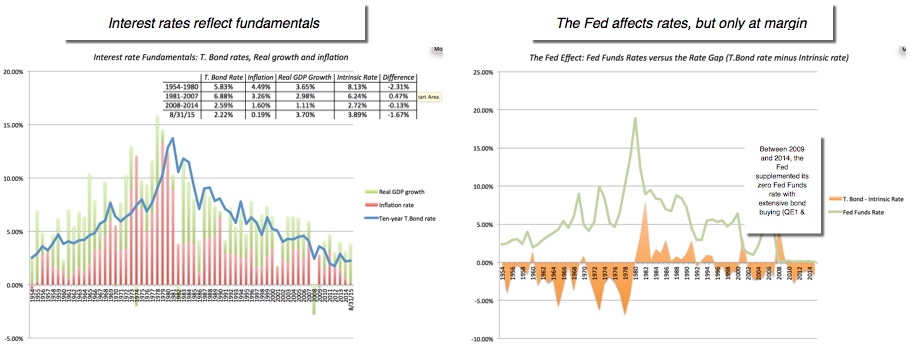

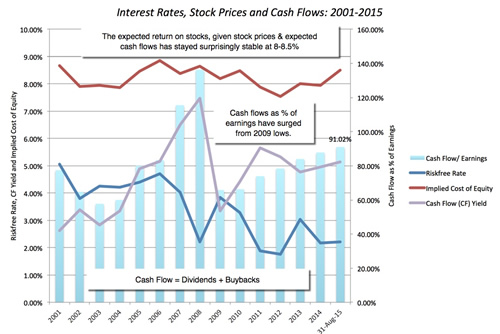

Reality: The Fed has had a bond-buying program that is unprecedented and large, but only relative to the Fed's own history. Relative to the size of the US treasury bond market (about $500 billion a day in 2014), the Fed bond-buying (about $60-$85 billion a month) is modest and unlikely to have the influence on interest rates that is attributed to it. So, what has kept rates low? At the risk of rehashing a graph that I have used multiple times, it is far simpler and more fundamental, and it lies in the Fisher equation, which decomposes the nominal interest rate into its expected inflation and real interest rate components:

Nominal Interest Rate = Expected Inflation + Expected Real Interest Rate

If you make the assumption that in the long term, the real interest rate in an economy converges on real growth rate, you have an equation for what I call an intrinsic risk free rate. In the graph below, I graph out the actual US 10-year treasury bond rate against this intrinsic risk free rate and you can make your own judgment on why rates have been low for the last five years.'

To me, the answer seems self evident. Interest rates in the US (and Europe) have been low because inflation has been non-existent and real growth has been anemic, and it is my guess that rates would have been low, with or without the Fed’s exertions. In fact, the cumulative effect of the Fed's exertions can be measured as the difference between the intrinsic risk free rate and the US treasury bond rate, and during the entire quantitative easing period of 2008-2014, it amounted to about 0.13%. It is true that the jump in US GDP in the most recent quarter has widened the difference between the treasury bond rate and the intrinsic interest rate, but it remains to be seen whether this increase is a precursor to more healthy growth in the future, or just an one-quarter aberration. Why preserve the myth: I think it is much more comforting for developed market investors to think of low interest rates as an unmitigated good, pushing up stock and bond prices, rather than as a depressing signal of future growth and low inflation (perhaps even deflation) in much of the developed world. That problem will not be fixed by Fed meetings and is symptomatic of shifts in global economic power and a re-apportioning of the world economic pie. 3. The reason stock prices are so high is because rates are low

Myth: Stock prices are high today because interest rates are at historic lows. If interest rates revert back to normal levels, stock prices will collapse.

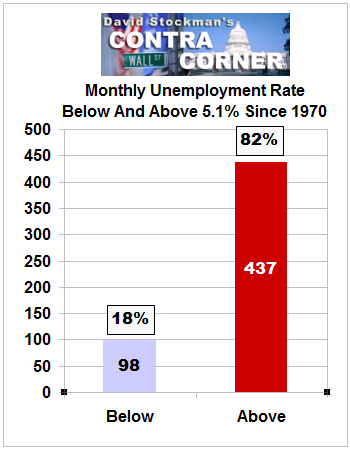

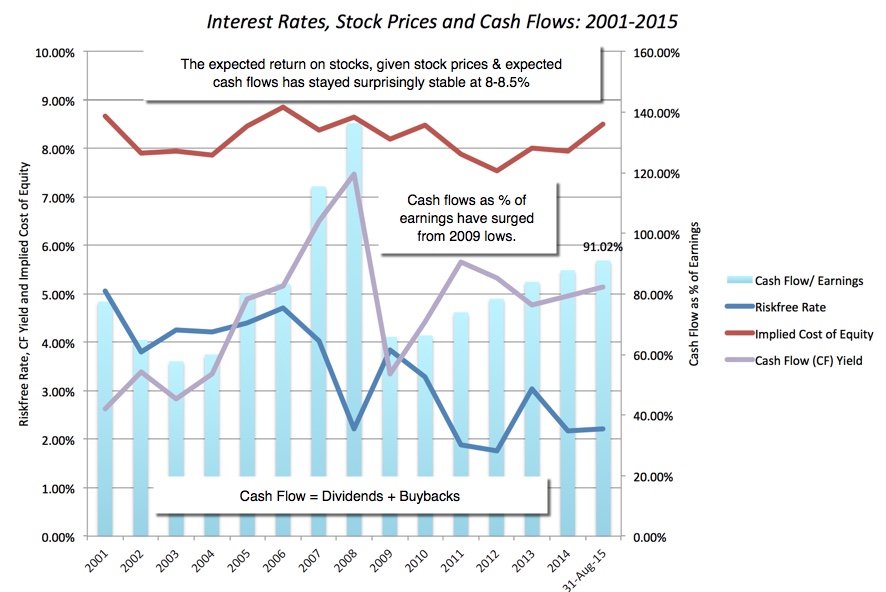

Reality: Low interest rates have been a mixed blessing for stocks. The low rates, by themselves, make stocks more attractive relative to the alternative of investing in bonds. But if the low rates are symptomatic of low inflation and low real growth, they do have effects on the cash flows that can partially or completely offset the effect of low rates. One way to decompose the effects is to compute forward-looking expected returns on stocks, given stock prices today and expected cash flows from dividends and buybacks in the future to see how much of the stock price effect is fueled by interest rates and how much by cash flow changes. If this bull market has been entirely or mostly driven by the drop in interest rates, the expected return on stocks should have declined in line with the drop in interest rates. In my most recent update on this number at close of trading on August 31, 2015, I estimated an expected return of 8.50%, almost unchanged from the level in 2009 and higher than the expected return in 2007.

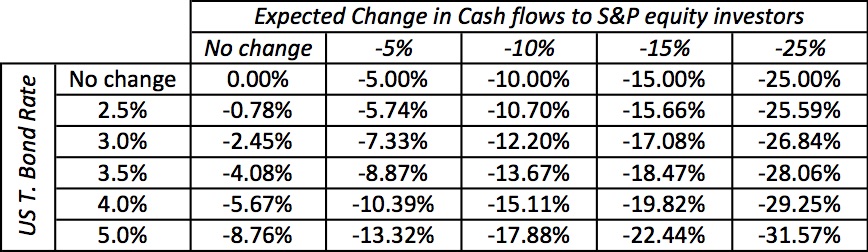

At least based on my estimates, the primary driver of stock prices has been the extraordinary fountain of cash that companies have been able to return in the last few years, combined with a capacity to grow earnings over the same period. By the same token, if you are concerned about cash flows, it should be with the sustainability of these cash flows, for two reasons. The first is that earnings will be under pressure, given the strength of the dollar and the weakness in China, and this is starting to show up already, with 2015 earnings about 5-10% below 2014 levels. The second is that companies will not be able to keep returning as much as they are in cash flows; in 2015, the cash returned to stockholders stood at 91% of earnings, a number well above historic norms. In the table below, I check to see how much the index, which was at 1951.13 at the close of trading on September 3, would be affected by an increase in interest rates (increasing the US 10-year T.Bond rate from the 2.27% on September 3, to 5%) as contrasted with a drop in cash flows (with a maximum drop of 25%, coming from a combination of earnings decline and reduced cash payout): If you hold cash flows constant, an increase in interest rates has a relatively small effect on stock prices, with stock prices dropping 8.76%, even if the US T.Bond rate rises to 5%. In contrast, if cash flows drop, the index drops proportionately, even if interest rates remain unchanged. You are welcome to make your own "bad news" assumptions and check out the effect on value in this spreadsheet.

Why preserve the myth: For perpetual bears, wrong time and again in the last five years about stocks, the Fed (and low interest rates) have become a convenient bogeyman for why their market bets have gone wrong. If only the Fed had behaved sensibly and if only interest rates were at normal levels (though normal is theirs to define), they bemoan, their market timing forecasts would have been vindicated.

4. The biggest danger to the Fed is that the market will react violently to a change in its interest rate policy

Myth: The biggest danger to the Fed is that, if it reverses its policy of zero interest rates and stops its bond buying, stock and bond markets will drop dramatically.

Reality: While no central bank wants to be blamed for a market meltdown, the bigger danger, in my view, is that the Fed does what it has been promising to for so long, and nothing happens. That is a good thing, you might say, and while I agree with you in the short term, the long-term consequences for Fed credibility are damaging and here is why. The best analogy that I can offer for the Fed and its role on interest rates is the story of Chanticleer, a rooster that is the strutting master of the barnyard that he lives in, revered by the other farm animals because he is the one who causes the sun to rise every morning with his crowing (or so they think). In the story, Chanticleer’s hubris leads him to abandon his post one morning, and when the sun comes up anyway, the rooster loses his exalted standing. Given the build up we have had over the last few years to the momentous decision to change interest rate policy, think of how much our perceptions of Fed power will change, if stock and bond markets respond with yawns to an interest rate policy shift.

Why we hold on to the myth: If you buy into the first three myths, this one follows. After all, if you believe that the Fed sets interest rates, that it has deliberately kept interest rates low for the last five years and that stock prices are high because interest rates are low, you should fear a change in that policy. Coupled with China, you have the excuses for your underperformance this year, thus absolving yourself of all responsibility for your choices. How convenient?

What next? I don't know what will happen at the FOMC meeting, but I hope that it announces an end to it's "interest rate magic show". I think that there is enough pent up fear in markets that the initial reaction will be negative, but I am hoping that investors move on to healthier, and more real, concerns about economic growth and earnings sustainability. If the Fed does make its move, the best news will be that we will not have to go through more rounds of obsessive Fed watching, second-guessing and punditry. |

|||

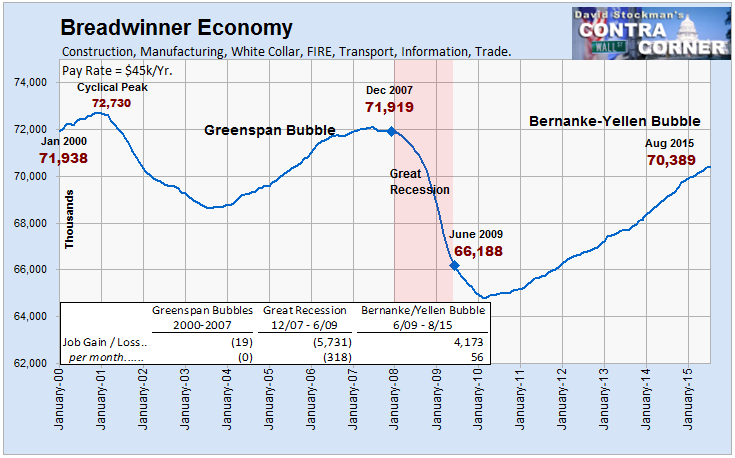

The Endless Emergency - Why It's Always ZIRP Time In The CasinoSubmitted by David Stockman via Contra Corner blog, Based on the headline from the latest Jobs Friday report you wouldn’t know that we are still mired in an economic emergency - one apparently so extreme that it might entail moving to the 81st straight month of zero interest rates at next week’s FOMC meeting. After all, the unemployment rate came in smack-dab on the Fed’s full-employment target at 5.1%. But that’s not the half of it. The August unemployment rate was also in the lowest quintile of modern history. That’s right. There have been 535 monthly jobs reports since 1970, yet in only 98 months or 18% of the time did the unemployment rate post at 5.1% or lower.  Monthly Unemployment Rate Below And Above 5.1% Since 1970 In a word, the official unemployment rate is now in what has been the macroeconomic end zone for the past 45 years. Might this suggest that the emergency is over and done? Not at all. The talking heads have been out in force insisting on yet another deferral of “lift-off” on the grounds that the economy is allegedly still fragile and that the establishment survey number at 173,000 jobs came in on the light side. Even the so-called centrists on the Fed—–Stanley Fischer and John Williams—–have gone to full-bore, open-mouth, two-armed economist mode, jabbering incoherently while they await more “in-coming” economic data. Self-evidently, the only “incoming” information that can matter between now and next Wednesday is the stock market averages. To wit, if last October’s Bullard Rip low on the S&P 500 holds at 1867, the FOMC will declare “one and done”, at least for the year; and if the market succumbs to another spot of vertigo, the Fed will concoct yet another lame excuse for delay. Indeed, the Fed’s true Humphrey-Hawkins target is transparent. Namely, avoidance of a “risk-off” hissy fit at all hazards. So let’s just call the whole thing a cosmic farce and dispense with the macroeconomic hair-splitting. Ordinary people everywhere on the planet are in grave danger because governments and their central banking branches have put the gamblers in charge of the economic show. That’s self-evident in Europe where the Brussels/Frankfurt apparatchiks are deathly afraid of a stampede toward the exits by the front-running gamblers who “rented” (on repo) the sovereign bond market on Draghi’s “whatever it takes” ukase. So they have now turned Greece into an outright debtors’ prison, extinguishing the last remnants of democratic self-rule and imposing debt obligations that will approach $500 billion when Greece’s new bailout and existing massive ECB debits are reckoned. Greece’s battered and still shrinking $200 billion economy, therefore, will either become an economic Atlantis lost under the Aegean or an exploding debt bomb. That is, when Greece finally defaults, it will trigger the demise of the Euro, the European Project and the continent’s rickety banking system——-stuffed to the gills, as it is, with the unpayable debts of aging, sclerotic socialist economies. Likewise, the lunatic twosome of Abe and Kuroda in Japan have succeeded in putting the Japanese economy back into recession—-even as they run the greatest sovereign buyback Ponzi in history. To wit, the BOJ is buying up Japan’s stupendous one quadrillion yen of public debt faster than new debt is being created, thereby pegging the 10-year JGB at a ridiculous 36 basis point yield and flushing Japan’s domestic investors into a rampaging stock bubble that is an accident waiting to happen. In the nearby land of red capitalism the statist fix gets more preposterous by the day. Having sent out Brink’s trucks loaded with $300 billion to buy unwanted stocks and a fleet of paddy wagons to arrest anyone even a tad too eager to sell, China’s chief money printer told the G-20 on Saturday that China’s $5 trillion stock market meltdown was over. But when the Shanghai market opened nearly 2% down last night, the “national team” went berserk hitting the “offers” in a desperate effort to prove him right. On a dime, the red casino suddenly ripped to 3% higher by the market’s close. So the suzerains of red capitalism now depend on a blunderbuss PPT (Plunge Protection Team) to keep the grim reaper at bay. With more retail stock account holders (90 million) than communist party members (80 million) and more separate trading accounts (287 million) than the combined population of Japan, South Korea, Taiwan and Thailand (267 million), a supreme irony has come to pass. Namely, that Beijing’s heirs of Mao’s anti-capitalist revolution have no choice except to prop-up the stock market in order to obfuscate the deflationary whirlwind battering Mr. Deng’s hothouse economy. Even then, the giant Red Elephant in the room is hard to hide. That’s why capital is in full flight, as underscored by last night’s disclosure that China’s vaunted FX reserves dropped by $94 billion in August alone—-notwithstanding a huge current account surplus. That’s also why China’s imports plunged by 14% and exports by nearly 6% last month, and why car sales have dropped sharply again in August. Indeed, flat-lining industrial production, power consumption and freight shipments all show an economy floundering at stall speed or worse. At least the rulers in Beijing make no bones about the fact that they are rigging the stock index. After all, “command and control” is what the communist party does. Not so for the hypocritical posse of cowards, dissemblers and Keynesian dogmatists who run the Fed. These folks presumably have a passing regard for the rudiments of capitalism and free markets. Yet they insist that the most important market in all of capitalism—–the money market where traders and speculators fund trillions of positions and inventories—-is no market at all; and that, instead, it’s an administrative department of the central bank to be governed by the writ of 12 FOMC members based on their subjective assessment of the “incoming” macroeconomic noise. Stated differently, the Fed has extinguished any and all market prices for money, and indeed any price at all; and in the process has caused the falsification of debt and equity prices throughout the capital markets. So Wall Street and its equivalents around the world have become little more than casinos where the gamblers trade against the croupiers domiciled in the major central banks. But heavens forfend that our monetary central planners should admit to the unseemly bended knee estate to which they have been reduced. So in what amounts to mindless ritual incantation they persist in gumming about what is self-evidently seasonally maladjusted, constantly revised, inherently incomplete noise. At the end of the day that’s the frail reed on which the whole contemporary central banking enterprise is based. The truth is, central banks emit credits conjured from thin air into a borderless planetary financial system that is now populated by the demons and furies of bubble finance. These free money enabled gamblers and speculators never stop confecting new forms of carry trades, collateralized finance and momentum chasing algorithms that rip the casino loose from the real economy. Moreover, all the central bank interest rate pegging at zero is beside the point insofar as the real economy is concerned. That’s because over the last two decades the central banks have fueled a debt binge of staggering proportions. Overall credit market debt has grown from $40 trillion in 1995 to $200 trillion last year. That $160 trillion credit expansion was nearly 4X the modest global GDP growth of $45 trillion during the same period. Accordingly, the world has simultaneously reached a condition of “peak debt” in the DM world, where 90% of households are tapped out or on welfare; and “peak capacity” in the EM world, where a digging, building and investment spree has left economies drowning in excess industrial capacity and white elephant public infrastructure. In that context, the only thing that zero interest rates can do is fuel a few more spasms of “risk-on” rips in the casino; and supply a drip of cheap capital to DM companies wishing to buy back their own stock, and a temporary lifeline to EM and commodity sector zombies hemorrhaging cash. But what it can’t do is anything to deliver the so-called Humphrey-Hawkins target of maximum employment; or the goal of price stability as per the Fed’s perverse definition of it as 2% on the PCE deflator—— less food and energy or whatever else the monetary politburo chooses to delete from the figure. The measured inflation rate, of course, is now being powerfully suppressed by the very global deflation flowing from peak DM debt and peak EM capacity that the central bank money printers have generated over the last two decades. Beyond that, there is not a shred of valid evidence from economic history or logic that says you get more sustainable growth in living standards from 2% consumer inflation than from 0%. But at the end of the day all of the Fed’s jawing in support of ZIRP is rooted in an utterly obsolete model of bathtub economics in one nation. That is, the notion that central bank credit is injected into a closed domestic economy, not a wide-open global casino, and that these injections will eventually cause an invisible economic ether called “aggregate demand” to rise to the brim of full employment. Since the year 2000 the Fed has emitted $4 trillion of central bank credit. But as the Friday Jobs report actually showed, 5.1% on the official unemployment rate has had nothing to do with filling the US economic bathtub to its purported full employment potential. As shown below, notwithstanding hitting the 5% unemployment target three times since the late 1990s, the real measures of labor inputs employed by the US economy have gone steadily south. The civilian employment-population ratio is down by five full percentage points or 12.5 million workers, and total nonfarm labor hours deployed by the business economy have not broken the flat-line in 15 years. Even more to the point, the number of breadwinner jobs paying a fulltime living wage was still nearly two million below its turn of the century level in Friday’s report.  Breadwinner Economy Jobs Needless to say, Friday’s report perfectly underscores why basing Fed policy on “incoming data” like the BLS employment report is so copasetic to the casino. If the Fed take no action after the September release, it’s hard to imagine a report that wouldn’t support ZIRP or near-ZIRP in the minds of the money printers and the Wall Street gamblers they pleasure. |

|||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK -Sept 6th, 2015 - Sept. 12th, 2015 | |||

| BOND BUBBLE | 1 | ||

| RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates | 2 | ||

| GEO-POLITICAL EVENT | 3 | ||

| CHINA BUBBLE | 4 | ||

| JAPAN - DEBT DEFLATION | 5 | ||

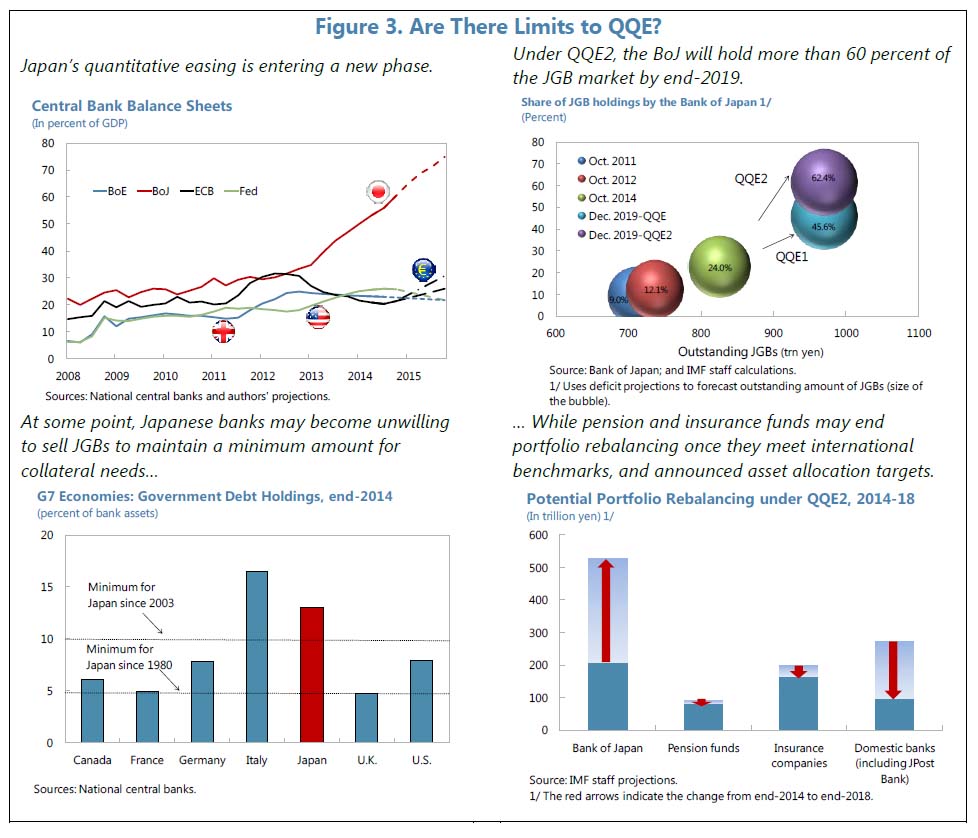

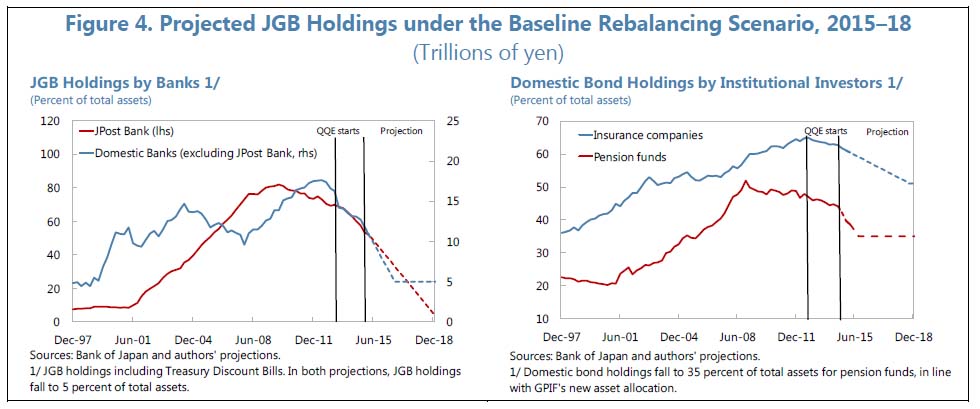

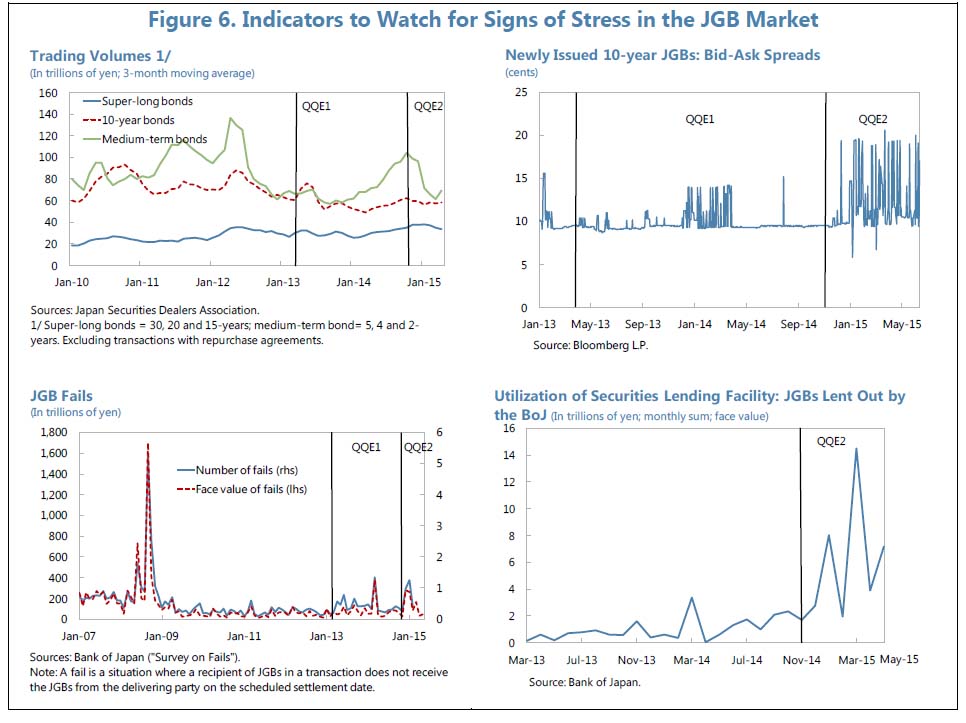

JAPAN - DEBT DEFLATION The IMF Just Confirmed The Nightmare Scenario For Central Banks Is Now In PlaySubmitted by Tyler Durden on 09/06/2015 - 19:59

The centrally-planned house of cards is finally starting to shake uncontrollably.

|

09-08-15 | JAPAN | 5 - Japan Debt Deflation Spiral |

The IMF Just Confirmed The Nightmare Scenario For Central Banks Is Now In PlayThe most important piece of news announced today was also, as usually happens, the most underreported: it had nothing to do with US jobs, with the Fed's hiking intentions, with China, or even the ongoing "1998-style" carnage in emerging markets. Instead, it was the admission by ECB governing council member Ewald Nowotny that what we said about the ECB hitting a supply brick wall, was right. Specifically, earlier today Bloomberg quoted the Austrian central banker that the ECB asset-backed securities purchasing program "hasn’t been as successful as we’d hoped." Why? "It’s simply because they are running out. There are simply too few of these structured products out there." So six months later, the ECB begrudgingly admitted what we said in March 2015, in "A Complete Preview Of Q€ — And Why It Will Fail", was correct. Namely this:

(Actually, we said all of the above first all the way back in 2012, but that's irrelevant.) So aside from the ECB officially admitting that it has become supply*constrained even with security prices at near all time highs, why is this so critical? Readers will recall that just yesterday we explained why "Suddenly The Bank Of Japan Has An Unexpected Problem On Its Hands" in which we quoted BofA a rates strategist who said that "now that GPIF’s selling has finished, the focus will be on who else is going to sell. Unless Japan Post Bank sells JGBs, the BOJ won’t be able to continue its monetary stimulus operations." We also said this:

Once again to be accurate, the first time we warned about the biggest nightmare on deck for the BOJ (and ECB, and Fed, and every other monetizing central bank) was back in October 2014, when we cautioned that the biggest rish was a lack of monetizable supply. We cited Takuji Okubo, chief economist at Japan Macro Advisors in Tokyo, who said that at the scale of its current debt monetization, the BOJ could end up owning half of the JGB market by as early as in 2018. He added that "The BOJ is basically declaring that Japan will need to fix its long-term problems by 2018, or risk becoming a failed nation."

This was our summary:

That said, our conclusion, which was not to "expect the media to grasp the profound implications of this analysis not only for the BOJ but for all other central banks: we expect this to be summer of 2016's business" may have been a tad premature. The reason: overnight the IMF released a working paper written by Serkan Arslanalp and Dennis Botman (which was originally authored in August), which confirmed everything we said yesterday... and then some. Here is Bloomberg's summary of the paper:

Here are the excerpts from the paper:

Back to Bloomberg:

Who in turn merely joined Zero Hedge who warned about precisely this in October of last year. Back to the IMF paper, which notes that in Japan, where there is a limited securitization market, the only "high quality collateral" assets are JGBs, and as a result of the large scale JGB purchases by the JGB, "a supply-demand imbalance can emerge, which could limit the central bank’s ability to achieve its monetary base targets.Such limits may already be reflected in exceptionally low (and sometimes negative) yields on JGBs, amid a large negative term premium, and signs of reduced JGB market liquidity."

For those surprised by the IMF's stark warning and curious how it is possible that the BOJ could have put itself in such a position, here is the explanation:

As we expanded yesterday, the biggest issue for the BOJ is not that it has problems buying paper, but that there are simply not enough sellers: "under QQE1, only around 5 percent of BoJ’s net JGB purchases from the market came from institutional investors. In contrast, under QQE2, close to 40 percent of net purchases have come from institutional investors between October 2014 and March 2015."

This is where things get back for the BOJ, because now that the BOJ is buying everything official institutions have to sell, the countdown has begun:

Then there are the liquidity issues:

This, too, is precisely what we warned yesterday would be the outcome: "the BOJ will not boost QE, and if anything will have no choice but to start tapering it down - just like the Fed did when its interventions created the current illiquidity in the US govt market - especially since liquidity in the Japanese government market is now non-existant and getting worse by the day." The IMF paper conveniently provides some useful trackers to observe just how bad JGB liquidity is in real-time.

The IMF is quick to note that the BOJ does have a way out: it can simply shift its monetization to longer-dated paper, expand collateral availability using tthe BOJ's Securited Lending Facility (which basically is a circular check kiting scheme, where the BOJ lends banks the securities it will then repurchase from them), or simply shift from bonds to other assets: "the authorities could expand the purchase of private assets. At the moment, Japan has a relatively limited corporate bond market (text chart). Hence, this would require jumpstarting the securitization market for mortgages and bank loans to small and medium-sized enterprises which could generate more private assets for BoJ purchases." But the biggest risk is not what else the BOJ could monetize - surely the Japanese government can always create "monetizable" kitchen sinks... but what happens when the regime shifts from the current buying phase to its inverse:

When considering that by 2018 the BOJ market will have become the world's most illiquid (as the BOJ will hold 60% or more of all issues), the IMF's final warning is that "such a change in market conditions could trigger the potential for abrupt jumps in yields." At that moment the BOJ will finally lose control. In other words, the long-overdue Kyle Bass scenario will finally take place in about 2-3 years, tops. But ignoring the endgame for Japan, and recall that BofA triangulated just this when it said that "the BOJ is basically declaring that Japan will need to fix its long-term problems by 2018, or risk becoming a failed nation", what's worse for Abe is that the countdown until his program loses all credibility has begun. What happens then? As BNP wrote in an August 28-dated report, "Once foreign investors lose faith in Abenomics, foreign outflows are likely to trigger a Japanese equities meltdown similar to the one observed during 2007-09." And from there, the contagion will spread to the entire world, whose central banks incidentally, will be faced with precisely the same question: who will be responsible for the next round of monetization and desperately kicking the can one more time. But before we get to the QE endgame, we first need to get the interim point: the one where first the markets and then the media realizes that the BOJ - the one central banks whose bank monetization is keeping the world's asset levels afloat now that the ECB has admitted it is having "problems" finding sellers - will have no choice but to taper, with all the associated downstream effects on domestic and global asset prices. It's all downhill from there, and not just for Japan but all other "safe collateral" monetizing central banks, which explains the real reason the Fed is in a rush to hike: so it can at least engage in some more QE when every other central bank fails. But there's no rush: remember to give the market and the media the usual 6-9 month head start to grasp the significance of all of the above. Source: IMF

|

|||

EU BANKING CRISIS |

6 |

||

| TO TOP | |||

| MACRO News Items of Importance - This Week | |||

GLOBAL MACRO REPORTS & ANALYSIS |

|||

US ECONOMIC REPORTS & ANALYSIS |

|||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | |||

Submitted by Tyler Durden on 09/09/2015 Buiter: Only "Helicopter Money" Can Save The World From The Next Recession

That rather hilarious characterization of the pseudoscience that is economics comes from the desk of Citi’s Chief Economist Willem Buiter and it’s apparently evidence that even if you don’t think too much of his views on “pet rocks” (gold is a 6,000 year-old bubble) or on the efficacy and/or utility of physical banknotes (ban cash), you’d be hard pressed to disagree with him when it comes to critiquing his profession. Of course we don’t want to give Buiter too much credit here because the quote shown above could simply be an attempt to stamp a caveat emptor on his latest prediction in case, like his predictions on when Greece would ultimately leave the euro, it turns out to be wrong. As tipped by comments made at the Council of Foreign Relations in New York late last month, Buiter is out with a damning look at the global economy which he says will be drug kicking and screaming into a recession by the turmoil in China and the unfolding chaos in EM. Here’s the call:

More specifically, Buiter says the odds of some kind of recession (either mild or terrifying) are 55%. Not 54%, or 56% mind you, but exactly 55%, because as indicated by the introductory excerpt above, economic outcomes are very amenable to precise forecasting:

The culprit, as mentioned above, is China (where Citi says real GDP growth is actually somewhere in the neighborhood of 4%) and EMs more broadly which are suffering mightily in the face of sluggish Chinese demand, slumping commodity prices, and, most recently, the devaluation of the yuan:

Evidence of weakness, Buiter continues, is everywhere:

And China - the epicenter of it all - is ill-equipped to cope because, as we’ve discussed at length, the country’s many spinning plates have elicited an eye-watering array of conflicting directives and policies which are now tripping over each other at nearly every turn:

Finally, DM central planners are in no shape to combat the China/EM contagion because - and this will come as no surprise - they are simply out of ammunition having thrown everything in the Keynesian toolbox at their respective economies in the post-crisis years with limited (and swiftly diminishing) returns:

As you might have guessed, Buiter thinks there’s only one way out of this: helicopter money. And not just in the US, but in Europe (against the protestations of what Buiter calls the “Teutonic fringe”) and indeed across all DMs and also in China.

So basically, these central banks which Buiter just admitted are already “operating in the zone of severely diminishing returns,” should not only do more of the same, but a lot more of the same and in fact, they should all dive head first into the Keynesian abyss by simultaneously cranking the knob on their respective printing presses to the max:

There you have it. "QE#N where N could become a large integer", and paradoxically, by not normalizing policy when it had the chance, the Fed has now made this inevitable because as we've shown, tightening into an EM FX reserve drawdown will only exacerbate said drawdown making an embarrassing about-face by the FOMC a foregone conclusion. In other words, this is game over. We've entered the monetary Twilight Zone where the only way to keep the increasingly wobbly house of cards standing is to continue to monetize everything that's monetizable and when we hit the limit we must then move to issue more debt for the sole purpose of monetizing it and immediately canceling it. But as Buiter noted at the outset, these are all just the musings of a pseudo-scientist, who, by the very nature of his profession, is prone to making predictions that, much like the Fed's "liftoff", are just as likely to "explode in mid-air" as not.

|

|||

| Market | |||

| TECHNICALS & MARKET |

|

||

| COMMODITY CORNER - AGRI-COMPLEX | PORTFOLIO | ||

| SECURITY-SURVEILANCE COMPLEX | PORTFOLIO | ||

| THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur | |||

| 2015 - FIDUCIARY FAILURE | 2015 | THESIS 2015 |  |

| 2014 - GLOBALIZATION TRAP | 2014 |  |

|

|

|||

|

2013 2014 |

|

||

FINANCIAL REPRESSION - War on Cash Life In A Cashless World: How Cash Became A Policy Tool – An Interview With Dr. Harald MalmgrenSubmitted by Tyler Durden on 09/06/2015 - 08:45

Banks in the US and Europe are trying to develop a cashless transactions system. The concept is to establish a comprehensive ledger for a business or a person that records everything received and spent, and all of the assets held – mortgages, investment portfolios, debts, contractual financial obligations, and anything else of market value. There would be no need for cash because the ledger would tell you and anyone you were considering a transaction with how much is available and would be transactable at any specific moment. This is not a dreamy idea. Blythe Masters is leading a new business effort to develop a universal cashless system. Not only is she gathering significant investor interest, but the Federal Reserve and various US Government agencies have become keenly interested in the potential usefulness and efficiencies of a universal cashless system The Case For Outlawing CashSubmitted by Tyler Durden on 09/06/2015 - 14:15

September is here. As expected, market volatility is increasing. The Great Zombie War is intensifying. And investors are getting scared. Now they even want to do away with the State’s own scrip... You see where this is going, don’t you? If the feds are able to ban cash, they will have you completely under their control. You will invest when they want you to invest. You will buy when and what they want you to buy. You will be forced to keep your money in a bank – a bank controlled, of course, by the feds. The Danger Of Eliminating CashSubmitted by Tyler Durden on 09/07/2015 - 18:10

In the early days of central banking, one primary objective of the new system was to take ownership of the public's gold, so that in a crisis the public would be unable to withdraw it. Gold was to be replaced by fiat cash which could be issued by the central bank at will. This removed from the public the power to bring a bank down by withdrawing their property. A primary, if unspoken, objective of modern central banking is to do the same with fiat cash itself.

|

09-07-15 | ||

Submitted by Erico Matias Tavares of Sinclair & Co. Life In A Cashless World: How Cash Became A Policy Tool – An Interview With Dr. Harald MalmgrenCash as a Policy Tool – An Interview with Dr. Harald Malmgren The Hon. Dr. Harald Malmgren, Chief Executive of Malmgren Global, advises governments and companies on international trade and investment. A former senior aide to US Presidents John F. Kennedy, Lyndon B. Johnson, Richard Nixon and Gerald Ford and to Senators Abraham Ribicoff and Russell Long, US Senate Committee on Finance, he is a frequent author of articles and papers on global economic, political and security affairs. E. Tavares: Prof. Malmgren, it is a pleasure and a privilege to be speaking with you today. We would like to talk about cash – the actual bills and coins – as a policy tool, something which is not often discussed. Before we get into that, what are the main developments you are seeing in the transactional space around the world? H. Malmgren: Banks in the US and Europe are trying to develop a cashless transactions system. The concept is to establish a comprehensive ledger for a business or a person that records everything received and spent, and all of the assets held – mortgages, investment portfolios, debts, contractual financial obligations, and anything else of market value including pleasure boats, automobiles, and other machinery. There would be no need for cash because the ledger would tell you and anyone you were considering a transaction with how much is available and would be transactable at any specific moment. Any purchase, past or recent could be found and details provided whenever such information was sought. Governments would very much like such ledgers to exist because they could view everything that is taking place financially in real time, including ability to evaluate net worth, patterns of spending and of earned and unearned income, and of course, an instant assessment of all taxable activities. Governments would be able to gauge overall economic activity in real time, no longer needing to wait for months the collection of revenues and sales of businesses and surveys of consumer spending. This is not a dreamy idea. Blythe Masters, the JP Morgan architect of organized market trading of modern asset backed securities like mortgage backed securities and collateralized debt obligations, became known as one of the great financial engineers in recent decades. Widespread adoption of the trading techniques she devised led to an historic expansion of credit to households and great corporations alike. Subsequently she led innovations in trading of both commodities securities and physical commodities. In 2015 she is leading a new business effort to develop a universal cashless system. Not only is she gathering significant investor interest, but the Federal Reserve and various US Government agencies have become keenly interested in the potential usefulness and efficiencies of a universal cashless system. Needless to say, agencies concerned with illicit uses of cash or cash enabled means of tax evasion are enthusiastic. Estonia, a small country next to Russia with which I am personally familiar, essentially has a cashless economy. They use mobile phones to pay for almost all daily living requirements, including car parking, public transport, fuel, and in fact most of their daily purchases. This system does not yet include records of all personal assets, and especially personal gambling and other private activities. This hasn’t been developed here in the US yet, but one can envisage our government liking the idea. Some officials in the Eurozone have recently advocated the adoption of some kind of standardized, universal cashless system in which taxable revenues, personal income and wealth could not be hidden and taxation could be automated. No doubt there would be resistance in Greece to such a system because evasion of taxes has been the most popular national sport of all Greeks since before the Roman Empire spread to Greece. The people now intensively working on a mechanism for a cashless society are building it around the concept of blockchain technology. In essence, there would be a single ledger that records each expenditure or revenue event (the block), linking them chronologically with every other subsequent purchase, sale, or revenue event in a recorded chain. It could initially begin with a complete ledger of individuals or distinct businesses which could then be connected with another to a bigger ledger that a bank or other large financial institution might maintain for all of its clients. Banks or other designated financial institutions could then link their own comprehensive ledgers with those of the others. If you think about this for a moment, it is evident that the ledger for a big bank like JP Morgan would inevitably include activities throughout the world without respect for borders. Central banks and governments would inevitably encourage even further consolidation so that all significant financial flows and all debts and assets could be monitored in real time, enabling policies and regulations to be adapted to the realities of daily life. The objective of the blockchain that Blythe Masters is pursuing is ultimately to put together a global blockchain, which is consolidated at any moment in time. Everything you have and everything you owe are visible. In the blockchain system no entry can be altered or edited. No asset could be used for more than one transaction. No asset could be used twice for increased spending or investment leverage. Many investors might find this extremely uncomfortable, as it is common practice in banking and investment management circles around the world to use the same assets for re-collateralization. This process is known among bankers as rehypothecation. This would prevent the kind of securitization that many people say is taking place in China, where the same pile of metal ore sitting at the port can be used as collateral several times to borrow money from different banks and nonbank lenders. Nor could you do the kind of rehypothecation that is taking place in London, where the same assets are used to raise leverage by different entities, including banks and hedge funds. This was at the origin of the problems at MF Global for instance and it is quite significant. The British like to keep this system because it attracts a large flow of financial assets held around the world to be transferred to London and held in branches and subsidiaries of foreign financial institutions So we can understand why many governments and central banks don’t like this type of uncontrolled, highly leveraged activity. However, to turn it around, a single ledger for everybody would mean no more privacy, and the end of rehypothecation. We might also consider that if governments could see everything then various regulators would be enabled to issue guidance on what’s normal or appropriate personal and business behavior. If your funds are being used in a statistically abnormal manner then they can start routinely asking you for an explanation, if it was drug money or money laundering or purchases of regulated products like alcoholic beverages or firearms. If you were suspended for drunken driving authorities might like to add to the penalties the prohibition of purchasing or being in possession of an alcoholic beverage at any time during a probationary period. Bad dietary habits could also come under public scrutiny. Regulators motivated by moral self-justification can have boundless imagination in ways to compel proper behavior in society. So cashless, single ledger systems would raise everyone’s concerns about privacy and surveillance. Basically the government would be able to start questioning anyone vigorously about virtually every aspect of daily living. I can understand why they would want this, but it would be appalling for the rights of individuals. Looking at it the other way, cash is used by people for many things. It can be used for things like gambling, but it can also help Russian citizens who have opportunity to interact with foreign visitors to offset the decline of the ruble. In a sense it is refuge that can help individuals to deal with restrictive situations that are not the result of their own behavior. To me this is one of the essential pillars of individual liberties and flexibility. A complete ledger system would place everyone inside a precisely defined, monitorable box with defined set of rules of behavior. If local or national governments found themselves in financial crisis, they would not be limited to European style bail-ins of savings accounts. They could tap personal or family assets directly through the ledger system. Your balance could be altered by government simply by adding one new block to a long chain. One can understand the benefits, but there are potential negative consequences for individuals and businesses, and the Social Contract between citizens and their governments would be threatened. ET: The world has seen an explosion in debt levels since 2007, largely to combat the effects of the Great Financial Crisis, the aftershocks of which can still be felt to this day. Central banks played a crucial role in stabilizing banks and other large financial institutions, monetizing large amounts of government debt and privately held securitized debts in order to reduce borrowing costs and create liquidity to stave off deflation and recession. There are of course limits to this policy, in that economic agents – including the government – end up getting incentivized to borrow even more, thus increasing the inherent financial risks in our economies; shortages of good credit collateral and liquidity may inadvertently develop; and it tends to favor Wall Street more than Main Street, negating trickledown economics that should benefit all. What we can say conclusively is that recent policies are not working well, because the so-called recovery in the last seven years has been the weakest since WWII. Moreover, large asset holders have seen their wealth grow, while the majority of the working class have seen little gain, and in many cases have endured losses owing to loss of value in their homes, or even loss of ownership of their homes. In this context, it seems to us that using actual cash as a primary tool to inject liquidity into the economy has some merit. But this raises a more fundamental question. Rather than issuing debt, part of which would end up being monetized by the central bank under a QE program, the government could print more dollar bills and coins to be disbursed directly for payment of current social and infrastructure programs. Money might go straight to the real economy, rather than through the hands of bankers, without imposing interest charges and without issuance of new certificates of sovereign debt to add to already burgeoning national debt. Having been an economic adviser to several US Presidents, do you think this could be an effective economic policy tool, and as such should we be discussing it more often? HM: You raise a very interesting question about cash going into the real economy versus the banking system. Using actual cash to stimulate the economy is clearly an option. But let’s look at the Federal Reserve. It is really a government sanctioned institution that is owned by its member banks. The banks are eager to receive benefits from this system. The Chair of the Federal Reserve frequently reiterates that its primary objective is to ensure the safety and soundness of its banks. So you can understand why the US central bank would not want to send money outside of the system. It’s not part of its perceived responsibility to its members. You can have a government that could print the money without the central bank being involved, basically sending checks out to everyone. It has been done a few times in the past, with small checks issued by the Treasury Department and mailed to every registered taxpayer in hopes of boosting aggregate consumer spending. In these past experiments such disbursements to households primarily went to paying down debt, not to new purchases. So is the financial system we have in place today bad? I don’t think it is necessarily bad. The central bank wishes to retain some degree of control of the economy and many members of Congress are averse to anything that looks like a free subsidy to the populace. Of course, politicians are not always averse to complex subsidies that hide the reality of redistribution of government resources to specific interest groups like cotton, dairy and tobacco farmers, or to corn producers whose output is sold as ethanol additive to gasoline at a subsidized price. However, QE was intended to increase lending in the economy through the banks. Unfortunately, banks did not increase their lending, but instead diversified their other trading and investing activities, much of which took place globally as they diversified their businesses and their global presence. The main effect of artificially increased liquidity flowing through banks was to pump up the value of assets. People or companies who had them saw their wealth grow, but those who didn’t – which is most people – got relatively poorer as a result. In my view, QE has essentially widened the wealth gap between the poor people and the wealthy but it didn’t improve or help the broader economy. Worse, it encouraged companies to borrow money at near zero interest to buy back their own shares during recent years when revenues and earnings were not growing very much, thus giving the appearance of better quarterly results and higher stock valuations, and of course enhancing the wealth of business leaders and their directors, all of whom held shares. In the last seven years since the breakout of the Great Financial Crisis the world has experienced a real deficiency of capital flowing to new capacity, or productivity. The real economy was not expanded. Instead wealth was redistributed in the form of rising asset values, while wages and household incomes remained stagnant. Personally, I feel compelled to add my own opinion as an economist that QE was a failure in stimulating lending and economic growth in our advanced economies, and a failure by widening the wealth gap of our societies. The US administration might have accomplished something different via fiscal policy instead of having all these liquidity injections, but the President and Congress failed to devise a true package of economic growth stimulus. The Federal Reserve then took it upon itself to conjure up QE as an attempted substitute for the failures of Congress and the President. What we have learned is that monetary policy cannot be an effective substitute for meaningful fiscal policy. Indeed, a few decades from now people will most likely look back and view period this as one of the great economic mistakes in modern history. ET: Everyone talks about the lack of infrastructure investment in the US. Would it be better for the economy if the government had spent, say, $500 billion to pay for new infrastructure projects by printing $100 bills rather than more QE? HM: Yes. The increased fiscal flow into the economy would end up in the pockets of people involved in construction, maintenance and so forth – essentially into capital spending and consumption rather than into the stimulation of financial activities. ET: There is a real risk associated with this policy which is the government overdoing it. Once a politician gets unfettered access to a printing press there’s no stopping his or her programs getting funded. In theory debt has built-in features to keep the borrowers honest (which of late has been somewhat disabled by the central banks); however, with cash you can just print it to infinity – like in Zimbabwe, but most likely with the same consequences. Unconstrained money printing inevitably will result in inflation across all of society. Curiously, despite the benefits of cash in conducting economic activity, governments look at their citizens using cash with great suspicion. Some economists have recently begun to suggest that Western economies should ban it altogether as a way to avoid hoarding and promote private consumption growth – we suspect along the lines of what the FDR Administration did to gold in the 1930s [until then gold and silver had been used as currency in the US]. While this may seem far-fetched, Louisiana has banned cashed transactions on second hand purchases and several EU economies have prohibited cash purchases of items above a certain value. US citizens entering and leaving the United States must declare large amounts of cash they may be carrying, and there have been frequent seizures of such cash by government officials on the suspicion that large sums of cash are likely to be used for illicit activity or tax evasion. The reality now is that cash no longer flows freely through the economy. What it is your reaction to these events? HM: Things are a little different depending on the economy you are looking at. In Europe there’s a problem in that individual compliance with taxation rules is resisted. Wealth is often hidden so as to leave an impression of insufficient income or wealth. Governments across Europe introduced value added tax administration because it was a mechanism for automatically deducting consumption, or sales taxes at each step from raw materials to manufacture to distribution to final retail consumption. Value added taxes are automatically applied by cash registers and bookkeeping requirements. The idea of introducing value added taxes or some other form of consumption taxation has been discussed in Congress from time to time, but it has been vigorously opposed by Democrats as discriminatory towards lower income families. So this type of tax has been very useful especially in Southern Europe where not paying taxes has been a national privilege for decades, if not centuries. Still, there continue to be serious tax avoidance problems that tax authorities are trying to tackle. In Italy people using fancy cars and clothes at upscale ski resorts and beaches are closely monitored and audited to scrutinize sources of such extravagances. The case of Greece is even more extreme because it is almost impossible to collect taxes. The major source of income is tourism, and authorities are highly reluctant to resolve domestic tax deficiencies by piling taxes on tourists, which might result in diminished flow of visitors to Greece. So it is understandable that the authorities there would try to limit cash purchases to address this issue. In the US the situation is a little different. The banks would really like to have a means to hold or control title on everything. The Fed would like to have a more direct control of the economy and the IRS would like to have greater oversight. The motivation here is not deficiency of the economy but rather deficiency of governance. Taxation at the local or state level is much more issue-specific, including property taxes, licenses, mandatory fees for services, and so forth. I think the Fed is frustrated that QE has not resulted in higher levels of investment and growth, which is why they would like to have greater control of the economy, not less which is what would happen via the issuance of bills. ET: Looking at the broader picture, do you believe the dollar being the world’s reserve currency brings more net benefits or net costs to the US economy at this stage? HM: That’s a debate that has been going on for many decades and there are people on both sides. The economies of Asia and Europe are troubled, and emerging markets more broadly are in the downward phase of the economic cycle as a result of an historic slowdown of world trade. The primary driver of growth in those emerging markets is exports because domestic consumption is weak. When world trade was robust they had a strong boost to their economies which could not be achieved internally. But now their export demand has fallen off and domestic demand remains inadequate to drive a desired rate of economic growth. Plus we have Germany, France and the UK which are also very export dependent. As these economies weaken, we may see a liquidity crisis. In this environment, for example companies in Russia would rather own dollars than rubles. The Russian government is now trying to ban use of dollars or other foreign currencies, not for geopolitical reasons but because the Russian government and its central bank have an acute shortage of dollars that is continuously worsening as world demand for Russian resources continues declining. Beside the US Dollar, the other most liquid currencies are Sterling and the Japanese Yen. Sterling actually has the peculiar feature that mobile money in the world likes to go to London. It is a nice place to live close to Continental Europe, a big financial center and the courts protect the rights of asset holders. In Japan the government is so involved in the yen through its vast government managed or regulated pension and savings system that market liquidity remains strong even though Japan’s financial markets suffer ups and downs. When world markets suffer a downturn, Japanese investors are quick to repatriate wealth held abroad, keeping the Yen stronger than it might otherwise be. The US economy has weaknesses, but it also is far more resilient than most other economies around the world. The US financial markets have far larger liquidity than any other market in the world, so holding assets denominated in dollars assures that buyers and sellers will be available at times of declining financial confidence. If emerging markets continue in their downward trajectory or if anything goes wrong elsewhere, particularly in China, there would likely be an increase in demand for dollars primarily because it is the most liquid alternative asset. Even if we had a downturn in this market there would be global demand for dollar assets – just to park anywhere in the US because the expectation would be that the dollar would be rising in relation to other currencies. So this money inflow can go into stocks, bonds and real estate. And this will benefit the US in the event of a global recession. If there is one, the US would probably be the first to recover and it would be because of this liquidity provided by the dollar. I can see why people say that the dollar is costly, but for now and in the next few years it will be hugely beneficial to the US. And I cannot see the dollar collapsing any time soon. The Chinese are increasingly using their currency in international transactions. But if you look closely the other countries with which China is now trading have no money, so they can either barter or use the Chinese currency system. The wealthy Chinese park as much money in dollars as they can, which is why capital flight from China is huge and growing. Chinese capital flees to the US in various forms. For example, they send their kids to study here and before graduating they set up businesses which are then capitalized by their wealthy parents, enabling the kids to get “green cards” or residency permits. I hear that most Chinese juniors in the US are told by their parents not to return home. And millions of dollars are coming in to buy real estate and other assets put under the supervision of sons, daughters, and other relatives. So the dollar is a good thing to have for the next several years. And it’s hugely beneficial to us during times of global slowdown. By the way, negotiating the emergence of an alternative to the dollar would take a decade or more, and it would be really painful. It’s nothing that can happen at the snap of a finger. I don’t see it any time soon; something for the next century perhaps. ET: But if the US were to ban the use of dollar bills, would this not mean the certain demise of the dollar as the world’s reserve currency? After all foreigners hold an estimated 70% of all US dollar currency and would dump it in a hurry if it were banned, in exchange for some other currency, likely from a major US economic rival. HM: I think that’s right. It would not be painless for us. A lot of this money is what we used to call some years ago “hot money”. So the question is where would it go? And that’s not an easy question to answer. A lot of people say well it’s going to go to gold. I have had many discussions about this with traditional gold traders in Europe, where there is gold trading experience going back centuries. Their view is that you can take some gold home, but if you are talking millions or even billions then you have a problem. You can only move that much money if you use an armored vehicle and strong guards to move heavy gold caches. And given that you will want to see and touch it, if you store it in your basement people will eventually discover you have it and try to steal it. If you leave your gold in a bank, the bank will seize it and use it if the bank falls into distress, perhaps leaving you a promissory note. Basically gold is heavy, not secure enough for holding by individuals, and not easily moved. So where do you go then? If there is another highly liquid alternative then OK. If the Eurozone were healthy maybe the Euro would be a possibility, or you might park in Sterling for a while. Would there be a creation of something else? Maybe if such a scenario unfolds in the future, but this would likely be a creation of private interests and not governments, and which in fact would be used to usurp the power of governments. In the UK we can see emerging experiments with locally issued scrip as currency substitutes, usable among agreed parties. That particular experiment seems to be growing in scale this year. ET: Prof. Malmgren, it has been a real pleasure talking with you. Thank you very much for sharing your insights with us. HM: Thank you. |

|||

Submitted by Bill Bonner via Bonner & Partners (annotated by Acting-Man's Pater Tenebrarum),

|

|||

Submitted by Alasdair Macleod via GoldMoney.com, The Danger Of Eliminating CashIn the early days of central banking, one primary objective of the new system was to take ownership of the public's gold, so that in a crisis the public would be unable to withdraw it. Gold was to be replaced by fiat cash which could be issued by the central bank at will. This removed from the public the power to bring a bank down by withdrawing their property. A primary, if unspoken, objective of modern central banking is to do the same with fiat cash itself. There are of course other reasons for this course of action. Governments insist that they need to be able to trace all private sector transactions to ensure that criminals do not pursue illegal activities outside the banking system, and that tax is not evaded. For the government, knowledge of everything individuals do is necessary control. However, in the monetary sense, anti-money laundering and tax evasion are not the principal concern.Central banks are fully aware that the financial system is fragile and could face a new crisis at any time. That's why cash in their view must be phased out. A gold run against a bank or banks, in the ordinary course of banking, is no longer a systemic threat, but the possibility that depositors might queue up to withdraw physical cash from a bank in which they have lost confidence is very real. Furthermore it is a public spectacle associated with monetary disorder of the most alarming sort. It is far better, from a central banker's point of view, to only permit the withdrawal of a deposit to be matched by a redeposit in another bank. That way, a bank run can be hidden through the money markets, with or without the intervention of the central bank, and the deflationary effects of cash hoarding are avoided. This is commonly understood by followers of monetary matters. What has not been addressed properly is how a cashless economy behaves in the event of a significant alteration in the public's preferences for money relative to goods. Normally, there is a balance in these matters, with the large majority of consumers unconcerned about the objective exchange-value of their money. There are a number of factors that can change this complacent view, but the one that concerns us for the purpose of this article is the speed at which the relationship between the expansion of money and credit and the prices of goods and services can change. There is no mechanical link between the two, but we can sensibly posit that the extra demand represented by an increase in the money quantity will eventually drive up prices, setting the conditions for a potential shift in public preferences for money, which would drive prices up even more. When the general public perceives that prices are rising and will continue to do so, people will buy in advance of their needs, increasing their preference for goods over holding money. This is currently desired by central bankers wishing to stimulate demand, but they are under the illusion it is a controllable process. Furthermore, increases in the money quantity are being driven by factors not under the direct control of monetary authorities. Welfare states are themselves insolvent and require the issuance of money and low-interest credit to balance their books. Commercial banks can only continue in business if the purchasing power of money continues to fall, because their customers are over-indebted. Unless the expansion of the money quantity continues at an increasing rate, the whole financial system will most likely grind to a halt. It is now required of central banks to ensure the money quantity continues to expand sufficiently to prevent systemic failure. It is therefore only a matter of time, so long as current monetary policies persist, before it dawns on the wider public what is happening to money. Preferences will then shift more definitely against holding money, radically altering all price relationships. If this leads into a hyperinflation of prices, which is the logical and unavoidable outcome, the speed at which money collapses will be governed in part by physical factors. In the case of Germany's great inflation in the 1920s, the final collapse can be tied down to a period of six months or so, between May and November in 1923, after a last-ditch attempt to control monetary inflation failed. The limiting factor in this case was the time taken to clear payments through the banking system, and when prices began to rise so rapidly that cheques lost significant value during the clearing and encashment process, the economy moved entirely to cash. When prices rose faster than cash could be printed, the limitation on the purchase of necessities then became one of cash availability. It is in truth impossible to isolate all the factors involved, and the course of events during the destruction of a currency's purchasing power is bound to vary from case to case. Today the situation is very different from the hyperinflations in Europe over ninety years ago. A society which uses electronic transfers spends bank deposits instantly. The merchant, who is subject to the same panic over the value of the payment received looks to dispose of his cash balances as rapidly as possible as well. In other words, the electronic transfer of money has the potential to facilitate a collapse in purchasing power at a rate that is far more rapid than previously experienced. The most obvious delaying factor left becomes the speed with which the public realises that government money has no value at all. People are generally ignorant of monetary matters, and a majority of them have no alternative but to believe in their money, because without it they are reduced to barter. It is entirely human to wish these concerns away. For a minority of the population lucky enough to have a combination of wealth and foreign currency bank accounts the problem was not so great in the past, but the interconnectedness of the global monetary system suggests that all today's fiat currencies face the same problem contemporaneously, and there is no refuge in foreign currency. These concerns have encouraged the development of alternative solutions, such as our own Bitgold/GoldMoney payment and storage facility, which will allow both consumers and producers to reduce their exposure to the banking system and continue to trade. There are also private currency alternatives such as bitcoin. Whether or not alternative currencies have a future monetary role for ordinary people at this stage looks unlikely, primarily because they are less stable than government currencies; however that might change in the future. They represent a work-in-progress that has the power to undermine the state monopoly on money, not least because they lie outside a government's ability to manage capital controls directed through the banks. What fascinates many of those with an understanding of anticipatory private sector solutions, is the potential for triggering a seismic change in the money used today. They have the ultimate potential to free commerce from the whole concept of a state-directed monetary policy. Rapidly developing technological solutions are therefore another factor that could accelerate the public rejection of government money and the state-licensed banking system, simply by offering a practical alternative to a debasing currency. With the progress being made to eliminate cash and the private sector's ability to develop an alternative financial system in advance, if the collapse of government money comes, it could be very swift indeed.

|

|||

2011 2012 2013 2014 |

|

||

| THEMES - Normally a Thursday Themes Post & a Friday Flows Post | |||

I - POLITICAL |

|||

| CENTRAL PLANNING - SHIFTING ECONOMIC POWER - STATISM | THEME | ||

- - CORRUPTION & MALFEASANCE - MORAL DECAY - DESPERATION, SHORTAGES. |

THEME |  |

|

| - - SECURITY-SURVEILLANCE COMPLEX - STATISM | M | THEME | |

| - - CATALYSTS - FEAR (POLITICALLY) & GREED (FINANCIALLY) | G | THEME | |

II-ECONOMIC |

|||

| GLOBAL RISK | |||

| - GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | G | THEME | |

| - - SOCIAL UNREST - INEQUALITY & A BROKEN SOCIAL CONTRACT | US | THEME | |

| - - ECHO BOOM - PERIPHERAL PROBLEM | M | THEME | |

| - -GLOBAL GROWTH & JOBS CRISIS | |||

| - - - PRODUCTIVITY PARADOX - NATURE OF WORK | THEME | MACRO w/ CHS |

|

| - - - STANDARD OF LIVING - EMPLOYMENT CRISIS, SUB-PRIME ECONOMY | US | THEME | MACRO w/ CHS |

III-FINANCIAL |

|||

| FLOWS -FRIDAY FLOWS | MATA RISK ON-OFF |

THEME |  |

| CRACKUP BOOM - ASSET BUBBLE | THEME | ||

| SHADOW BANKING - LIQUIDITY / CREDIT ENGINE | M | THEME | |

| GENERAL INTEREST |

|

||

| STRATEGIC INVESTMENT INSIGHTS - Weekend Coverage | |||

|

SII | ||

|

SII | ||

|

SII | ||

|

SII | ||

| TO TOP | |||

Read More - OUR RESEARCH - Articles Below

Tipping Points Life Cycle - Explained

Click on image to enlarge

{kind=link}

{kind=link}

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

TO TOP