The Telegraph reports on the Greek debt deal announced today .. identifies several challenges actions which must be taken to keep the deal going .. "Greece has to push a series of austerity demands through parliament by this Wednesday in order to unlock a fresh multi-billion euro .. Greece has until Wednesday to pass laws that:

• Implement VAT hikes • Cut pensions • Take steps to ensure the independence of Greece's statistics office is maintained • Put measures in place to automatically slash spending if Greece fails to meet its targets on primary surpluses.

It has until July 22 (an extra week compared with a draft statement) to: • overhaul its civil justice system • implement the Bank Recovery and Resolution Directive (BRRD) to bring bank resolution laws in line with the rest of the EU

"In our view, there are two main factors keeping investors sidelined.One is the residual implementation risks involved in the latest arrangements... The second, of much broader importance, is the accumulated evidence of the inadequacy of the Euro area's present fiscal governance, which takes up too many resources and exposes the whole system to collapse."

Despite the euphoria in global equity markets, The FT's Wolfgang Munchau - once one of the keenest euro enthusiasts - warns regime change is coming in Europe. The actions of the creditors has "destroyed the eurozone as we know it and demolished the idea of a monetary union as a step towards a democratic political union," Munchau exclaims, fearing they have "demoted the eurozone into a toxic fixed exchange-rate system, with a shared single currency, run in the interests of Germany, held together by the threat of absolute destitution for those who challenge the prevailing order." He concludes rather ominously, "we will soon be asking ourselves whether this new eurozone, in which the strong push around the weak, can be sustainable."

With the provocative and dramatic Greek "time out" language pulled from the final finmin and summit draft language, the two most humiliating aspects of the latest extend and pretend "deal" for the Greek people will be the return of the Troika's (surely we can call it the Troika again as part of the Greek capitulation) IMF mission to Athens, and the escrowing of some €50 billion in Greek assets in a liquidation fund.

Granted said fund will not be domiciled in Luxembourg as was originally envisioned, but Europe will still have control and first refusal rights over what are technically Greek properties, in the process Athens handing over about 25% of Greek GDP (and sovereignty) over the Brussels.

What are these assets? For the answer we go to the horse's mouth, Jeroen Dijsselbloem, who laid out the holdings of the proposed Greek privatization that would be sold off as follows: "it still is going to be an independent fund, valued at €50 billion which can beairplanes, airports, infrastructure and most certainly banks.”

Bloomberg quotes the Eurogroup finmin president:

They will be brought in with the target to privatize those in the coming years, but we will take our time for that.

We then hope for proceeds of EU50 billion, but that will be clear later.

The banks first have to be refinanced from this aid program, but after that I take it that they’re worth money and then we can sell them.

The proceedings are aimed at lowering Greece’s national debt.

In other words, Greece will be liquidated piecemeal to repay creditors. In even other words, the proceeds from the Third Greek Bailout will not only not reach the Greek people, but Greece will have to sell itself in pieces to top off the creditors' funding needs.

Dijsselbloem concludes: "That is good for Greece, but also good for us. We are in the end the ones from whom the money is borrowed."

It was not exactly clear why this would be good for Greece.

So for all those curious, here are some of the "assets" that already have, or soon will hit Ebay.

The only caveat: when (not if) Greece defaults again, and it is time to collect on Europe's secured DIP loan (which is what the Third bailout really is) collateral because not even the French socialists can push for a fourth bailout, good luck trying to repossess Aegean islands or the Santorini ferry terminal.

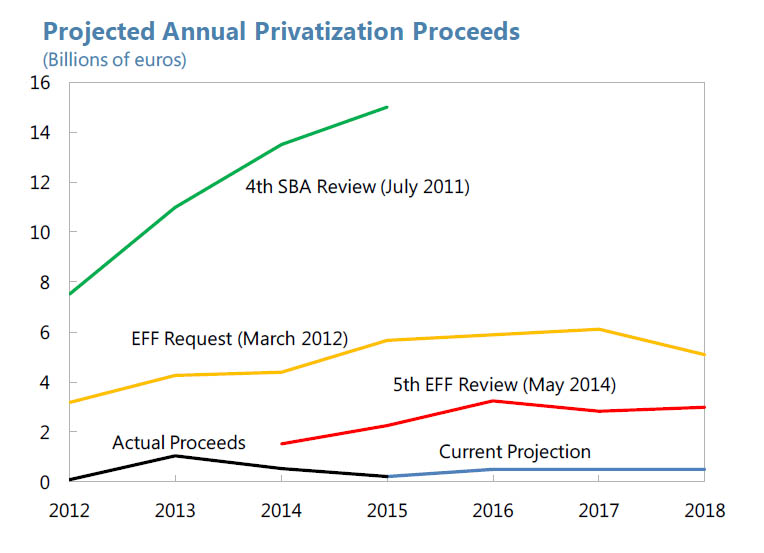

Oh, and for those struck by a case of deja vu, the €50 billion privatization "plan" is nothing new: it was first proposed by the IMF in 2011. This is what happened next:

What does the IMF say now about this latest privatization proposal? "Not realistic."

Which may be a problem for Greek banks since as the summit deal envisions, half of the privatization "proceeds" will go to recapitalize Greece's insolvent banks. Proceeds which the IMF projects will be about €2 billion until 2018!

This is a problem because with this implicit admission that the Greek financial sector will effectively never receive the needed funds to remain stable, any ELA increase by the ECB will be promptly used by Greek depositors to yank as much money as they can, awaiting the next weekly dose of monetary generosity from Mario Draghi, as both capital controls and the Greek bank run remain a permanent fixture of Greek daily life.

As outlined exhaustively here over the past 24 hours, the new “deal" for Greece has implications far beyond the Aegean and may well mark the beginning of the end for the EMU experiment. But leaving the bigger picture implications aside for now, the two most important short-term considerations for Greece are: 1) establishing political stability, and 2) stabilizing the banks.

The new Greek deal is "absolutely impossible, totally non-viable and toxic …[they were] the kind of proposals you present to another side when you don’t want an agreement." Speaking with The New Statesman, former Greek FinMin Yanis Varoufakis blasts Wolfgang Schaeuble's position which will lead to "a humanitarian crisis" for Greece and warns, regarding this latest creditors' proposal, "if anything it will be worse [for the Greeks]." His conclusion is succinct, "we were set up...,"Merkel and Schäuble’s control over the Eurogroup is absolute, and that the group itself is beyond the law.

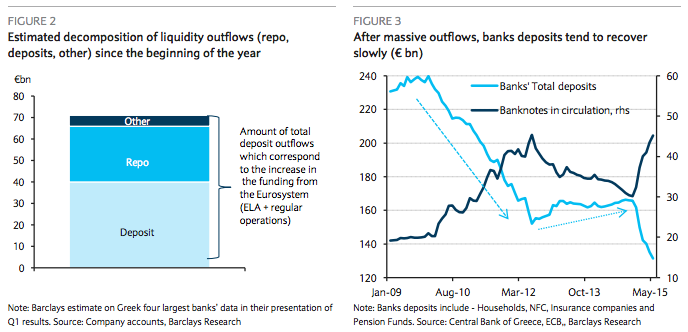

Even with a deal in place and a new program for Greece on the horizon, the country's banks are by no means in the clear as deposit outflows, limited breathing room under ELA, and deteriorating asset quality present formidable stumbling blocks going forward.

On Friday in "Don’t Tell Merkel, Greek Banks Need Another €10-14 Billion Bailout," we warned that the €53 billion aid request from Greece was likely only part of the story. The country’s banks, which were (and still are) on the verge of collapse would need to be recapitalized and according to one banking official who spoke to Reuters, that cost of that recap would be somewhere in the neighborhood of €14 billion.

Fast forward 24 hours and that €14 billion had turned into €25 billion, bringing the total estimated cost of the proposed ESM program for Greece to some €76 billion. EU finance ministers balked at the figure and by Sunday it was clear that creditors intended to extract the harshest set of concessions yet out of Athens in return for a new program. After 13 hours of negotiations in Brussels, EU leaders reached an agreement in principle which will require PM Alexis Tsipras to push a draconian set of reforms through parliament by Wednesday. But even if Greece does manage to secure a new bailout this week which includes the €25 billion in recap funding via the agreed upon escrow fund, the banks are by no means out of the woods. Here’s what we said on Friday:

Indeed, even if a deal is reached this weekend and the ECB raises the ELA cap on Monday, it’s difficult to imagine that the deposit outflows will cease (would you trust your deposits in a Greek bank even with a "deal"?) and as suggested above, if capital controls are lifted, the situation will be even worse because Greeks will simply take the opportunity to withdraw all of their money at once. With the liquidity "cushion" down to just €750 million (according to same official who spoke to Reuters about the recap needs), deposit flight will clearly have to be funded via more ELA, which means whatever is left in terms of pledgable collateral will soon disappear even under the rather optimistic assumption that outflows are kept at between €80-100 million per day (the current run rate). At that point (unless the ECB decides to buy the banks more time by substantially lowering haircuts), it's recap time and then ... well, see above.

In the final analysis, no one is going to trust Greek banks for a very, very long time and talk of a depositor bail-in won't do anything to help the situation. The acute lack of confidence means that any capital injected from EU bailout funds will promptly disappear as depositors continue to pull their funds, while the county's rapidly deteriorating economic situation simultaneously drives up NPLs.

Now, Barclays is out reinforcing virtually all of the above on the way to explaining why the banking system is and will continue to be Greece’s "Achilles heel":

As of the end of 2014, Greek banks’ total borrowing at the ECB’s regular operations amounted to €56bn, with negligible usage of ELA. Their usage of the ECB liquidity has increased to about €118bn as of the end of May and we estimate to €125.4bn currently, of which €38.8bn at the MRO and LTRO, while the ELA funding via the Central Bank of Greece should be close to the current limit of €89bn.

The capital controls introduced on 29 June after the announcement of the referendum have reduced significantly the pace of deposit outflows. However, with depositors continuing to withdraw from ATM machines at a limit of €60 per day, Greek banks’ liquidity needs have reached a level very close to the current ELA ceiling. Therefore, for some of them the risk of running out of liquidity in the very near term is high, especially if the ECB keeps freezing the ELA provision at the current level of €89bn.

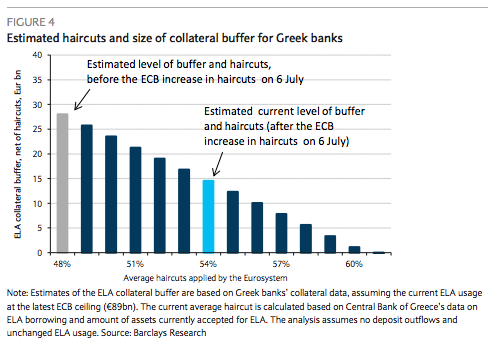

Based on some unconfirmed figures reported on Bloomberg (stating that the adjustments regard mainly securities issued or guaranteed by the Greek government for which the haircuts were brought to 45%), we estimate that the average haircut has been increased to about 54% from our previous estimate of 48%. This would imply a reduction in the ELA-eligible collateral buffer (net of haircuts) from our initial estimate of €28bn as of the end of June to about €15bn currently.

While the current collateral buffer (which we estimate at around €15bn) should allow Greek banks to keep operating if the ECB’s Governing Council approves a further increase in the ELA, we think it will not be enough to absorb any significant increase in deposit outflows in the event that capital controls are eased and banks are reopened. A tiny collateral buffer limits the banks’ capacity to borrow ELA liquidity. Also we suspect that the remaining spare collateral is not evenly distributed among the four largest banks, and therefore some of them are likely to be in more of a stressed liquidity situation than the others, making them more vulnerable to any further bank run. Therefore, we believe that capital controls should remain in place for a long period even if there are positive developments in the negotiations and the ECB eventually increases the ELA ceiling. We believe also that further tightening of the daily cash withdrawal limit from the current €60 might be needed, just to reduce the outflow of banknotes.

On Monday 13 July, the ECB’s Governing Council is expected to meet to decide on ELA support for Greek banks. Following the outcome of the 11-12 July meetings, paving the way for a continuation of the negotiations, we think the ECB is likely to keep the ELA ceiling at the current level of €89bn and to moderately increase it only after approval of reforms by the Greek Parliament on Wednesday 15 July. However, even if the ELA is increased, we expect the ECB to maintain its cautious approach with a very gradual step up of the limit depending on the evolution of negotiations.

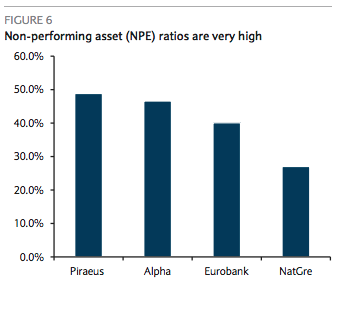

But even if Greece averts an EMU exit and its banks continue to receive liquidity through the ELA, the country’s entry into a new programme will still likely require banks to raise capital in order to bolster solvency and cushion them against asset quality deterioration associated with a weakened economy. The average non-performing exposure ratio (NPE) is 41%, already very high but now also at risk of continually increasing over the coming quarters. Ultimately, however, a strengthened capital system is needed to help restore confidence and therefore deposits. A fresh balance sheet assessment and stress test reflecting the revised macro-economic climate cannot be ruled out as a pre-requisite of a new programme and could be the catalyst for identifying fresh capital needs.

So just as we said, the solvency of the banking system is still very much an issue and far from alleviating the need for capital controls, the days and weeks (and perhaps months) ahead will likely see capital controls get tougher in order to stem the deposit outflow and prevent the weakest of the four large banks from running out of pledgable collateral.

Furthermore, the rapid deterioration in the Greek economy could well mean further asset impairment, necessitating the need for still more capital injections going forward.

As we noted last Monday, a crisis of confidence is nearly impossible to reverse in the short-term and if there is any place on earth where confidence is in short supply, it's at Greek banks.

And just moments ago:

GREECE TO EXTEND BANK HOLIDAY, CAPITAL CONTROLS TODAY: OFFICIAL

ECB SAID TO KEEP GREEK EMERGENCY LIQUIDITY CEILING UNCHANGED

What is on display more brightly and clearly than ever, though, is the utter fakery of international banking. The players have lost faith in their own shenanigans. They simply go through the motions now awaiting the political fallout, which is to say the revolt of the people who can still do arithmetic. The old refrain, “your check is in the mail” may not be so reassuring to folks who haven’t eaten for three days. Personally, I would expect the gasoline bombs to be flying around Syntagma Square before the middle of the week.

Now that Greece has capitulated and offered up its sovereignty in what can only be described as an unconditional surrender to Berlin and Brussels, here's what's next for the country, the government, and the Greek people.

WHAT’S NEXT?

The Greek govt is set to renew a bank holiday and capital controls decree which expires today

The ECB’s GC is expected to discuss ELA for Greece’s banks

Eurogroup meeting later today will work on Greece’s short-term needs and discuss bridge financing

Greece has accepted to legislate on 4 action points by Thursday July 16, and another two by July 22, according to Malta’s PM Muscat

Then Greece would come before the Eurogroup and euro- area member states would decide to open or close the needed negotiations that would let the ESM to disburse funds, Muscat says

Dutch PM Rutte says it could take weeks to negotiate Greek ESM aid deal

WHAT DOES IT MEAN FOR GREECE’S BANKS?

Greek banks are to be recapitalized by Greek asset fund and Tsipras says the deal protects the stability of the banking system

ELA will stay in place all the while that another bailout is in the pipeline, Mizuho’s Peter Chatwell says in e-mailed comments

ECB ELA will most likely stay in place until at least Wednesday, pending Greek ability to legislate the list of prior actions, Oxford Economics says in a note

WHAT ABOUT TSIPRAS AND SYRIZA?

Support at Wednesday’s vote from Greece’s pro-Europe parties will come at a cost, when the timing is right, Barclays says

It makes more sense for those parties to let PM Tsipras bear the political cost of capital controls while triggering elections would make default inevitable, plunging the country into a complete paralysis for the next 30 days

Don’t entirely rule out a coalition partner change (with To Potami), and believe this situation will eventually lead to new elections after the summer

A new unity govt or an early election very possible, Rabobank says

Given political fractures in Greece, passage of the proposal through parliament is far from certain, Richard Cochinos, strategist at Citigroup, says in client note

Decent likelihood of a Greek cabinet reshuffle; govt could possibly fold on reforms

Tsipras may seek to expel those opposed to a deal with creditors from the party as he no longer commands a majority in parliament, Reuters said, citing people familiar

“Constructive” centrist parties will likely continue to support the government coalition, Barclays says

Snap elections necessary but can’t take place now, Greece’s Labor minister Skourletis says

WHAT ABOUT ITS CREDITORS?

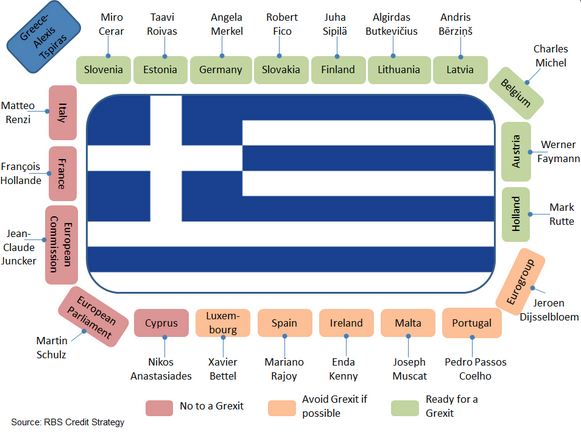

Germany, the Netherlands, Austria, Slovakia, Estonia and Finland all need parliamentary approval to open negotiations on a new Greek program, an EU official said last week, while France’s Hollande said French National Assembly to vote on the deal on Wednesday

While Marcel Fratzscher, president of the DIW economic institute, says it will be very difficult to sell the deal to German voters and Germany’s Greens say the deal means Greece will be stuck in a recession, a govt lawmaker said it is likely the German coalition will approve the deal

Rutte says he’s unhappy he has to break an electoral promise to Dutch constituents on no further Greece aid

The deal is so tough there’s a better than even chance that the Finnish parliament will authorize the negotiations, Berenberg’s Holger Schmieding writes in e- mailed comment

Even if a deal can eventually be reached to keep Greece in the euro area, there will be long-term consequences, the damage done to relations between France and Germany may prove irredeemable while Germany’s suggestion Greece be granted a short term exit from the single currency shatters the principle that euro-area membership is irrevocable, Oxford Economics says

IS THERE ANY AGREEMENT ON RESTRUCTURING GREECE’S DEBT?

Over the weekend, an IMF source told Reuters said that if other creditors couldn’t agree on a haircut, grace periods on interest payments could be combined with lower rates and extended maturities

Tsipras said the negotiations had managed to gain restructuring while Merkel confirmed interest-payment grace periods and longer maturities will “be discussed once there is a successful evaluation of the new Greek program”

WHAT ABOUT GREXIT?

Tsipras says summit outcome averts collapse of banking system

Risks of a Greek exit have reduced in the very short term as the ECB should remain supportive as long as prior actions are passed in Parliament by Wednesday and talks are headed in the right direction, Barclays says

The chances of a Grexit have now fallen below 50%, UBS WM write

The deal and Wednesday’s vote may stretch the Greek govt to breaking point, forcing new elections; the month’s hiatus that would ensue while elections took place would almost certainly see Greece ejected from the euro area, Oxford Economics says

"Exit from the currency block is now officially something that can be used as a threat to those that don’t behave the German way."

"The last six months' crisis has exposed weaknesses in the Eurozone's governance framework that will likely reverberate for months and years into the future."

"Greece will continue to fight, and we will continue to fight, so that we can return to growth, regain our lost national sovereignty"

Prime Minister Alexis Tsipras’ statement following the conclusion of the Eurozone Summit

We have been fighting hard for six months now, and we fought until the end to achieve the best possible outcome, an agreement that will enable the country to get back on its feet, and for the Greek people to be able to continue to fight.

We faced tough decisions, tough dilemmas. We assumed responsibility for the decision in order to prevent the most extreme objectives from being implemented—those pushed for by the most extreme conservative forces in the European Union.

The agreement calls for tough measures. However, we prevented the transfer of public property abroad, we prevented the financial asphyxiation and the collapse of the financial system—this was planned to the last detail – having recently been designed to perfection, and in the process of being implemented.

Finally, in this tough battle, we managed to gain the restructuring of the debt and a financing process for the medium-term.

We were aware that it would not be an easy task, but we have created a very important legacy. An important legacy, and a much-needed change throughout Europe. Greece will continue to fight, and we will continue to fight, so that we can return to growth, regain our lost national sovereignty. We earned our popular sovereignty. We sent a message of democracy, a message of dignity throughout Europe and the world. This is the most important legacy.

Finally, I would like to thank all of my colleagues–ministers, colleagues and associates who gave, along with me, a very tough fight. A fight, which at the end of the day, will be vindicated.

Today’s decision will maintain Greece’s financial stability and provide recovery potential. However, as we knew beforehand, the agreement will be difficult to implement. The measures include those that Parliament has voted on. Measures that will inevitably create recessionary trends. However, I am hopeful that the growth package of 35 billion euro that we achieved, debt restructuring, as well as securing funding for the next three years will create market confidence, so that investors realize that fears of a Grexit are a thing of the past—thereby fueling investment, which will offset any recessionary trends.

I believe that a large majority of the Greek people will support the effort to return to growth; they acknowledge that we fought for a just cause, we fought until the end, we have been negotiating through the night, and no matter what the burdens will be, they will be allocated – we guarantee this – with social justice. And it will not be the case that those who have shouldered the burden during the last years will be stuck footing the bill once more.This time, those who avoided paying—many of whom were protected by the previous governments–will pay now, they, too, will shoulder the burden.

Finally, I want to make this commitment: Now, we need to fight just as hard as we fought to achieve the best outcome abroad-in Europe, to rid vested interests in the country. Greece needs radical reforms in favor of social forces, and against the oligarchy that have led to the country’s current state. And this commitment to this new effort begins tomorrow.

Just around 9am CET, after a 17-hour mammoth all-night session, Greece did manage to cobble together a "deal" if one may call this latest embarrassing can-kicking that, which was nothing short of total capitulation by Tsipras. As part of the deal, Greece "surrendered to European demands for immediate action to qualify for up to 86 billion euros ($95 billion) of aid Greece needs to stay in the euro" in the words of Bloomberg.

For those who missed today's festivities in Brussels, here is the 30,000 foot summary: Europe has given Greece a "choice": hand over sovereignty toGermany Europe or undergo a 5 year Grexit "time out", which is a polite euphemism for get the hell out.

Here are the 12 conditions laid out as a result of the latest Eurogroup meeting, which are far more draconian than anything presented to Greece yet and which effectively require that Greece cede sovereignty to Europe, this time even without the implementation of a technocratic government.

Streamlining VAT

Broadening the tax base

Sustainability of pension system

Adopt a code of civil procedure

Safeguarding of legal independence for Greece ELSTAT - the statistics office

Full implementation of automatic spending cuts

Meet bank recovery and resolution directive

Privatize electricity transmission grid

Take decisive action on non-performing loans

Ensure independence of privatization body TAIPED

De-Politicize the Greek administration

Return of the Troika to Athens (the paper calls them the institutions... for now)

One alternative, generously presented to Greece, is for the country to put some €50 billion of assets - the best ones - in escrow to creditors. A more polite way of putting would be a Greek secured loan.

Greece would place about €50 billion of state assets into an independent company.

Those assets could serve as collateral against aid loans.

Greece is told to set aside a quarter of its GDP for Europe to do as it sees fit, and which can be "seized" if Greece is seen as veering away from its third bailout promises again.

And since Greece has no option but to promise everything and the moon, it will surely comply hoping that it is once again allowed to promptly forget all the promises as soon as it pockets some of that €86 billion in new bailout funds just to unlock the €120 billion in deposits held hostage in Greek banks by the ECB, even if the resulting debt will push Greek debt/GDP well above 200%.

"In case no agreement could be reached, Greece should be offered swift negotiations on a time-out from the euro area with possible debt restructuring."

EU finance ministers have effectively given Greece 24 hours to accept the set of rather draconian conditions outlined in a “draft” term sheet leaked to the press earlier today.

As a reminder, here are the stipulations:

fully comply with the medium-term primary surplus target of 3.5 percent of GDP by 2018, according to a yearly schedule to be agreed with the institutions;

carry out ambitious pension reforms and specific policies to fully compensate for the fiscal impact of the Constitutional Court ruling on the 2012 pension reform and to implement the zero deficit clause;

adopt more ambitious product market reforms with a clear timetable for implementation of all OECD toolkit I recommendations, including Sunday trade, sales periods, over-the-counter pharmaceutical products, pharmacy ownership, milk, bakeries. On the follow-up of the OECD toolkit II, manufacturing needs to be included in the prior action;

on energy markets, the privatization of the electricity transmission network operator (ADMIE) must proceed, unless replacement measures can be found that have equivalent effect, as agreed by the institutions;

on labor markets, undertake rigorous reviews of collective bargaining, industrial action and collective dismissals in line with the timetable and the approach suggested by the institutions. Any changes should be based on international and European best practices, and should not involve a return to past policy settings which are not compatible with the goals of promoting sustainable and inclusive growth;

fully implement the relevant provisions of the Treaty on Stability, Coordination and Governance in the Economic and Monetary Union, in particular to make the Fiscal Council fully operational;

adopt the necessary steps to strengthen the financial sector, including decisive action on non-performing loans, transposition of BRRD and measures to strengthen governance of the HFSF and the banks;

develop a significantly scaled up privatization program with improved governance. A working group with the institutions shall provide proposals for better implementation mechanisms;

amend or compensate for legislation adopted during 2015 which have not been agreed with the institutions and run counter to the program commitments;

implement the key remaining elements from the December 2014 state of play of the fifth review of the second economic adjustment program."

After a day-long meeting of the Eurogroup, the European FinMins were unable to reach a conclusion on the third Greek bailout and instead once again punted the revised term sheet, this time with absolutely draconian terms, back to Tsipras, and told him he has until tomorrow to agree to the terms, and until Wednesday to pass them into law, for talks to even begin!

While there is "hope" in the unforgettable words of France's Moscovici, it is once again up to Greece to convince Europe it really wants to stay in the Union. According to Reuters, the Eurogroup is about to release a statement, whose draft it has seen, which will demand much more from the tiny country caught in a state of permanent depression. To wit: Greece will not be able to start negotiations on a third bailout until it makes changes to its sales tax and pension systems and strengthens the independence of its statistics office, a draft statement of euro zone finance ministers said on Sunday.

Here is the punchline from Greek nemesis #1, Schauble: SCHAEUBLE PROPOSES TIME-LIMITED `GREXIT': FAZ; SCHAEUBLE SUGGESTS 5-YR GREXIT, HUMANITARIAN SUPPORT: FAZ

In other words, Germany just said kick Greece out, conditionally, for 5 years (it is not quite clear what Greece would use for currency in the meantime), quarantine it, and treat it as a third-world country until 2020. Somehow we doubt global stocks expected this outcome when they soared on Friday...

Initially it was just an unconfirmed rumor circulating in the German FAS media that the local FinMin had proposed a "temporary Grexit" option. It now appears that this was not only not a rumor, but Schauble's sentiment is contagious: moments ago Finnish broadcaster MTV reported that first Finland, and then the Eurozone's smaller, if somewhat more solvent nations, Estonia, Lithuania, Slovakia, Slovenia and even the Netherlands, support the German position on temporarily suspending Greece' Euro membership.

Comments from the Eurozone finance ministers and others attending the Eurogroup meeting, via Reuters:

GERMAN FINANCE MINISTER WOLFGANG SCHAEUBLE

"We will have exceptionally difficult negotiations."

"The problem is that that there was a situation at the end of the year that was very hopeful, despite all the scepticism of previous years, and that this was destroyed in an incredible way in the last months and hours.

"We are dealing with financing gaps which exceed everything we have dealt with in the past."

"We are talking about a completely new three-year programme

LUXEMBOURG FINANCE MINISTER PIERRE GRAMEGNA

"We, as Luxembourg, because we hold the EU presidency right now, are definitely ready to discuss debt restructuring, finalising is another issue."

SLOVAKIAN FINANCE MINISTER PETER KAZIMIR

"I see a huge problem with DSA (debt sustainability analysis), so long-term sustainability of the Greek debt. So now we will see what the institutions will bring on the table, what kind of finances and we have to assess it... This package would be appropriate for the completion of the second programme, but I'm afraid this is not enough for the third programme, for the ESM programme."

EUROGROUP CHAIRMAN AND DUTCH FINANCE MINISTER JEROEN DIJSSELBLOEM

"We are still far away. It looks quite complicated. On both content and the more complicated question of trust, even if it's all good on paper the question is whether it will get off the ground and will it happen. So I think we are facing a difficult negotiation."

Will you talk about debt relief?

"I don't know we will get to that."

"There is still a lot of criticism on the proposal, reform side, fiscal side, and there is of course a major issue of trust. Can the Greek government be trusted to do what they are promising, to actually implement in coming weeks, months and years. I think those are the key issues that will be addressed today."

(For Greeks to regain trust) "Well, they will have to listen to the ministers and the institutions first and see what improvements are needed. And they will have to show very very strong commitments to rebuild that trust."

FRENCH FINANCE MINISTER MICHEL SAPIN

"Confidence has been ruined by every Greek government over many years which have sometimes made promises without making good on them at all. Today we need to have confidence again, to have certainty that decisions which are spoken of are decisions which are actually taken by the Greek government.

On debt restructuring: "France has always said there is no taboo about the debt. We have the right to talk about the debt."

We don't want there to be reduction in the nominal value of the debt because that is a red line for many of the member states in the Eurogroup.

"France ... is a link, and we will play this linking role to the very end."

ITALIAN ECONOMY AND FINANCE PIER CARLO PADOAN

"I expect a long finance ministers meeting on Greece. It is not very easy but we will do all we can."

"The purpose of this meeting is to kick off negotiations on ESM which is a medium-term, very demanding programme and we are all here with open minds to reach an OK, a green light to start negotiations. The government, the Greek Parliament and the Greek people are positive towards starting what is the beginning of a negotiation. It is not about striking a deal tonight."

MALTESE FINANCE MINISTER EDWARD SCICLUNA

"This (Greek issue) has to be solved today because it is a question of coming up with this framework which gives assurance to the finance ministers."

IRISH FINANCE MINISTER MICHAEL NOONAN

"The Greek paper was silent on banking. Obviously the Greek banks are in difficulty now and it's going to be hard to put them back on an even keel, so we need a full briefing on that. Secondly I said we needed a medium term sustainable programme. Sustainability depends a lot on whether the programme is sufficient to cause the Greek economy to grow and to create jobs... It is very hard to stimulate an economy when on the demand you are doing corrective work so they need more supply side initiatives which effectively means a lot of reform which doesn't seem to be built into the programme."

"I think the trust is now being rebuilt in the relationship with Greece. I would hope that trust would continue to be rebuilt today. That's pretty important also."

EUROPEAN COMMISSION VICE-PRESIDENT VALDIS DOMBROVSKIS

"It must be said that we are clearly making progress and the Greek government's proposal actually is pretty much along the lines of what the institutions' proposal was before the referendum. So clearly we see there is a willingness of the Greek to reach an agreement and also the vote in parliament showed that there is a parliamentary majority to move ahead with this programme."

"What we should be discussing today is basically about giving a mandate to the European Commission in liaison with the ECB and in close cooperation with the IMF to start negotiations about this ESM programme."

AUSTRIAN FINANCE MINISTER HANS JOERG SCHELLING

Asked about whether he was positive on a deal: "Yes and no. Of course it is a step ahead that Greece has finally delivered, surprisingly what was already agreed before and surprisingly after the referendum. What is missing are the details. The biggest item we have to talk about is what guarantees Greece can give to implement what has been agreed. We have seen for five years now that such lists are sent, but the implementing measures never happen."

DUTCH JUNIOR FINANCE MINISTER ERIC WIEBES

"The Greeks have clearly made a step forward but at the same time we see that the institutions are critical of the plan, the missing specificities and they see that the plan is weaker in some areas than it should be. It is their suggestion to only start negotiations when these conditions are further filled in.

At the same time, many governments, mine too, have serious concerns about the commitment of the Greek government and also the power of the implementation. That has been the weak point because after all, we are discussing a proposal from the Greek government that was fiercely rejected a week ago, and that is a serious concern.

(On what the Greeks can do further) we have to discuss that. Clearly there has to be made a step that enables trust with all the financing parties. (What happens if there is no agreement tonight) That is basically up to the Greek government."

IMF MANAGING DIRECTOR CHRISTINE LAGARDE

"I think we are here to make a lot more progress."

EUROPEAN ECONOMIC AFFAIRS COMMISSIONER PIERRE MOSCOVICI

"Since the start, the European Commission had the objective, that of the integrity of the euro. It was to keep a reformed Greece in the euro zone."

"I note that the Greek government has made significant gestures."

"We (the creditors) have said the Greek reform programme could constitute a basis for a new programme."

"Our general sentiment is that there need to be reforms, solid reforms, reforms appropriate to the Greek authorities and reforms that are implemented as soon as possible."

* * *

"BEST OF THE WEEK "

MOST CRITICAL TIPPING POINT & THEMES ARTICLES THIS WEEK

July 5th, 2015 - July 11th, 2015

BOND BUBBLE

1

RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates

2

GEO-POLITICAL EVENT

3

CHINA BUBBLE

4

JAPAN - DEBT DEFLATION

5

EU BANKING CRISIS

6

TO TOP

MACRO News Items of Importance - This Week

GLOBAL MACRO REPORTS & ANALYSIS

US ECONOMIC REPORTS & ANALYSIS

CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES

Market

TECHNICALS & MARKET

COMMODITY CORNER - AGRI-COMPLEX

PORTFOLIO

SECURITY-SURVEILANCE COMPLEX

PORTFOLIO

THEMES

THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur

Professor Joseph Salerno is a noted Austrian Economist who spoke with the Financial Repression Authority on Financial Repression and his growing concerns with what is referred to as "the War-On-Cash", which he sees leading America and other developed countries in the wrong direction. He sees it as presently gaining momentum in senior policy levels around the world as global debt problems become more acute.

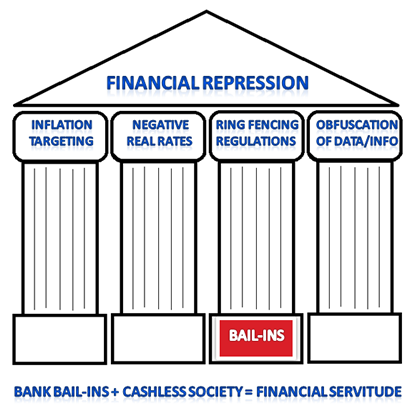

FINANCIAL REPRESSION

"A combination of Deliberate Inflation and very low Interest Rates. Interest rates which are kept low by a viarety of what are called "Unconventional Monetary Policies".

"There is talk now of having:

Negative Nominal Rates,

Governments taking over Pension Funds,

Varies 'priveleging' of government debt as part of bank capital.

so it (Financial Repression) is a series of inteferences in the financial markets by government with the end being to push interest rate lowers so they can inflate away their debt! They do that by having interest rates even lower than the rate of inflation."

"What Financial Repression does is transfer surreptitiously resources and coming wealth from savers and retirees to the government and its crony banks. I think it exists, it is dangersous and I think many people are being hurt by it!"

WAR-ON-CASH - GETTING TO NEGATIVE NOMINAL BOND RATES

Professor believes the goverment wants Negative Nominal Rates but as points out: "The only way they can do that is to lock peoples deposits into the banking system - that is where the War-on-Cash comes in! They would love to restrict or even abolish the use of cash within the United States if they could. That mans they would have to use deposits."

"This another way of propping up a very unsound and dangerously flawed banking system!"

Professor Salerno has spoken out extensively on this subject, most recently at the Mises Circle event in Stamford, Connecticut

Governments, at least modern western governments, have always hated cash transactions. Cash is private, and cash is hard to tax. So politicians trump up phony reasons like drug trafficking and money laundering to win support for bad laws like the Bank Secrecy Act of 1970, which makes even small cash transactions potentially reportable to the Feds.

Today cash is under attack like never before. Ultra low interest rates are the norm for commercial bank accounts. In Europe, as the ECB ventures into negative nominal interest rates, certain banks threaten to charge customers for depositing cash. Meanwhile, certain European bonds now pay negative yields, effectively turning them into insurance products rather than financial assets. And some economists now call for the outright abolition of cash, which shows just how far some will go in their crazed belief that economic prosperity can be commanded by forcing us to spend rather than save.

The War on Cash is real, and it will intensify.

PUBLIC FOREFEITURE

Both bank deposits and withdrawals of cash are now carefully srutenized by banks and police agencies across America. Safety deeposits boxes are seeing increasing restrictions on what can be held in them in the way of cash. People depositing cash often find themesleves facing public asset forefeitures and seizures by the police. In some cases when cleared as being innocent then have serious difficulty in getting their seized assets returned. Professor Salerno expounds on this and other troubling new developments in America.

....there is much, much more in this fact filled 29 minute Video.

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you confirm the facts on your own before making important investment commitments.

THE CONTENT OF ALL MATERIALS: SLIDE PRESENTATION AND THEIR ACCOMPANYING RECORDED AUDIO DISCUSSIONS, VIDEO PRESENTATIONS, NARRATED SLIDE PRESENTATIONS AND WEBZINES (hereinafter "The Media") ARE INTENDED FOR EDUCATIONAL PURPOSES ONLY.

The Media is not a solicitation to trade or invest, and any analysis is the opinion of the author and is not to be used or relied upon as investment advice. Trading and investing can involve substantial risk of loss. Past performance is no guarantee of future returns/results. Commentary is only the opinions of the authors and should not to be used for investment decisions. You must carefully examine the risks associated with investing of any sort and whether investment programs are suitable for you. You should never invest or consider investments without a complete set of disclosure documents, and should consider the risks prior to investing. The Media is not in any way a substitution for disclosure. Suitability of investing decisions rests solely with the investor. Your acknowledgement of this Disclosure and Terms of Use Statement is a condition of access to it. Furthermore, any investments you may make are your sole responsibility.

THERE IS RISK OF LOSS IN TRADING AND INVESTING OF ANY KIND. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Gordon emperically recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, he encourages you confirm the facts on your own before making important investment commitments.

DISCLOSURE STATEMENT

Information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities.

Please note that Mr. Long may already have invested or may from time to time invest in securities that are discussed or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him.

FAIR USE NOTICEThis site contains

copyrighted material the use of which has not always been specifically

authorized by the copyright owner. We are making such material available in

our efforts to advance understanding of environmental, political, human

rights, economic, democracy, scientific, and social justice issues, etc. We

believe this constitutes a 'fair use' of any such copyrighted material as

provided for in section 107 of the US Copyright Law. In accordance with

Title 17 U.S.C. Section 107, the material on this site is distributed

without profit to those who have expressed a prior interest in receiving the

included information for research and educational purposes.

If you wish to use

copyrighted material from this site for purposes of your own that go beyond

'fair use', you must obtain permission from the copyright owner.

Submitted by Tyler Durden on 07/13/2015 - 12:47

Submitted by Tyler Durden on 07/13/2015 - 12:47

Submitted by Tyler Durden on 07/13/2015 - 12:05

Submitted by Tyler Durden on 07/13/2015 - 12:05

Submitted by Tyler Durden on 07/13/2015 - 11:32

Submitted by Tyler Durden on 07/13/2015 - 11:32

Submitted by Tyler Durden on 07/13/2015 - 08:54

Submitted by Tyler Durden on 07/13/2015 - 08:54

Submitted by Tyler Durden on 07/13/2015 - 10:35

Submitted by Tyler Durden on 07/13/2015 - 10:35

Submitted by Tyler Durden on 07/13/2015 - 09:30

Submitted by Tyler Durden on 07/13/2015 - 09:30

Submitted by Tyler Durden on 07/13/2015 - 09:17

Submitted by Tyler Durden on 07/13/2015 - 09:17

Submitted by Tyler Durden on 07/13/2015 - 07:54

Submitted by Tyler Durden on 07/13/2015 - 07:54

Submitted by Tyler Durden on 07/13/2015 - 13:54

Submitted by Tyler Durden on 07/13/2015 - 13:54

Submitted by Tyler Durden on 07/13/2015 - 06:54

Submitted by Tyler Durden on 07/13/2015 - 06:54

Submitted by Tyler Durden on 07/13/2015 - 08:38

Submitted by Tyler Durden on 07/13/2015 - 08:38

Submitted by Tyler Durden on 07/13/2015 - 08:05

Submitted by Tyler Durden on 07/13/2015 - 08:05

Submitted by Tyler Durden on 07/13/2015 - 06:16

Submitted by Tyler Durden on 07/13/2015 - 06:16